For many individuals, the purchase of a home represents the most significant financial transaction of their lives. Because few people have the liquid capital to purchase a property outright, the home loan—or mortgage—acts as the essential bridge between a financial dream and the reality of property ownership. Understanding how these loans function is not merely a matter of administrative necessity; it is a vital component of long-term wealth management and personal financial health.

A home loan is a secured loan used to purchase real estate. The property itself serves as collateral, meaning that if the borrower fails to meet the repayment terms, the lender has the legal right to seize the property through foreclosure. While this may sound daunting, the structured nature of home loans allows millions of people to build equity and secure a stable living environment. To navigate this complex landscape, one must understand the mechanics, the costs, and the strategic implications of borrowing.

The Mechanics of a Home Loan: Principal, Interest, and Amortization

At its core, a home loan is comprised of several moving parts that dictate how much you pay each month and how much the loan costs you over its entire lifespan. Understanding these components is the first step in mastering your personal finances.

The Relationship Between Principal and Interest

Every mortgage payment is generally split into two primary buckets: principal and interest. The principal is the actual amount of money you borrowed from the bank to buy the home. The interest is the cost of borrowing that money, expressed as a percentage. In the early years of a loan, a larger portion of your monthly payment goes toward interest. As the balance decreases, a larger percentage of your payment is applied to the principal.

The Role of the Down Payment

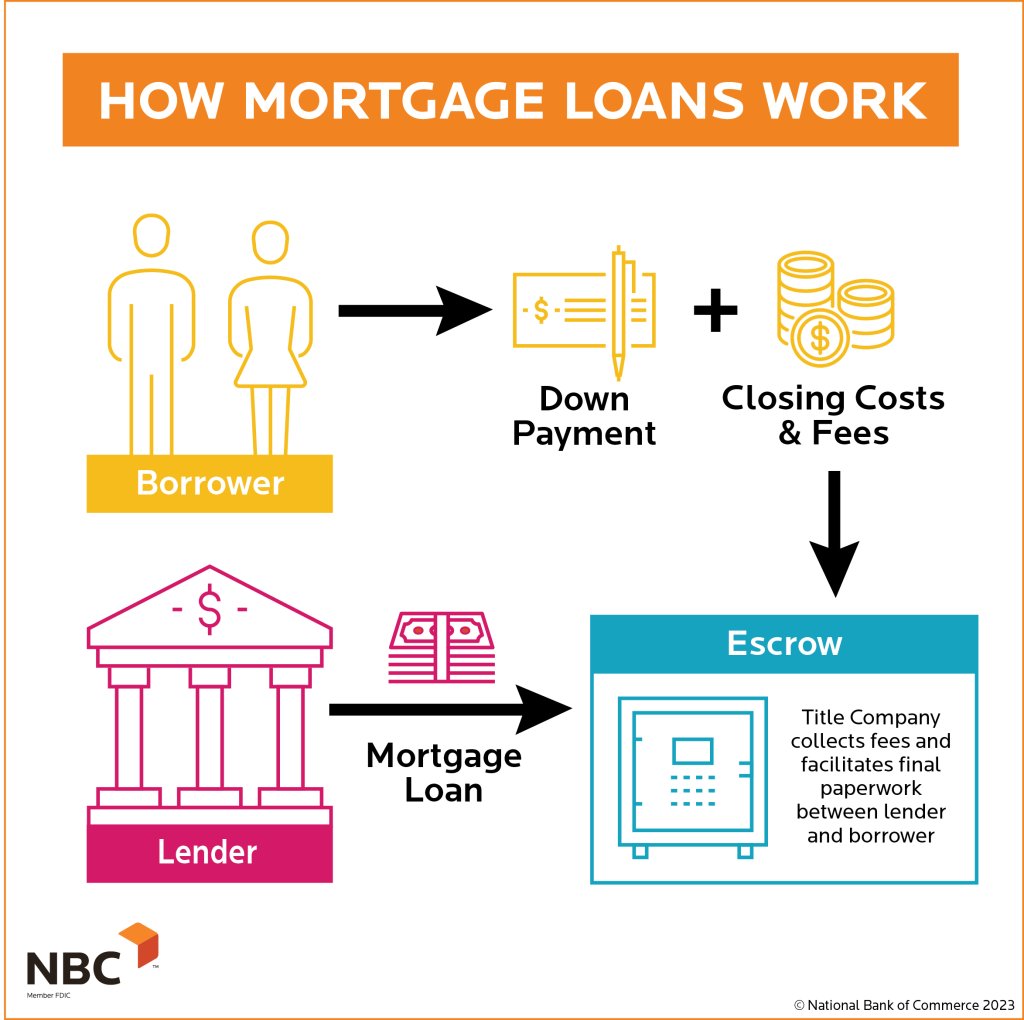

The down payment is the initial cash payment you make toward the purchase of the home. In the world of personal finance, the size of your down payment has a cascading effect on your loan’s health. Traditionally, a 20% down payment is the gold standard, as it often eliminates the need for Private Mortgage Insurance (PMI) and secures better interest rates. However, many modern financial products allow for down payments as low as 3% or 3.5%, though this usually results in a higher monthly cost due to insurance premiums.

Understanding the Amortization Schedule

Amortization is the process of paying off debt through regular installments over a fixed period. A home loan comes with an amortization schedule—a table that details every payment over the life of the loan. This schedule is a powerful financial tool; it shows you exactly how much equity you are building each year and how much you are saving (or losing) by making extra payments toward the principal.

Types of Mortgages: Choosing the Right Financial Vehicle

Not all home loans are created equal. The type of mortgage you choose should align with your financial goals, your risk tolerance, and the length of time you plan to stay in the home.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The most common choice is the Fixed-Rate Mortgage, where the interest rate remains the same for the entire life of the loan (usually 15 or 30 years). This provides predictability and protects the borrower from rising market interest rates. On the other hand, an Adjustable-Rate Mortgage (ARM) typically offers a lower initial interest rate for a set period (like 5 or 7 years), after which the rate adjusts based on market conditions. ARMs can be strategic for those who plan to sell the home before the adjustment period begins, but they carry the risk of significantly higher payments in the future.

Government-Backed Loans: FHA, VA, and USDA

For those who may not qualify for a “conventional” loan, the government offers several programs to encourage homeownership. FHA loans, backed by the Federal Housing Administration, are popular for first-time buyers with lower credit scores or smaller down payments. VA loans are available to veterans and active-duty service members, often requiring no down payment at all. USDA loans target rural homebuyers and also offer low-to-no down payment options. Each of these has specific eligibility requirements and fee structures that impact your overall financial plan.

Conventional and Jumbo Loans

Conventional loans are not insured by the federal government and typically follow the guidelines set by Fannie Mae or Freddie Mac. They often require higher credit scores but offer more flexibility. When a loan amount exceeds local “conforming” limits—often in high-cost-of-living areas—it becomes a Jumbo Loan. These require more rigorous financial vetting, higher down payments, and significant cash reserves, as they represent a higher risk to the lender.

The Financial Math: Interest Rates, APR, and Qualification

To understand how home loans work, you must look beyond the “sticker price” of the home and focus on the cost of the capital. Small fluctuations in interest rates can result in tens of thousands of dollars in difference over the life of a loan.

Factors Influencing Your Interest Rate

Lenders determine your interest rate based on a combination of macroeconomic factors and your personal financial profile. Your credit score is perhaps the most significant factor you can control; a score above 740 typically unlocks the best available rates. Additionally, your Debt-to-Income (DTI) ratio—the percentage of your gross monthly income that goes toward paying debts—tells the lender if you can afford the monthly commitment. A DTI of 36% or lower is generally preferred by financial institutions.

The Importance of the APR

When comparing loan offers, the interest rate is only part of the story. The Annual Percentage Rate (APR) includes the interest rate plus other costs, such as lender fees, closing costs, and mortgage insurance. Therefore, the APR is a more accurate reflection of the true cost of the loan. As a savvy borrower, you should always compare the APRs of different lenders to see which institution is truly offering the best deal.

The Impact of the Loan Term

Choosing between a 15-year and a 30-year mortgage is a fundamental personal finance decision. A 30-year mortgage offers lower monthly payments, providing more “breathing room” in your monthly budget. However, a 15-year mortgage typically comes with a lower interest rate and results in significantly less interest paid over time. For example, on a $300,000 loan, a 15-year term could save you over $100,000 in interest compared to a 30-year term, though the monthly payment will be substantially higher.

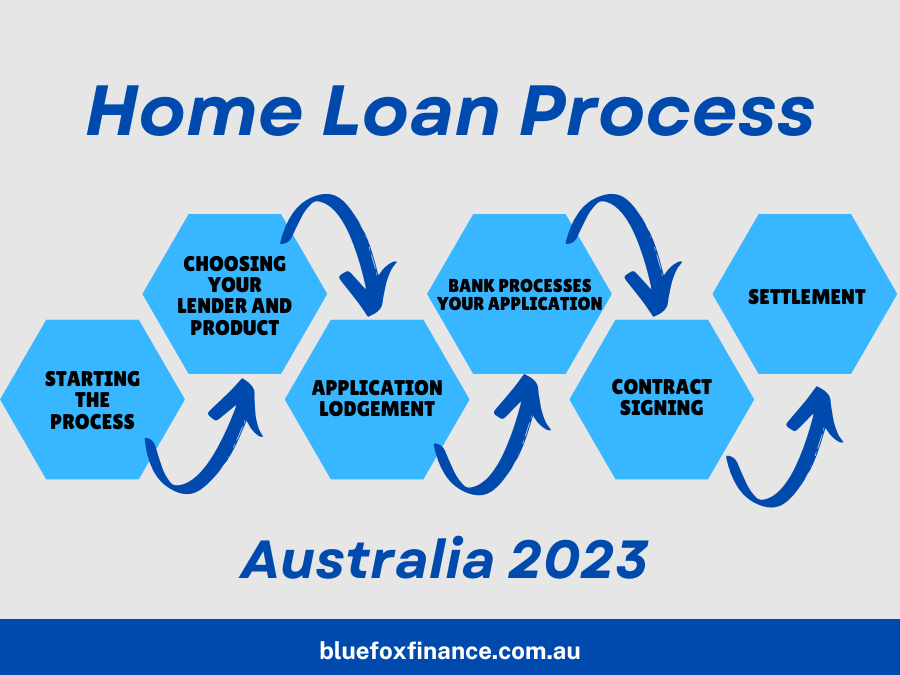

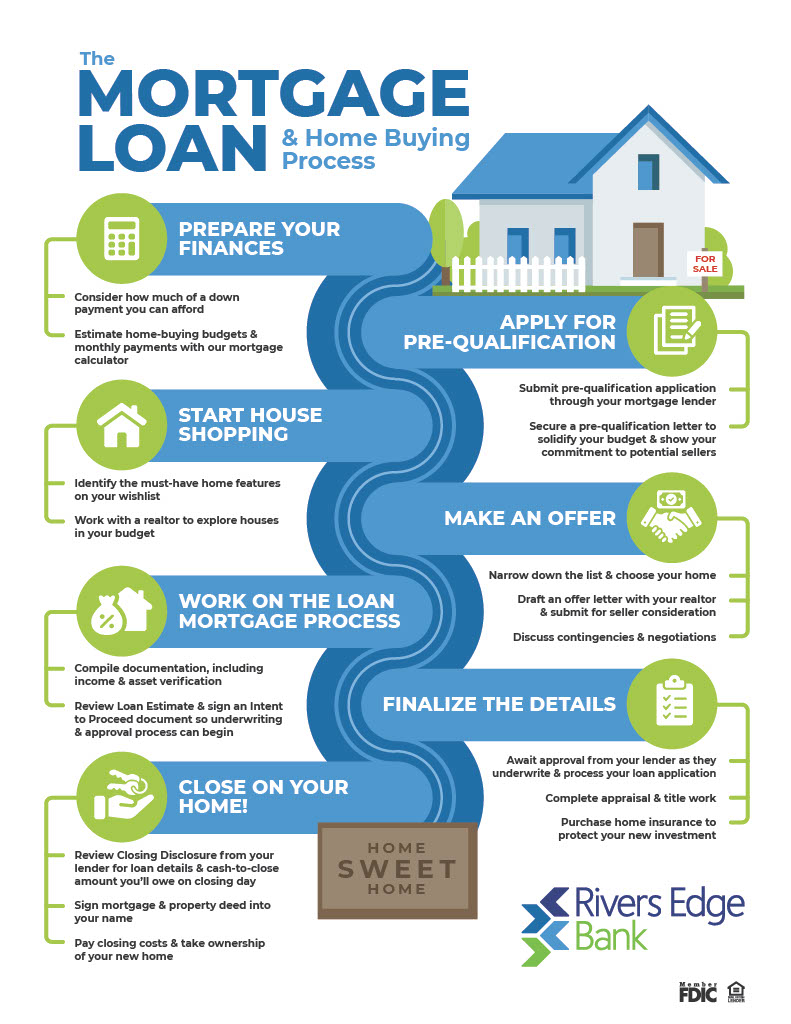

The Path to Approval: From Pre-Approval to Closing

The process of obtaining a home loan is a rigorous exercise in financial transparency. It requires a deep dive into your economic history and current standing.

Pre-approval vs. Pre-qualification

The journey begins with pre-qualification, which is a basic estimate of how much you might be able to borrow. However, a “Pre-approval” is far more significant. It involves a lender verifying your income, assets, and credit. In a competitive real estate market, a pre-approval letter is an essential tool, signaling to sellers that you are a serious and financially capable buyer.

The Underwriting Process

Once you have found a home and made an offer, the loan enters the “underwriting” phase. This is where the lender’s “detectives” verify every detail of your financial life. They will look at tax returns, bank statements, and employment history. They will also order an appraisal of the property to ensure that the home’s value justifies the loan amount. During this time, it is critical not to make any major financial changes, such as changing jobs or taking out a new car loan, as this can disqualify you from the mortgage.

Closing Costs and Finalizing the Deal

The final step is “closing,” where the ownership of the property is officially transferred. Borrowers must be prepared for closing costs, which typically range from 2% to 5% of the home’s purchase price. These costs cover title insurance, attorney fees, taxes, and escrow deposits. Understanding these upfront costs is essential for proper budgeting, as they must be paid in cash at the time of closing.

Long-Term Wealth Building Through Home Ownership

A home loan should not be viewed merely as a monthly expense; it is a vehicle for wealth accumulation and financial stability.

Building Equity and Net Worth

Every time you make a mortgage payment, you are essentially transferring money from one part of your balance sheet to another. As the principal balance decreases and property values (ideally) increase, your equity grows. This equity is a form of forced savings that contributes significantly to your net worth over time. Eventually, this equity can be tapped into via Home Equity Lines of Credit (HELOCs) for home improvements or other investments.

Strategic Refinancing

Home loans are not static. If market interest rates drop, or if your credit score improves significantly, you may choose to refinance. Refinancing involves taking out a new loan to pay off the old one, ideally at a lower interest rate or with better terms. This can lower your monthly payments or allow you to shorten the term of the loan, further accelerating your path to being debt-free.

Tax Implications and Financial Benefits

In many jurisdictions, homeownership comes with financial incentives. The interest paid on a mortgage is often tax-deductible (up to certain limits), which can lower your overall tax liability. Furthermore, while rent prices tend to increase over time with inflation, a fixed-rate mortgage keeps your housing “cost of capital” stable for decades, providing a powerful hedge against inflation.

In conclusion, understanding how home loans work is a cornerstone of financial literacy. By mastering the mechanics of interest, choosing the right loan product, and managing the approval process with diligence, you can turn a mortgage from a simple debt into a strategic tool for building lifelong wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.