Obtaining a loan is often a pivotal moment in an individual’s or entrepreneur’s financial journey. Whether you are looking to consolidate high-interest debt, fund a major life event, purchase a home, or scale a business, the process of securing capital requires a blend of strategic preparation, financial literacy, and a clear understanding of the lending ecosystem. In today’s complex financial environment, “getting a loan” is no longer a simple matter of walking into a local bank and shaking hands with a manager. It involves navigating digital algorithms, credit scoring models, and a diverse array of lending products tailored to specific needs.

This guide provides an in-depth exploration of the borrowing process, categorized under the “Money” niche, focusing on personal and business finance strategies to ensure you not only get approved but secure the most favorable terms possible.

1. Decoding the Borrowing Landscape: Identifying the Right Loan for Your Needs

Before beginning an application, it is essential to understand that not all loans are created equal. The financial market offers a variety of structures, each with its own risk profile and cost. Identifying the correct category is the first step in a successful financial strategy.

Secured vs. Unsecured Loans

The most fundamental distinction in the lending world is between secured and unsecured debt. A secured loan requires collateral—an asset like a house, a car, or a savings account—that the lender can seize if you default on the loan. Because the lender’s risk is mitigated by the asset, these loans typically carry lower interest rates.

An unsecured loan, conversely, is granted based solely on your creditworthiness and promise to pay. Personal loans and credit cards fall into this category. Because there is no collateral, lenders charge higher interest rates to compensate for the increased risk of loss.

Fixed-Rate vs. Variable-Rate Financing

When you secure a loan, you must choose how interest is calculated. Fixed-rate loans offer stability; your interest rate remains the same throughout the life of the loan, making budgeting predictable. Variable-rate loans (or floating rates) are tied to market indices. While they may start lower than fixed rates, they can increase over time, potentially leading to significantly higher monthly payments if the central bank raises interest rates.

Purpose-Specific Loans

Lenders often offer specialized products. For instance, mortgages are designed specifically for real estate, while auto loans are tailored for vehicles. Student loans often come with government-backed protections and unique repayment terms. For entrepreneurs, SBA (Small Business Administration) loans provide a gateway to capital that might otherwise be unavailable through traditional commercial channels. Matching your need to the specific product often results in better terms and higher approval odds.

2. Building Your Financial Resume: The Prerequisites for Approval

Lenders view every applicant as a collection of data points that indicate the likelihood of repayment. To get a loan, you must present a “financial resume” that proves you are a low-risk borrower.

The Power of the Credit Score

In the world of personal finance, your credit score is your most valuable asset. Most lenders use FICO or VantageScore models to evaluate your history. A score above 740 is generally considered “excellent,” granting you access to the lowest interest rates. If your score is below 600, you may face “subprime” rates or outright rejection. Before applying, it is vital to review your credit report for errors and pay down existing revolving debt to improve your “credit utilization ratio,” which accounts for 30% of your FICO score.

Understanding the Debt-to-Income (DTI) Ratio

Even with a perfect credit score, a lender may deny your application if they believe you cannot afford the monthly payments. The Debt-to-Income (DTI) ratio is the percentage of your gross monthly income that goes toward paying debts. Most lenders prefer a DTI below 36%, though some mortgage products allow up to 43% or higher. To calculate this, divide your total monthly debt obligations by your gross monthly income. If your DTI is too high, you may need to increase your income or eliminate smaller debts before applying for a new loan.

Proof of Income and Employment Stability

Lenders seek consistency. Most personal and mortgage lenders require at least two years of steady employment history. If you are a freelancer or business owner, this “Money” niche requirement becomes more stringent. You will likely need to provide two years of tax returns, 1099s, and profit-and-loss (P&L) statements to prove that your income is not just sufficient, but sustainable.

3. The Modern Lending Marketplace: Where to Apply

The digital revolution has expanded the options for borrowers far beyond the traditional “Big Four” banks. Knowing where to look can save you thousands of dollars in interest over the life of a loan.

Traditional Banks and Credit Unions

Traditional banks offer the security of established institutions and the benefit of relationship banking. If you have been a long-time customer, you may receive preferential rates. Credit unions, which are member-owned non-profits, are often even better. Because they do not have to answer to shareholders, they frequently return profits to members in the form of lower loan rates and reduced fees.

Online Lenders and Fintechs

The rise of Financial Technology (Fintech) has streamlined the borrowing process. Online lenders like SoFi, Marcus, or Rocket Mortgage use advanced algorithms to provide instant pre-qualifications. These platforms often have lower overhead than physical banks, allowing them to offer competitive rates. They are particularly effective for personal loans and quick business lines of credit.

Peer-to-Peer (P2P) Lending

P2P lending platforms, such as Prosper or LendingClub, connect individual investors directly with borrowers. This “Money” sector innovation allows individuals to bypass traditional banking gatekeepers. If your credit profile is unique or if you are looking for a more personalized lending experience, P2P platforms can be a viable alternative, though rates vary significantly based on the risk grade assigned to your profile.

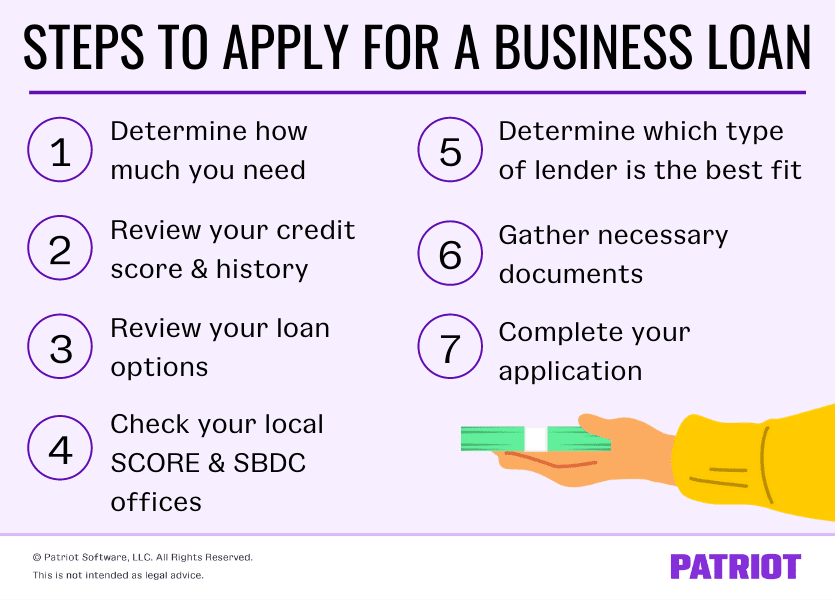

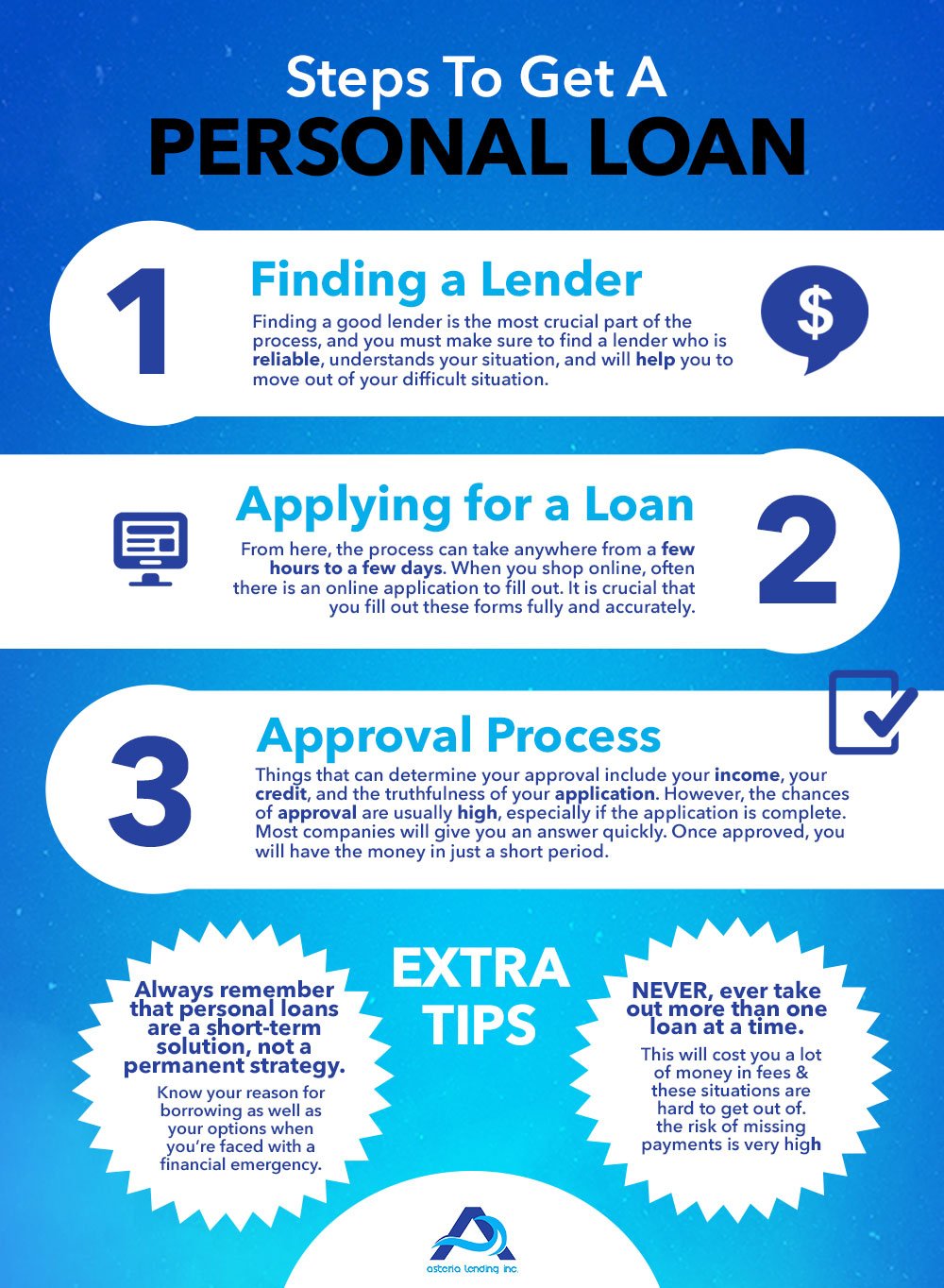

4. Navigating the Application Journey: A Step-by-Step Approach

Once you have identified the loan type and the lender, the application process begins. Navigating this stage with precision is key to avoiding delays or denials.

The Pre-Qualification Phase

Most modern lenders offer a “soft credit pull” pre-qualification. This allows you to see potential rates and loan amounts without affecting your credit score. Use this tool to shop around and compare the Annual Percentage Rate (APR)—which includes both the interest rate and any fees—across at least three different lenders.

Gathering the Documentation

When you move to a formal application, a “hard credit pull” will occur. At this stage, you must be prepared with a digital folder containing:

- Government-issued ID.

- Recent pay stubs (usually the last 30 days).

- W-2 forms or tax returns from the last two years.

- Bank statements (last 2–3 months) to prove liquidity.

- A list of current debts and monthly obligations.

The Underwriting and Funding Process

After submission, your application enters underwriting. This is the phase where the lender verifies all your information and assesses the risk. Be responsive; if an underwriter asks for a clarification on a specific bank deposit, providing that information quickly can be the difference between a 24-hour approval and a two-week delay. Once approved, you will sign the loan agreement, and funds are typically disbursed via ACH transfer within 1 to 5 business days.

5. Strategic Debt Management and Avoiding Pitfalls

Securing the loan is only half the battle; managing it responsibly is what ensures long-term financial health. In the “Money” niche, the goal is always to use leverage to increase net worth, not to diminish it.

Understanding the True Cost of Capital (APR)

Never look at the interest rate in isolation. The APR (Annual Percentage Rate) is the more accurate figure because it incorporates origination fees, processing fees, and other closing costs. A loan with a 5% interest rate and a 3% origination fee may actually be more expensive than a 6% interest rate loan with no fees. Always use the APR as your “apples-to-apples” comparison metric.

Avoiding Predatory Lending and High-Interest Traps

In your search for a loan, stay away from “payday loans” or “title loans.” These products often carry APRs exceeding 300% and are designed to trap borrowers in a cycle of debt. If a lender does not check your credit or promises “guaranteed approval,” it is a major red flag. Stick to reputable financial institutions and transparent online lenders.

The Repayment Blueprint

Once the funds are in your account, have a plan. Automate your payments to ensure you never miss a due date—this will further boost your credit score. If the loan is for debt consolidation, close the old accounts or stop using them to avoid “double-loading” your debt. If the loan is for a business, ensure the Return on Investment (ROI) from the capital exceeds the interest rate of the loan.

By understanding these five pillars—product selection, financial preparation, marketplace options, the application process, and long-term management—you transform the act of “getting a loan” from a stressful chore into a sophisticated financial maneuver. Leverage is a powerful tool in personal finance; when used correctly, it serves as the fuel for your economic growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.