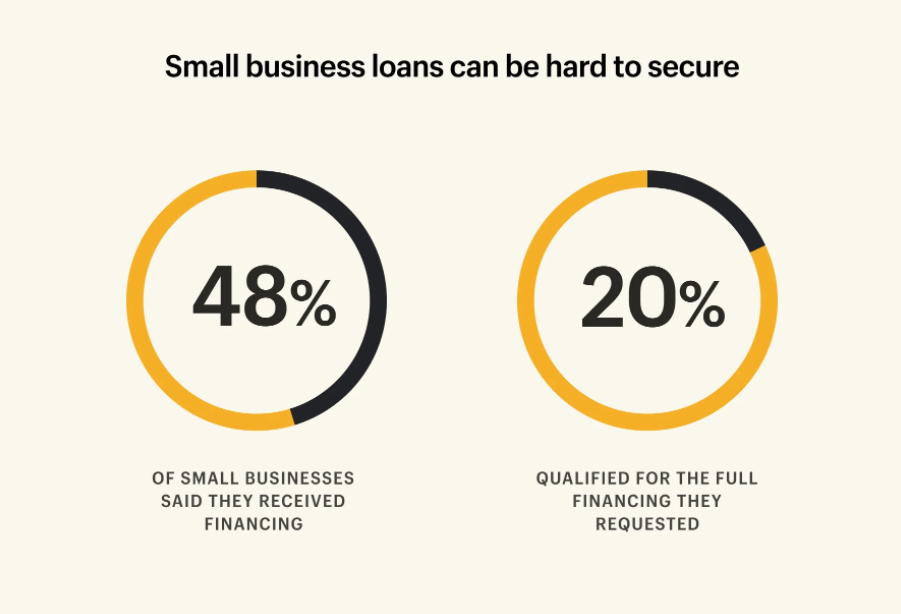

The quest for small business funding is a perennial challenge for entrepreneurs, ranging from nascent startups to established enterprises looking to expand. The perception of difficulty surrounding small business loans is often rooted in a complex interplay of economic conditions, lender requirements, and the borrower’s preparedness. While securing capital can indeed be arduous, understanding the landscape, preparing meticulously, and knowing where to look can significantly mitigate the hurdles.

The Evolving Landscape of Small Business Lending

The journey to obtaining a small business loan has always been dynamic, shaped by global economic trends, regulatory changes, and technological advancements. What was true a decade ago may not hold today, making continuous awareness crucial for any aspiring borrower.

Traditional Lenders vs. Alternative Options

Historically, traditional banks have been the primary source of small business loans. These institutions often offer the most competitive interest rates and favorable terms, but they also tend to have the most stringent approval processes. They typically require extensive documentation, a robust credit history, significant collateral, and a proven track record, making them challenging for startups or businesses with less-than-perfect financial histories.

The rise of financial technology (fintech) has revolutionized the lending landscape, ushering in a plethora of alternative lenders. Online lenders, peer-to-peer platforms, and community development financial institutions (CDFIs) offer more flexible criteria, faster application processes, and quicker funding times. While these options can be a lifeline for businesses unable to meet traditional bank requirements, they often come with higher interest rates and shorter repayment periods. The difficulty, therefore, is relative: easier access often means higher costs.

Post-Pandemic Shifts and Economic Factors

The COVID-19 pandemic introduced unprecedented volatility to the small business sector, prompting government intervention like the Paycheck Protection Program (PPP) and Economic Injury Disaster Loans (EIDL). While these programs provided temporary relief, their cessation has pushed many businesses back to traditional and alternative lending markets.

Current economic factors, such as inflation, rising interest rates, and potential recessionary pressures, further complicate the lending environment. Lenders become more risk-averse during periods of economic uncertainty, tightening their underwriting standards and demanding greater assurances from borrowers. This means that even well-qualified businesses might find the lending market less accommodating than in more stable times. The overall economic outlook directly influences the supply and cost of capital, making it inherently more difficult to secure loans when the future appears less certain.

Key Factors Influencing Loan Approval

Lenders, regardless of their type, assess a range of factors to determine a borrower’s creditworthiness and the likelihood of loan repayment. Understanding these critical elements is the first step toward overcoming the perceived difficulty.

Creditworthiness: Personal and Business

A strong credit profile is paramount. For established businesses, lenders scrutinize the business’s credit score (e.g., Paydex score from Dun & Bradstreet) and credit history, looking for consistent on-time payments, responsible debt management, and a low utilization rate.

For startups or younger businesses, the personal credit score of the business owner(s) often plays a more significant role. A FICO score of 680 or higher is generally considered good, but many traditional banks prefer scores in the 700s. A low personal credit score can be a substantial barrier, signaling to lenders a higher risk of default. Building and maintaining excellent personal and business credit is a long-term strategy but one that dramatically eases the loan application process.

Business Plan and Financial Projections

A comprehensive and compelling business plan is more than just a formality; it’s a critical tool for convincing lenders of your business’s viability and growth potential. The plan should clearly articulate your business model, market analysis, competitive advantage, management team, and, crucially, detailed financial projections.

Lenders want to see realistic and well-supported forecasts for revenue, expenses, and cash flow. They will scrutinize these projections to assess your ability to generate sufficient income to cover loan repayments. A poorly structured or overly optimistic business plan immediately raises red flags, making the loan significantly harder to obtain.

Collateral and Guarantees

Many small business loans, especially from traditional banks, are secured by collateral. This can include real estate, inventory, accounts receivable, equipment, or other business assets that the lender can seize if the borrower defaults. The value and liquidity of the collateral directly influence the loan amount and terms offered.

For businesses without substantial hard assets, a personal guarantee from the owner is often required. This means the owner is personally responsible for repaying the loan if the business cannot, putting personal assets at risk. The necessity of collateral or a personal guarantee can make obtaining a loan feel more daunting, particularly for owners who are reluctant to risk personal wealth.

Time in Business and Industry Stability

Lenders generally prefer to fund businesses with a proven track record. Many traditional banks require a minimum of two years in operation, as this period typically demonstrates stability, consistent revenue, and the ability to weather initial challenges. Startups often face greater difficulty in securing conventional loans due to this lack of operating history.

The industry in which your business operates also plays a role. Lenders assess industry-specific risks, growth potential, and economic sensitivity. Businesses in highly volatile or declining industries may face more scrutiny or higher interest rates, reflecting the increased perceived risk.

Common Hurdles and Pitfalls

Beyond the core factors, several common mistakes and oversights can trip up small business owners in their pursuit of capital.

Insufficient Documentation

The loan application process is documentation-intensive. Lenders require a vast array of financial statements (balance sheets, income statements, cash flow statements), tax returns (personal and business), bank statements, legal documents (articles of incorporation, licenses), and more. Failing to provide complete, accurate, and organized documentation not only delays the process but can also lead to an outright denial. It signals a lack of organization and preparedness, eroding lender confidence.

High Debt-to-Equity Ratios

Lenders meticulously analyze a business’s existing debt load relative to its equity. A high debt-to-equity ratio indicates that the business is heavily leveraged, relying more on borrowed funds than owner investment. This suggests a higher financial risk and can make lenders hesitant to extend additional credit. It’s crucial for businesses to maintain a healthy balance between debt and equity to appear attractive to potential lenders.

Lack of a Clear Use of Funds

Lenders want to know exactly how the loan proceeds will be used and how that use will contribute to the business’s growth and ability to repay the loan. Vague or poorly defined intentions for the funds — for example, simply “for working capital” without further explanation — are red flags. A precise breakdown of how the money will be allocated (e.g., purchasing specific equipment, funding a marketing campaign, hiring key personnel) demonstrates strategic thinking and a clear path to return on investment.

Choosing the Wrong Loan Product

The small business lending market offers a diverse range of products, from term loans and lines of credit to SBA-backed loans, invoice financing, and equipment loans. Each product is designed for specific purposes and comes with unique eligibility requirements and terms. Applying for a loan that doesn’t align with your business’s needs or financial profile is a common pitfall. For instance, seeking a long-term equipment loan for short-term operational expenses is a mismatch that lenders will quickly identify, leading to rejection.

Strategies to Improve Your Chances

While securing a small business loan can be challenging, proactive measures can significantly increase your likelihood of success.

Build a Strong Financial Foundation

Start early. Focus on improving both your personal and business credit scores. Pay bills on time, reduce existing debt, and monitor your credit reports for errors. Maintain robust financial records and generate accurate, up-to-date financial statements regularly. A strong financial foundation is the bedrock of any successful loan application.

Refine Your Business Plan

Ensure your business plan is not only comprehensive but also compelling and realistic. Clearly articulate your vision, market opportunity, and, most importantly, a detailed financial strategy that justifies the loan amount and demonstrates repayment capability. Seek feedback from mentors or business advisors to strengthen your plan.

Understand Lender Expectations

Research different types of lenders and their specific criteria. Don’t apply blindly. Understand the difference between traditional banks, online lenders, and SBA-backed loans. Each has its niche, and aligning your business’s profile with the right lender’s appetite can save time and effort. Many lenders publish their basic eligibility requirements, providing a useful starting point.

Explore Different Lender Types

Don’t limit yourself to just one type of lender. If traditional banks deem your business too risky, explore alternative online lenders, credit unions, or CDFIs. SBA loans, for instance, are attractive because they mitigate risk for lenders, often leading to more favorable terms for borrowers, even those who might not qualify for conventional loans. These programs have specific requirements, but they broaden the access to capital significantly.

Prepare Comprehensive Documentation

Before you even begin the application process, gather all necessary financial and legal documents. Organize them meticulously. Having everything readily available and presented professionally demonstrates your seriousness and attention to detail, making the lender’s job easier and speeding up the review process. Consider creating a “loan readiness” folder with all essential paperwork.

In conclusion, while the path to securing a small business loan is rarely without obstacles, labelling it as “difficult” isn’t a definitive statement. It’s more accurate to say it requires diligence, strategic preparation, and an informed approach. By understanding the lending landscape, recognizing the factors that influence approval, avoiding common pitfalls, and implementing robust strategies, entrepreneurs can significantly enhance their prospects of securing the capital needed to fuel their business growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.