Navigating the path to homeownership is often described as one of life’s most significant financial milestones. For many, the cornerstone of this journey is securing a mortgage loan – a complex yet essential financial product that bridges the gap between aspiration and reality. A mortgage is not merely a loan; it’s a long-term commitment that intertwines with your financial future, dictating your housing stability and influencing your wealth accumulation. Understanding the intricacies of how to obtain one is paramount for anyone contemplating the purchase of a home, whether it’s a first-time buyer embarking on a new adventure or an experienced homeowner looking to upgrade or relocate. This comprehensive guide aims to demystify the mortgage process, providing you with a professional, insightful, and engaging roadmap to securing the financing you need to unlock the doors to your dream home.

Understanding the Mortgage Landscape

Before diving into the application process, it’s crucial to grasp the fundamental concepts and players within the mortgage ecosystem. A clear understanding of these elements will empower you to make informed decisions and navigate the journey with confidence.

What is a Mortgage Loan?

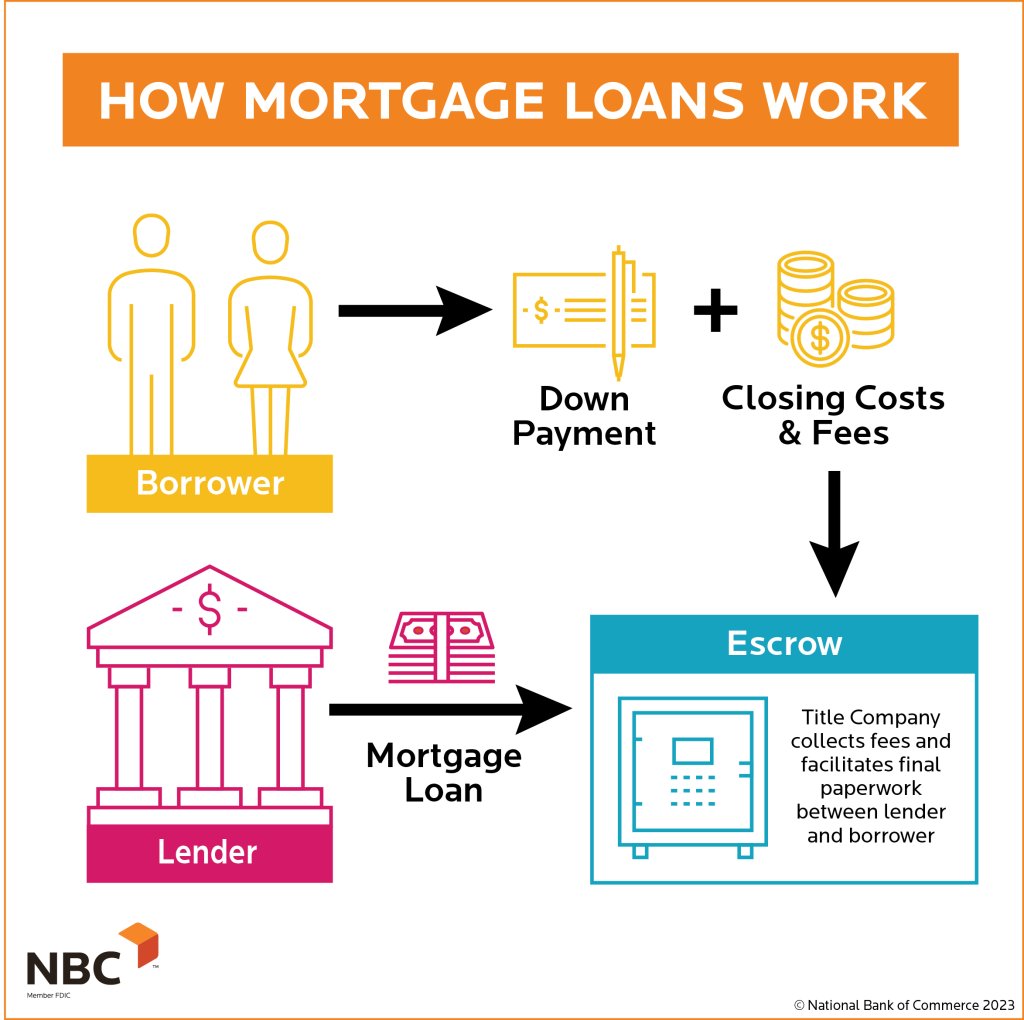

At its core, a mortgage loan is a secured loan used to purchase real estate. The property itself serves as collateral for the loan. This means that if you fail to repay the loan as agreed, the lender has the legal right to take possession of your home through a process known as foreclosure. Mortgages typically involve large sums of money, repaid over extended periods, often 15, 20, or 30 years, with interest. The payment you make each month usually consists of four main components, often referred to as PITI: Principal (the amount borrowed), Interest (the cost of borrowing), Taxes (property taxes), and Insurance (homeowner’s insurance, and sometimes private mortgage insurance or PMI).

Types of Mortgage Loans

The mortgage market offers a variety of loan products, each designed to cater to different financial situations and borrower needs. Choosing the right type is a critical decision that impacts your monthly payments, long-term costs, and eligibility.

- Conventional Loans: These are not insured or guaranteed by a government agency. They often require a good credit score and a down payment of at least 3% (though 20% is ideal to avoid PMI). They come in both fixed-rate and adjustable-rate varieties.

- Fixed-Rate Mortgages: The interest rate remains constant for the entire life of the loan. This provides predictable monthly payments, making budgeting easier and protecting you from rising interest rates.

- Adjustable-Rate Mortgages (ARMs): The interest rate is fixed for an initial period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on a predetermined index. ARMs can offer lower initial payments but carry the risk of higher payments if rates increase.

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular among first-time homebuyers and those with lower credit scores or smaller down payments (as little as 3.5%). They do require mortgage insurance premiums (MIP), both upfront and annually.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are available to eligible service members, veterans, and surviving spouses. They often require no down payment and no private mortgage insurance, making them highly advantageous.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans aim to promote homeownership in rural and eligible suburban areas. They typically require no down payment for qualifying borrowers and properties, but income limits apply.

Key Players in the Mortgage Process

Understanding who does what will help you navigate the process efficiently.

- Lenders: These are the financial institutions that provide the mortgage loan (e.g., banks, credit unions, online lenders).

- Mortgage Brokers: They act as intermediaries, connecting borrowers with various lenders to find the best rates and terms. They don’t lend money themselves but work on your behalf.

- Loan Officers: These professionals work directly for a lender or broker, guiding you through the application process and helping you choose a suitable loan product.

- Underwriters: These are the unsung heroes who meticulously review your application, financial documents, and property details to assess risk and determine if you meet the lender’s criteria for approval.

- Title Companies/Attorneys: They ensure that the property title is clear of liens and judgments, facilitate the transfer of ownership, and handle the closing process.

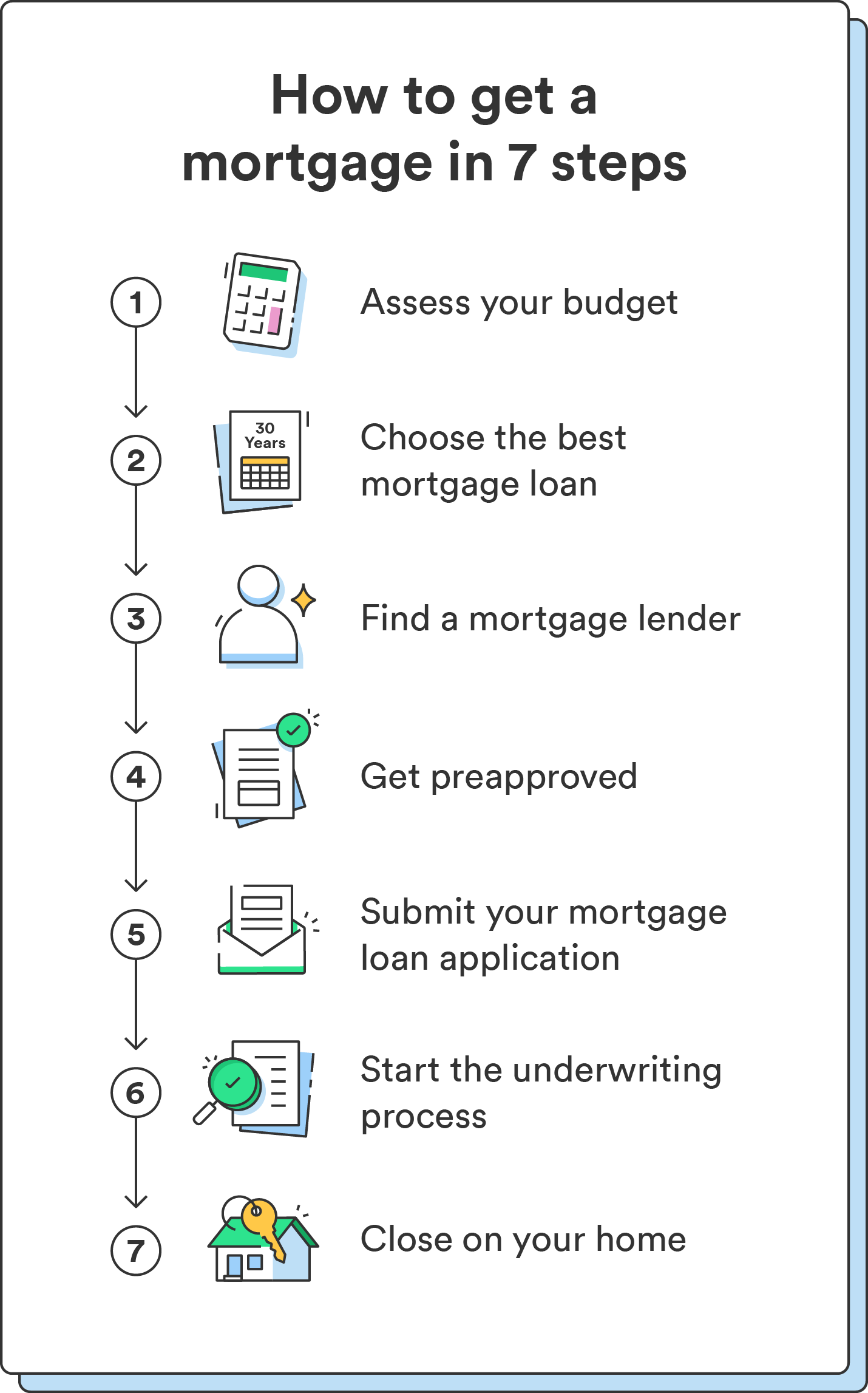

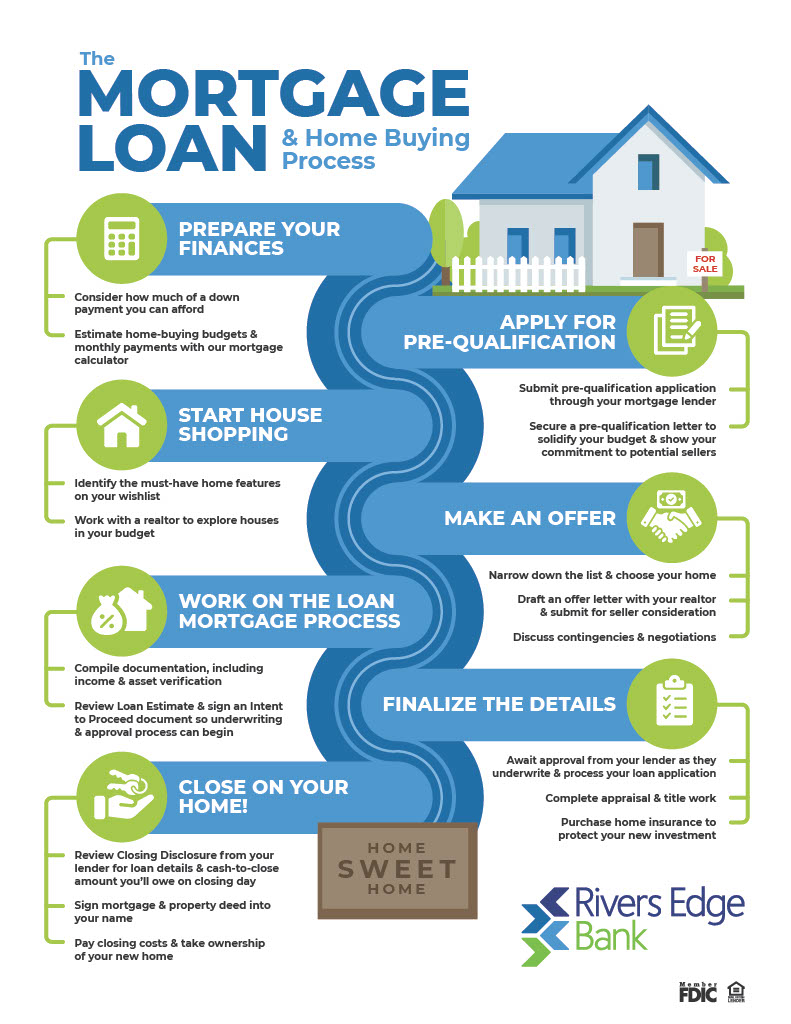

Preparing for Mortgage Pre-Approval

The journey to securing a mortgage officially begins long before you submit an application. Preparation is key, and getting pre-approved is a critical step that demonstrates your seriousness to sellers and gives you a clear budget.

Assessing Your Financial Health

Lenders scrutinize your financial stability to gauge your ability to repay the loan. Proactive self-assessment will highlight areas for improvement.

- Credit Score: Your credit score (FICO score) is a primary indicator of your creditworthiness. A higher score typically leads to lower interest rates. Aim for a score of 700 or above for the best rates, though some loans (like FHA) may accommodate lower scores. Review your credit report for inaccuracies and work to pay down debts, especially high-interest ones, to improve your score.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders generally prefer a DTI of 36% or less, though some programs allow up to 43-50%. A lower DTI indicates you have more disposable income to manage mortgage payments.

- Savings and Down Payment: Having a substantial down payment reduces the amount you need to borrow, lowers your monthly payments, and can help you avoid Private Mortgage Insurance (PMI) on conventional loans if you put down 20% or more. Lenders also look for reserve funds – typically 2-6 months’ worth of mortgage payments – to ensure you can cover expenses in case of an emergency.

Gathering Essential Documents

The mortgage application process is document-heavy. Getting organized early will save you time and stress. Prepare to gather the following:

- Income Verification: W-2 forms (for the past two years), pay stubs (most recent 30 days), tax returns (past two years if self-employed or if you have complex income streams). If self-employed, profit and loss statements will also be required.

- Asset Statements: Bank statements (checking and savings, past two months), investment account statements, and any other evidence of assets that can be used for your down payment and closing costs.

- Identification: Driver’s license or other government-issued ID, Social Security number.

- Employment History: A detailed two-year employment history, including contact information for previous employers.

- Debt Information: Statements for credit cards, auto loans, student loans, and any other outstanding debts.

Understanding Pre-Qualification vs. Pre-Approval

These terms are often used interchangeably but have significant differences.

- Pre-Qualification: This is an informal estimate of how much you might be able to borrow. It’s based on a quick review of your finances (often self-reported) and doesn’t involve a hard credit check. It’s a good starting point but holds little weight with sellers.

- Pre-Approval: This is a much more thorough process. A lender reviews your credit report (a hard pull), verifies your income and assets, and determines the maximum loan amount you qualify for, along with an estimated interest rate. A pre-approval letter is a conditional commitment from the lender and makes your offer far more attractive to sellers, indicating you are a serious and qualified buyer.

Navigating the Application and Underwriting Process

Once you’re pre-approved, the real work of finding a home begins. But even after your offer is accepted, there are crucial steps to take to finalize your mortgage.

Choosing the Right Lender

Don’t settle for the first lender you speak with. Shop around and compare offers from several different institutions – banks, credit unions, and online lenders. Look beyond just the interest rate; consider loan fees, closing costs, customer service, and the lender’s reputation. A slight difference in interest rate or fees can save you thousands of dollars over the life of the loan.

Submitting Your Application

With an accepted offer on a home, you’ll formally submit your full mortgage application to your chosen lender. This involves providing all the documents you gathered during the pre-approval phase, along with details about the specific property you intend to purchase. Your loan officer will guide you through this, ensuring all necessary forms are completed accurately.

The Underwriting Deep Dive

This is where the lender thoroughly vets your application. The underwriter will verify all information provided, scrutinize your credit history, income stability, assets, and liabilities. They assess the risk associated with lending to you and ensure that the loan meets both the lender’s guidelines and any applicable regulatory requirements. Be prepared for follow-up questions and requests for additional documentation; this is a normal part of the process. Transparency and prompt responses are key to a smooth underwriting experience.

Appraisal and Inspection: Protecting Your Investment

Simultaneously, the lender will order an appraisal of the property. An independent appraiser will assess the home’s value to ensure it’s at least equal to the purchase price, protecting the lender from over-lending and you from overpaying. Most buyers also hire a professional home inspector to evaluate the property’s condition, identify any potential issues (structural, mechanical, etc.), and provide peace of mind. While an inspection isn’t mandatory for the loan, it’s highly recommended to protect your investment.

From Approval to Closing Day

After successfully navigating underwriting, you’re on the home stretch. This final phase involves a series of critical steps leading up to the transfer of ownership.

Conditional Approval and Loan Commitment

Once underwriting is complete and all conditions are met, your lender will issue a conditional approval. This means your loan is approved, contingent on a few final items, which might include updated pay stubs, bank statements, or specific documentation related to the property. Once these conditions are satisfied, you’ll receive a loan commitment letter, signifying final approval.

Finalizing Documentation

Before closing, you’ll review and sign a mountain of paperwork. This includes the promissory note (your promise to repay the loan), the mortgage or deed of trust (which gives the lender the right to foreclose if you default), and numerous disclosures. Read everything carefully and ask questions about anything you don’t understand.

Understanding Your Closing Disclosure

The TILA-RESPA Integrated Disclosure (TRID) rule requires lenders to provide a Closing Disclosure (CD) at least three business days before your closing date. This crucial document details all the final terms of your loan, including interest rate, monthly payment, and all closing costs (lender fees, title fees, prepaid expenses, etc.). Compare it carefully with the Loan Estimate you received earlier to ensure there are no unexpected changes. This three-day window gives you time to ask questions and resolve any discrepancies.

The Big Day: What Happens at Closing?

Closing day is the culmination of your efforts. You, your lender representative, the seller, and the title company or attorney will meet to finalize the transaction. You’ll sign all the final paperwork, pay your remaining down payment and closing costs (usually via cashier’s check or wire transfer), and the lender will disburse the loan funds. Once everything is signed and funds are transferred, the deed will be recorded, and you’ll officially receive the keys to your new home!

Post-Closing Considerations

Securing your mortgage is a significant achievement, but the financial responsibilities of homeownership extend far beyond closing day. Proactive management of your mortgage can lead to substantial long-term financial benefits.

Managing Your Mortgage Payments

Consistency is key. Set up automatic payments to avoid late fees and protect your credit score. Understand your loan’s amortization schedule, which shows how your payments are allocated between principal and interest over time. Early in the loan term, a larger portion of your payment goes towards interest, but over time, more goes towards principal, building your equity.

Refinancing Opportunities

Interest rates fluctuate, and your financial situation may change. Keep an eye on market rates, as refinancing your mortgage could potentially lower your interest rate, reduce your monthly payments, shorten your loan term, or convert an ARM to a fixed-rate loan. However, weigh the costs of refinancing (closing costs, appraisal fees, etc.) against the potential savings.

Building Home Equity

As you pay down your mortgage principal and as property values appreciate, you build equity in your home. This equity represents your ownership stake and can be a valuable financial asset. It can be accessed later through a home equity loan or line of credit, or realized when you eventually sell your home. Making extra principal payments, even small ones, can significantly accelerate equity growth and reduce the total interest paid over the life of the loan.

Getting a mortgage loan is a journey that demands diligence, patience, and financial acumen. By understanding the process, preparing thoroughly, and engaging proactively with lenders and other professionals, you can confidently navigate the complexities and achieve the dream of homeownership, setting a strong foundation for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.