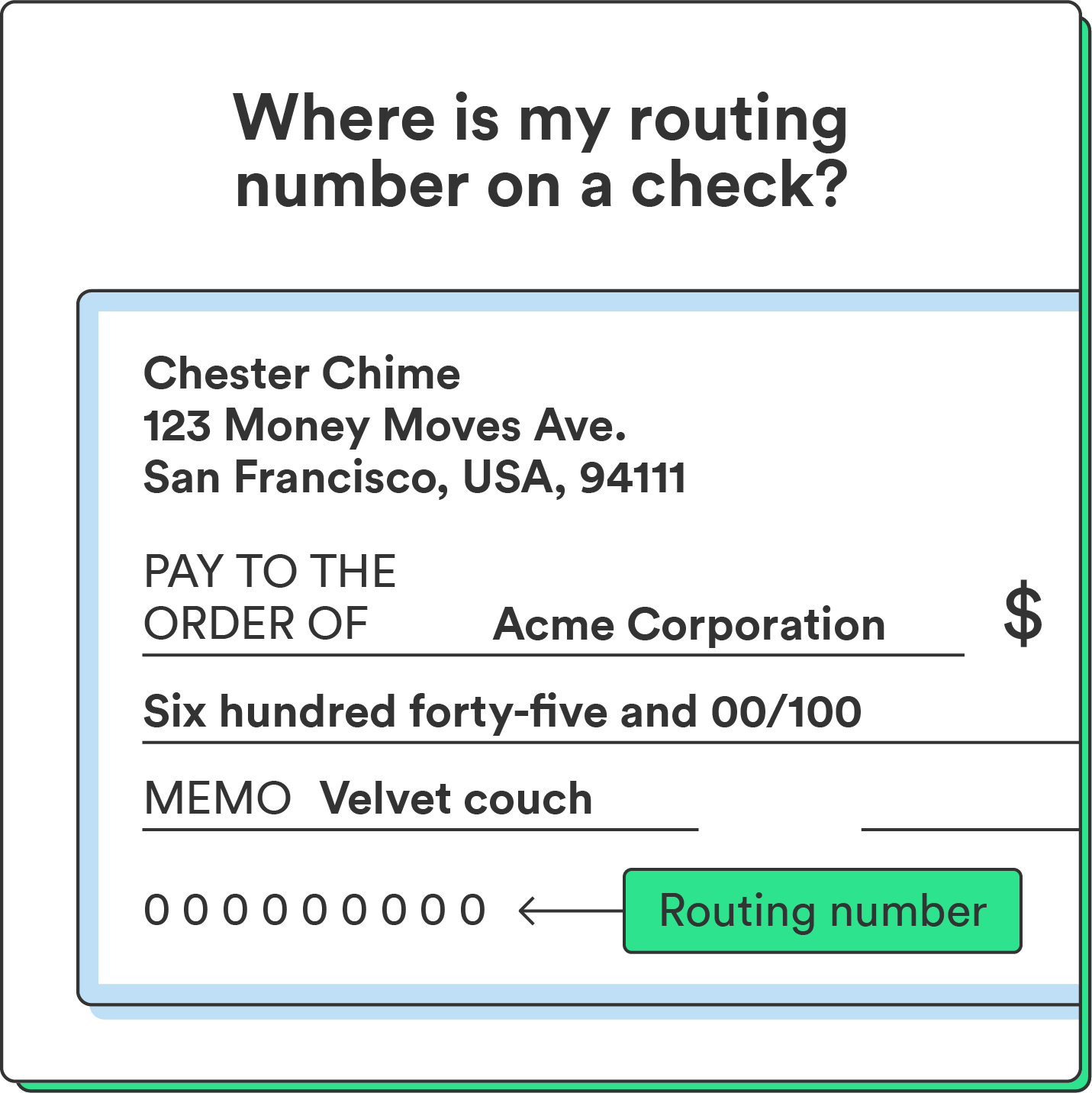

In today’s increasingly digital financial landscape, the physical checkbook often feels like a relic of a bygone era. Yet, the routing number, a critical nine-digit code essential for numerous financial transactions, remains as vital as ever. While traditionally found at the bottom of a paper check, many individuals find themselves needing this number without a check in hand. Whether you’re setting up direct deposit, paying bills online, initiating a wire transfer, or linking external accounts, knowing how to quickly and securely locate your routing number is a fundamental aspect of modern personal finance. This guide will walk you through the most effective and accessible methods to retrieve this crucial piece of information, ensuring your financial transactions proceed without a hitch, even if your checkbook is nowhere in sight.

Understanding Your Routing Number: The Essential Identifier

Before diving into how to find it, it’s crucial to understand what a routing number is and why it holds such significance in the financial ecosystem. This foundational knowledge empowers you to appreciate its role and handle it with the necessary care.

What is a Routing Number?

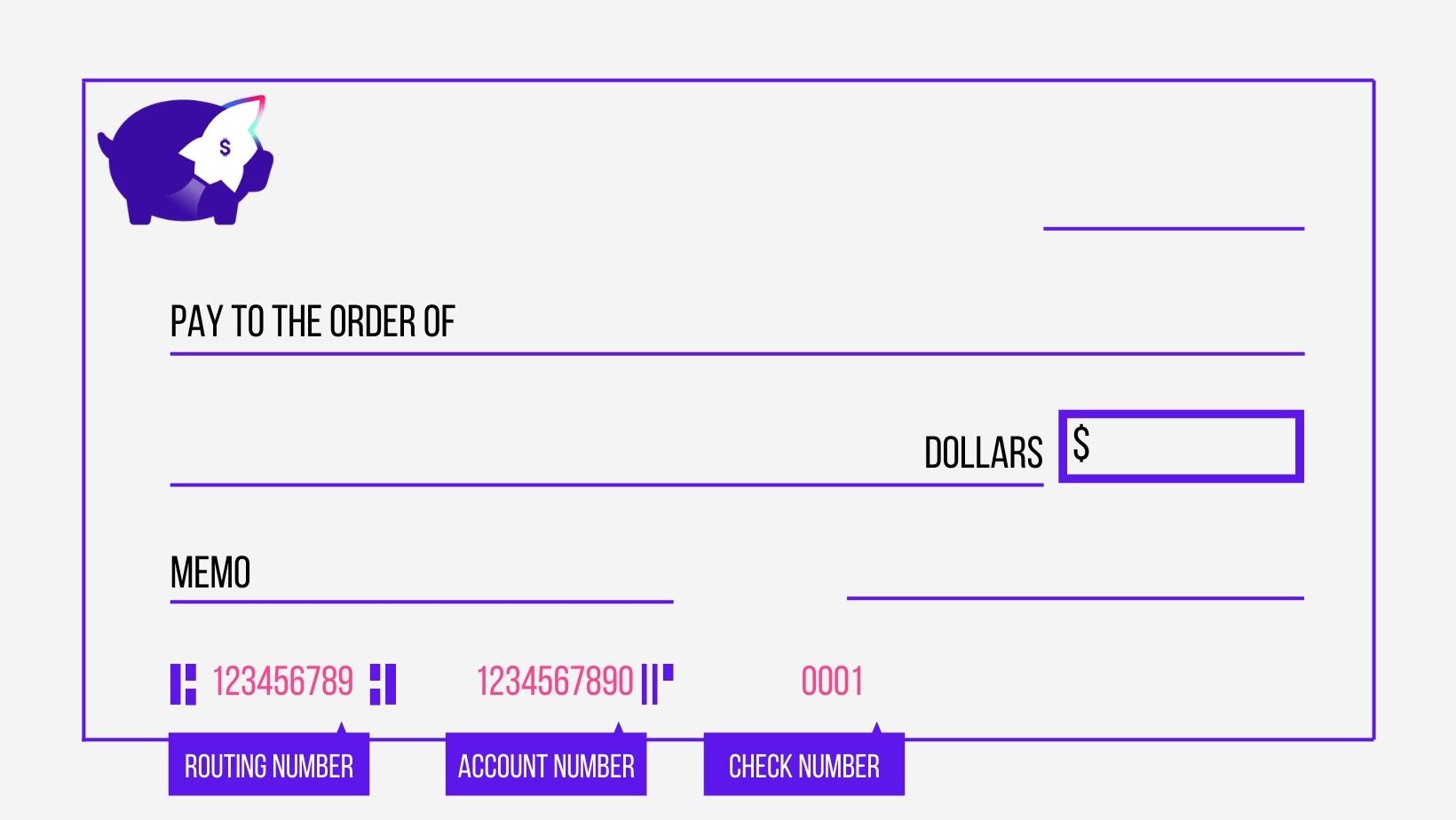

A routing number, also known as an ABA (American Bankers Association) routing transit number, is a nine-digit code used by banks to identify specific financial institutions within the United States. It acts much like a postal code for mail, but for money. Each bank and often different branches or types of accounts within a bank will have a unique routing number, ensuring that funds are directed to the correct financial institution during transactions. These numbers are public information for financial institutions but are essential for distinguishing one bank from another in the vast network of financial transactions.

Why is Your Routing Number Crucial?

The routing number serves as a cornerstone for a wide array of financial operations, making its availability paramount for managing your money effectively. Without it, many common banking activities would be impossible.

- Direct Deposits: This is perhaps the most common use. Whether it’s your paycheck, government benefits, or tax refunds, a routing number is combined with your account number to ensure funds land directly into your bank account.

- Automated Bill Payments: Many services, from utilities to subscriptions, offer automated payments directly from your bank account. This requires providing both your routing and account numbers to authorize the transactions.

- Electronic Funds Transfers (EFTs): This broad category includes everything from transferring money between your own accounts at different banks to sending money to friends or family via services that link directly to bank accounts.

- Wire Transfers: While often requiring additional security measures and information, domestic wire transfers fundamentally rely on routing numbers to direct funds to the correct receiving bank.

- Linking External Accounts: Modern financial management often involves linking accounts across different platforms – think investment apps, budgeting tools, or peer-to-peer payment services. These links are almost always established using your routing and account numbers.

Anatomy of a Routing Number

While the routing number appears as a single nine-digit sequence, it’s actually structured to convey specific information. The first four digits identify the Federal Reserve routing symbol, indicating the Federal Reserve district bank that processes payments for the financial institution. The next four digits identify the financial institution itself, and the final digit is a check digit, used to validate the entire sequence and prevent errors. This intricate design ensures accuracy and security in the transfer of funds across the nation’s banking system.

Digital Pathways: Accessing Your Routing Number Online

In an era dominated by digital convenience, your bank’s online platforms and mobile applications are often the quickest and most accessible sources for your routing number. These methods leverage secure, authenticated access to your account information.

Your Online Banking Portal

The most straightforward digital method is usually through your bank’s online banking portal. Once you log in to your account, your routing number is often prominently displayed or easily accessible within your account details.

- Log In Securely: Navigate to your bank’s official website and log in using your established username and password. Always ensure you are on the legitimate bank website to avoid phishing scams.

- Locate Account Information: Once logged in, look for sections like “Account Summary,” “Account Details,” “My Accounts,” or similar tabs.

- Find the Routing Number: Your checking account’s routing number is typically listed alongside your account number. Sometimes, you might need to click on a specific account to view its detailed information. Many banks also have a dedicated “Contact Us,” “Help,” or “FAQ” section where common routing numbers for various account types (e.g., checking, savings, wire transfers) are listed. Be mindful that some banks have different routing numbers for different types of transactions (e.g., domestic wire transfers versus ACH transfers).

Leveraging Your Bank’s Official Website

Even without logging into your personal account, most banks make their primary routing numbers publicly available on their official websites. This is particularly useful if you are setting up an account for the first time or simply need a quick reference.

- Navigate to the Bank’s Homepage: Go to the official website of your bank.

- Search or Browse: Use the website’s search bar and type “routing number,” “ABA number,” or “direct deposit.” Alternatively, look for links such as “About Us,” “Contact Us,” “FAQs,” or “Support.”

- Identify the Correct Number: Banks often have dedicated pages listing their routing numbers. Pay close attention to ensure you select the correct routing number for your specific region or account type, especially if your bank operates nationally or has different numbers for different purposes (e.g., checking, savings, wire transfers). Some larger banks may have multiple routing numbers depending on where the account was opened.

Mobile Banking Apps: Convenience at Your Fingertips

For those who manage their finances on the go, mobile banking apps offer a highly convenient way to retrieve your routing number.

- Open and Log In: Launch your bank’s official mobile app on your smartphone or tablet and log in securely.

- Access Account Details: Similar to online banking portals, navigate to your account details. This is often done by tapping on the specific account (e.g., “Checking Account”) from the main dashboard.

- View Routing Information: Your routing number is typically displayed directly on the account details screen, sometimes under an “Information” or “Show Details” button. Many apps also have a dedicated section for “Direct Deposit Information” which will prominently feature both your routing and account numbers.

Direct Communication: Reaching Out to Your Financial Institution

While digital methods are often the quickest, sometimes a direct interaction with your bank is necessary or preferred. These traditional avenues remain highly reliable for obtaining accurate routing number information.

A Call to Customer Service

A simple phone call to your bank’s customer service line can quickly provide you with the routing number you need. This method is particularly useful if you’re having trouble navigating online platforms or need clarification on different routing numbers for various transaction types.

- Locate the Number: Find your bank’s customer service phone number on their official website, the back of your debit card, or a recent bank statement.

- Prepare for Verification: When you call, the representative will ask you security questions to verify your identity. Have your account number, personal identification information (e.g., date of birth, Social Security number last four digits), and potentially a recent transaction detail ready.

- Request the Routing Number: Clearly state that you need your routing number for your checking or savings account. If applicable, specify the type of transaction (e.g., direct deposit, wire transfer) as some banks have different routing numbers for these purposes.

- Confirm and Note: Confirm the number with the representative and write it down accurately.

Visiting a Local Branch

For those who prefer face-to-face interaction or require additional assistance, visiting a local branch of your bank is a dependable option.

- Bring Identification: Make sure to bring a valid government-issued photo ID (driver’s license, passport) and possibly your debit card or account number for quick verification.

- Speak with a Teller or Representative: Explain your need for the routing number to a bank teller or customer service representative.

- Receive Assistance: They will be able to provide you with the correct routing number for your account and can often print out a slip with the information, or even help you set up direct deposit forms if that’s your ultimate goal. This method offers the highest level of personal assistance and security.

Decoding Your Bank Statements

Whether you receive physical mail statements or opt for electronic (e-statements), your bank statement is a reliable document containing your routing number.

- Locate a Recent Statement: Find a recent physical bank statement mailed to you, or log into your online banking portal to access e-statements.

- Review the Document: Your routing number is typically printed prominently on the statement, often near your account number, bank name, and address. It might be listed under a section like “Direct Deposit Information” or “Important Bank Information.”

- Identify Correct Number: Ensure you’re looking at the routing number for your checking account, as savings accounts sometimes have different numbers, though this is less common for ACH transfers.

Alternative Scenarios and Key Considerations

Beyond the standard methods, understanding when and how your routing number is used, along with critical security practices, is paramount for responsible financial management.

What if You’re Setting Up New Accounts or Services?

Many modern financial services require your routing and account numbers to link external bank accounts. This includes:

- Peer-to-Peer Payment Apps: Services like PayPal, Venmo, Cash App, and Zelle often require linking to a bank account via routing and account numbers for easy transfers.

- Investment and Brokerage Accounts: To fund your investment accounts, you’ll typically need to provide your bank’s routing number for ACH transfers.

- Online Wallets and Budgeting Tools: Various financial management apps and digital wallets integrate with your bank accounts for comprehensive financial oversight, necessitating your routing number during setup.

- Payroll and Benefits Portals: When starting a new job or setting up government benefits, you’ll input your routing and account numbers directly into their secure online portals or on paper forms.

In all these scenarios, follow the specific instructions provided by the service and ensure you are using their official, secure platforms.

Security Best Practices When Sharing Your Routing Number

While your routing number is less sensitive than your full account number or PIN, it’s still a critical piece of financial information that should be protected.

- Be Cautious Online: Only enter your routing number on secure, encrypted websites (look for “https://” in the URL and a padlock icon).

- Verify Recipients: Always confirm that the party requesting your routing number is legitimate and has a valid reason for needing it. For example, your employer for direct deposit or a reputable biller for automated payments.

- Beware of Phishing: Be extremely wary of unsolicited emails, texts, or calls asking for your routing number. Banks and legitimate institutions will rarely ask for this information via unsecure channels.

- Monitor Accounts: Regularly review your bank statements and online banking activity to catch any unauthorized transactions promptly.

When to Be Cautious: Avoiding Scams

Scammers frequently attempt to acquire banking details through various deceptive tactics. Understanding common red flags can protect you:

- “Official-Looking” Requests: Scammers may impersonate your bank, a government agency, or a familiar company, claiming an “issue” with your account and asking for your banking details to “resolve” it. Always independently verify the source.

- Too Good to Be True Offers: Be suspicious of requests for your routing number in exchange for lottery winnings, inheritances, or other improbable windfalls.

- Unknown Callers/Emails: Never give your routing number to someone who calls or emails you out of the blue, claiming to be from your bank or a government agency. If in doubt, hang up and call the official number of the institution.

In conclusion, while the traditional check may be fading from everyday use, the routing number remains an indispensable component of financial transactions. By utilizing your bank’s online portals, mobile apps, customer service channels, or even your bank statements, you can easily and securely obtain this crucial identifier without ever needing to touch a paper check. Armed with this knowledge and a commitment to security best practices, you can confidently navigate the modern financial landscape, ensuring your money goes exactly where it needs to be.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.