For many entrepreneurs, capital is the fuel that drives the engine of growth. Whether you are looking to bridge a seasonal cash flow gap, purchase high-value equipment, or expand your operations into new markets, securing a small business loan is often a pivotal milestone in a company’s lifecycle. However, the path to funding is frequently paved with complex requirements, rigorous financial scrutiny, and a multitude of options that can overwhelm even the most seasoned business owner.

Navigating the landscape of business finance requires a blend of strategic preparation and financial literacy. It is not merely about asking for money; it is about demonstrating that your business is a viable, low-risk investment for the lender. This guide breaks down the essential steps to obtaining a small business loan, focusing on the financial metrics, documentation, and strategic decision-making necessary to secure the capital your business needs to thrive.

Understanding Your Financing Needs and Loan Types

Before approaching a lender, you must have a crystalline understanding of why you need the capital and how you intend to repay it. Financial institutions categorize loans based on their purpose, duration, and the risk they pose to the lender. Selecting the wrong type of financing can lead to unnecessarily high interest rates or a debt structure that stifles your cash flow rather than helping it.

Traditional Term Loans vs. Lines of Credit

A traditional term loan is a lump sum of capital provided by a lender, which is repaid over a set period with a fixed or variable interest rate. These are best suited for specific, one-time investments such as purchasing real estate or a long-term expansion project. Because you receive the full amount upfront, you begin paying interest on the entire balance immediately.

In contrast, a business line of credit offers more flexibility. It provides access to a pool of funds that you can draw from as needed. You only pay interest on the amount you actually use. This is an ideal financial tool for managing short-term operational expenses, such as payroll during a slow month or purchasing inventory to prepare for a busy season. For many small businesses, having a line of credit is a vital safety net for maintaining liquidity.

SBA Loans: The Gold Standard for Small Businesses

The U.S. Small Business Administration (SBA) does not lend money directly to business owners. Instead, it provides a guarantee to partner lenders, promising to repay a portion of the loan if the borrower defaults. This reduced risk allows lenders to offer more favorable terms, lower interest rates, and longer repayment periods.

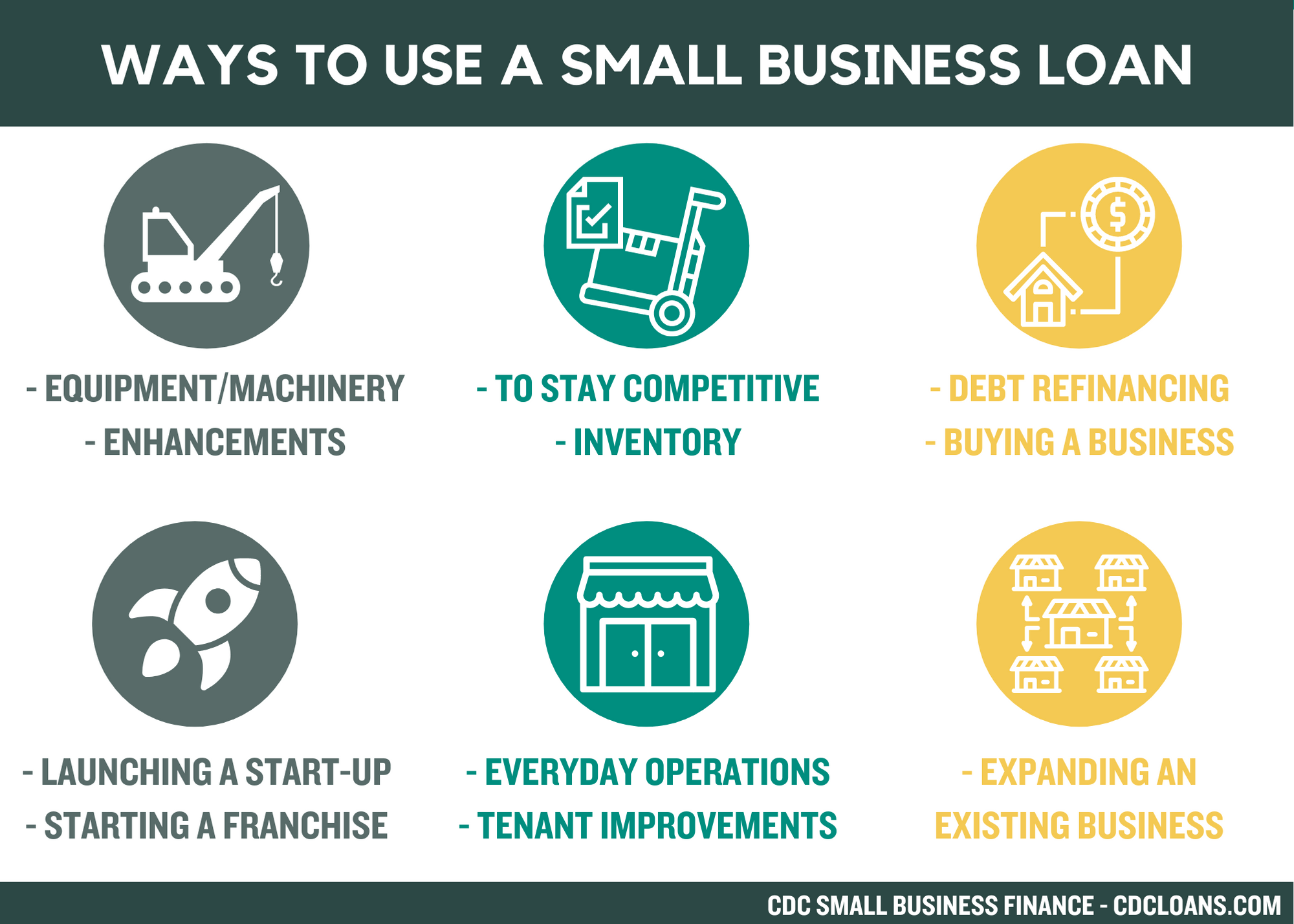

The SBA 7(a) loan is the most popular program, used for working capital, debt refinancing, or equipment. The SBA 504 loan is specifically designed for major fixed assets like land and machinery. While SBA loans are highly desirable due to their competitive financial terms, they also require extensive documentation and have a longer approval timeline compared to private lenders.

Alternative Financing: Equipment and Invoice Factoring

If your business lacks a long credit history but possesses significant physical or accounts receivable assets, alternative financing might be the most accessible route. Equipment financing uses the equipment itself as collateral, meaning if you default, the lender simply repossesses the machinery. This often makes the qualification process easier.

Invoice factoring (or accounts receivable financing) involves selling your unpaid invoices to a third party at a discount. While the effective “interest rate” can be higher than a traditional loan, it provides immediate cash flow for businesses that have reliable customers but long payment cycles.

Evaluating Your Financial Readiness and Creditworthiness

Lenders assess your loan application based on the “Five Cs of Credit”: Character, Capacity, Capital, Collateral, and Conditions. From a purely financial perspective, your creditworthiness is the most critical factor in determining whether you get approved and what interest rate you will pay.

The Importance of Personal and Business Credit Scores

For small business owners, your personal credit score is often as important as your business credit score. In the eyes of a lender, how you manage your personal finances is a strong indicator of how you will manage your business’s obligations. A personal FICO score above 680 is generally required for traditional bank loans, while SBA loans may require even higher scores.

Simultaneously, you must build your business credit profile. This involves registering your business as a legal entity, obtaining a D-U-N-S number, and ensuring that you pay your vendors and existing creditors on time. A strong business credit score demonstrates to the bank that the company is a distinct, reliable financial entity.

Analyzing Your Debt-to-Income and Debt Service Coverage Ratios

Lenders will perform a deep dive into your “capacity” to repay the loan. One of the most important metrics they use is the Debt Service Coverage Ratio (DSCR). This is calculated by dividing your business’s annual net operating income by its total annual debt payments.

A DSCR of 1.25 or higher is typically the benchmark for most lenders. It indicates that for every dollar of debt you owe, you have $1.25 in income to cover it. If your ratio is too low, it suggests that a slight dip in revenue could leave you unable to meet your loan obligations, making you a high-risk borrower.

Collateral Requirements and Personal Guarantees

Most small business loans are secured, meaning they require collateral—assets that the lender can seize if you fail to repay. Collateral can include real estate, inventory, equipment, or accounts receivable. The value of the collateral provides the lender with a “secondary source of repayment.”

In many cases, lenders also require a personal guarantee. This is a legal agreement stating that you, as the owner, are personally responsible for the debt if the business cannot pay. This bridges the gap for businesses that may not have enough corporate assets to fully secure a loan but have owners with strong personal financial standing.

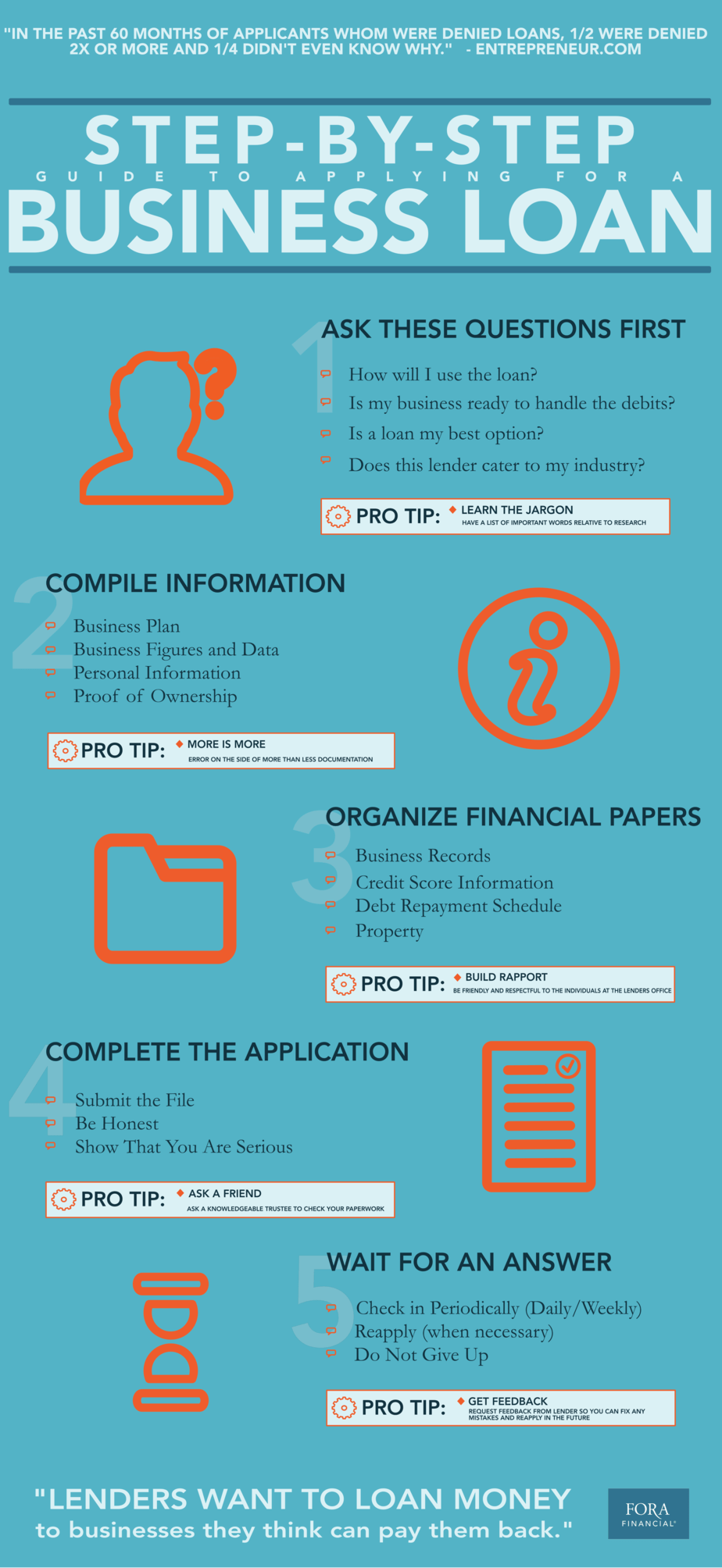

Preparing the Essential Documentation for a Successful Application

The application process for a small business loan is rigorous. Lenders require a high volume of documentation to verify your income, assess your business’s health, and ensure compliance with federal regulations. Organized financial records are often the difference between a swift approval and a rejection.

Crafting a Robust Business Plan

A business plan is more than just a roadmap; for a lender, it is a risk assessment tool. It should clearly outline your business model, target market, competitive landscape, and, most importantly, how the loan will be used to generate revenue. If you are borrowing money to buy new machinery, your business plan should quantify how that machinery will increase production and contribute to the bottom line.

Financial Statements: Balances, Profits, and Projections

You will need to provide at least two to three years of business financial statements. These include:

- Profit and Loss (P&L) Statement: Shows your revenue and expenses over time.

- Balance Sheet: Provides a snapshot of your assets, liabilities, and equity.

- Cash Flow Statement: Demonstrates how cash moves in and out of the business, proving you have the liquidity to make monthly loan payments.

Furthermore, lenders will want to see financial projections for the next 12 to 24 months. These projections must be realistic and backed by historical data or market research.

Legal and Tax Documentation Requirements

Expect to provide both personal and business tax returns for the last three years. Lenders use these to verify the income reported on your financial statements. Additionally, you will need to provide legal documents such as your Articles of Incorporation, business licenses, commercial leases, and any existing contracts with major clients or suppliers. This transparency allows the lender to ensure there are no legal encumbrances that could jeopardize your ability to repay the loan.

Navigating the Application Process and Choosing the Right Lender

Once your finances are in order and your documentation is ready, the final step is choosing where to apply. The source of your capital can significantly impact the speed of funding and the total cost of the loan.

Traditional Banks vs. Online Lenders

Traditional commercial banks and credit unions typically offer the lowest interest rates and the most favorable terms. However, they have the strictest eligibility requirements and the longest approval processes. They prefer established businesses with strong collateral and high credit scores.

Online lenders and fintech companies have revolutionized the lending space by prioritizing speed and accessibility. Using automated underwriting algorithms, they can often provide funding within days. The trade-off is that these loans often come with higher interest rates and shorter repayment terms. They are excellent for businesses that need capital quickly or those that may not meet the stringent criteria of a major bank.

The Underwriting and Approval Timeline

Underwriting is the process where the lender verifies all your information and assesses the risk. For a traditional bank or an SBA loan, this can take anywhere from a few weeks to several months. During this period, the lender may ask for clarifying information or additional documents. Being responsive and providing accurate data promptly can help expedite the process.

Comparing Interest Rates, Fees, and Terms

When comparing loan offers, looking at the interest rate alone is a mistake. You must evaluate the Annual Percentage Rate (APR), which includes the interest rate plus any fees (such as origination fees, processing fees, or closing costs).

Pay close attention to the repayment schedule and whether there are “prepayment penalties.” Some lenders charge a fee if you pay off the loan early, which can be a significant disadvantage if your business experiences a sudden windfall and you want to eliminate debt. By understanding the full financial impact of the loan terms, you can ensure that the capital you receive serves as a foundation for growth rather than a financial burden.

Securing a small business loan is a rigorous exercise in financial discipline. By understanding the various loan products, maintaining high credit standards, and preparing meticulous documentation, you position your business to gain the financial support necessary to achieve its long-term objectives.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.