Understanding the architecture of Social Security is a cornerstone of modern financial planning. For the vast majority of Americans, Social Security serves as a fundamental layer of retirement income, yet the actual mechanics behind the monthly check remain opaque to many. It is not a simple pension or a fixed-rate savings account; rather, it is a complex social insurance program that uses a specific formula to translate a lifetime of earnings into a monthly benefit.

Determining your benefit amount involves a multi-step process that accounts for inflation, your highest-earning years, and the age at which you choose to start receiving payments. By dissecting these components, individuals can make informed decisions about when to retire and how to supplement their Social Security income with private investments and personal savings.

The Foundation: Credits and the 35-Year Work History

The path to receiving Social Security benefits begins with the accumulation of “credits.” As of the current regulations, workers earn credits based on their annual earnings from employment or self-employment. In 2024, one credit is earned for every $1,730 of earnings, with a maximum of four credits per year. To qualify for retirement benefits, most workers need 40 credits, which translates to roughly ten years of work.

The Importance of the 35-Year Window

Once eligibility is established, the Social Security Administration (SSA) looks at your entire earnings history. However, the calculation does not average every year you have ever worked. Instead, it focuses exclusively on your 35 highest-earning years.

This specific timeframe is critical for several reasons:

- Filling the Gaps: If you have fewer than 35 years of covered earnings, the SSA fills the remaining years with zeros. These zeros can significantly drag down your career average, resulting in a lower monthly benefit.

- Replacing Lower Earnings: If you have worked for 40 years, the SSA will automatically drop the five lowest-earning years from the calculation. This ensures that your benefit is reflective of your peak productivity.

- Inflation Indexing: To ensure that earnings from 1985 are comparable to earnings in 2023, the SSA applies an indexing factor to your past wages. This “indexing” adjusts your historical earnings to reflect the general rise in wages that has occurred over your career, effectively bringing your past income into today’s dollar values.

The Math of the Benefit: From AIME to PIA

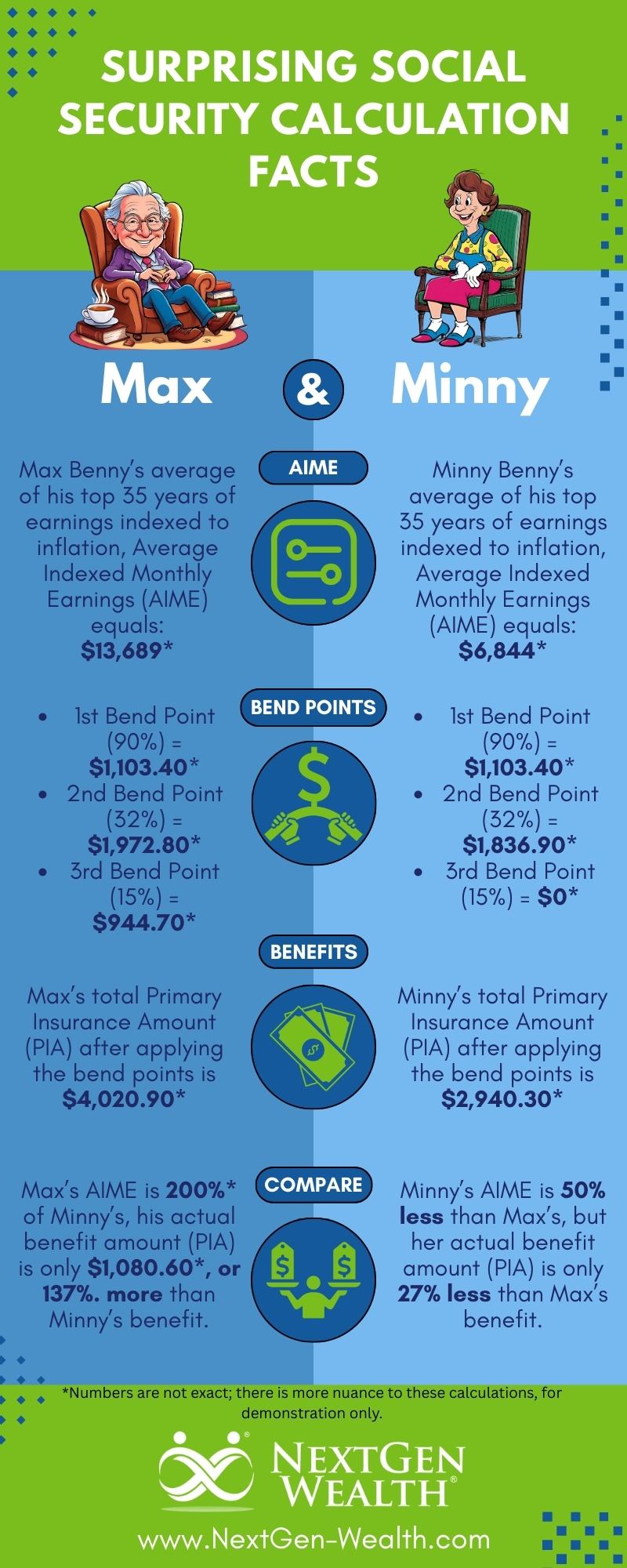

Once your 35 highest-earning years are identified and indexed for inflation, the SSA calculates your Average Indexed Monthly Earnings (AIME). This is done by summing the indexed earnings for those 35 years and dividing the total by 420 (the number of months in 35 years). The AIME represents your career-average monthly income, adjusted for the economy’s growth.

The Primary Insurance Amount (PIA) and Bend Points

The AIME is not your final benefit amount. Instead, it is passed through a progressive formula to determine your Primary Insurance Amount (PIA). The PIA is the base amount you would receive if you retired exactly at your Full Retirement Age (FRA).

The formula used to convert AIME to PIA is designed to be progressive, meaning it provides a higher “replacement rate” for lower-income workers than for higher-income workers. This is achieved through “bend points,” which are specific dollar thresholds that change annually. For a worker reaching age 62 in 2024, the formula is:

- 90% of the first $1,174 of AIME.

- 32% of AIME between $1,174 and $7,078.

- 15% of AIME over $7,078.

This tiered structure ensures a social safety net for those with lower lifetime earnings while still providing higher absolute benefits to those who contributed more to the system over their careers.

The Maximum Taxable Earnings Limit

It is also important to note that Social Security benefits are capped because the amount of income subject to Social Security taxes is capped. Each year, the SSA sets a “maximum taxable earnings” limit (for example, $168,600 in 2024). Any income earned above this threshold is not taxed for Social Security and, consequently, is not included in the AIME calculation. This creates a “ceiling” on the maximum possible benefit any individual can receive.

The Timing Factor: Full Retirement Age vs. Early or Delayed Filing

While the PIA sets the base benefit, the actual amount you receive is heavily influenced by when you choose to start collecting. The Social Security Administration designates a “Full Retirement Age” (FRA) based on your birth year. For those born in 1960 or later, the FRA is 67.

The Cost of Filing Early

You can choose to begin receiving benefits as early as age 62. However, doing so results in a permanent reduction of your monthly check. This reduction is calculated based on the number of months before your FRA that you begin receiving benefits.

- For the first 36 months of early filing, the benefit is reduced by 5/9 of 1% per month.

- For any months beyond 36, the benefit is further reduced by 5/12 of 1% per month.

For someone with an FRA of 67, filing at 62 results in a total permanent reduction of approximately 30%. While this provides immediate cash flow, it significantly reduces the total lifetime monthly income and the base upon which future inflation adjustments are calculated.

The Reward for Delayed Retirement

Conversely, if you delay receiving benefits beyond your FRA, the SSA rewards you with “Delayed Retirement Credits.” For every year you wait—up to age 70—your benefit increases by 8% per year.

This means that a person with an FRA of 67 who waits until 70 to file will receive 124% of their PIA. This is one of the most effective ways to “buy” a higher guaranteed, inflation-adjusted income stream for life. Once you reach age 70, there is no further incentive to delay, as the credits stop accumulating.

Spousal, Survivor, and Divorced Spouse Benefits

The determination of benefits extends beyond an individual’s own work record. The Social Security system is designed to provide financial security for families, leading to various derivative benefits.

Spousal Benefits

A spouse who has not worked or has lower lifetime earnings can receive a benefit based on their partner’s work record. The maximum spousal benefit is 50% of the worker’s PIA, provided the spouse waits until their own FRA to claim. It is important to note that a spouse claiming on their partner’s record does not reduce the primary worker’s benefit.

Survivor Benefits

In the event of a worker’s death, the surviving spouse may be eligible for survivor benefits. If the survivor has reached their own FRA, they can generally receive 100% of the deceased worker’s benefit (including any delayed retirement credits the worker had earned). This is a critical component of estate and legacy planning, particularly for couples with a significant disparity in lifetime earnings.

Divorced Spouse Benefits

If you were married for at least ten years and have been divorced for at least two years, you may be eligible to claim benefits based on your ex-spouse’s work record. The rules are similar to spousal benefits: you can receive up to 50% of their PIA, and claiming this benefit does not affect the ex-spouse’s benefit or the benefits of their current spouse.

External Influences: Taxes, COLA, and the Earnings Test

The final amount that actually lands in a retiree’s bank account can be affected by external economic factors and ongoing employment.

Cost-of-Living Adjustments (COLA)

To combat the eroding power of inflation, Social Security benefits are adjusted annually through the Cost-of-Living Adjustment (COLA). This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If prices rise, benefits rise. This feature is one of the most valuable aspects of Social Security, as few private annuities or pensions offer the same level of guaranteed inflation protection.

The Retirement Earnings Test

If you choose to work while receiving Social Security benefits before you reach your FRA, your benefits may be temporarily reduced if your earnings exceed certain thresholds. In 2024, the SSA withholds $1 in benefits for every $2 earned above $22,320. However, these withheld benefits are not “lost” forever; once you reach your FRA, the SSA recalculates your benefit amount upward to account for the months where benefits were withheld, effectively “repaying” you over time.

Taxation of Benefits

Depending on your total income, a portion of your Social Security benefits may be subject to federal income tax. This is determined by your “combined income,” which is the sum of your adjusted gross income, non-taxable interest, and half of your Social Security benefits.

- If your combined income is between $25,000 and $34,000 (individual) or $32,000 and $44,000 (joint), up to 50% of your benefits may be taxable.

- If your combined income exceeds these limits, up to 85% of your benefits may be taxable.

Strategic Financial Integration

Understanding how Social Security benefits are determined is not just an academic exercise; it is a vital part of comprehensive wealth management. By knowing the “bend points” and the impact of filing ages, individuals can better structure their retirement portfolios.

For instance, a high-earner might choose to draw down their taxable 401(k) or IRA assets between the ages of 62 and 70 to allow their Social Security benefit to grow by 8% annually. This strategy converts volatile market-based assets into a higher, guaranteed, inflation-linked lifetime floor.

Ultimately, Social Security is a formulaic reflection of your contribution to the American economy. While the variables of work history, indexing, and filing age can seem daunting, they provide a structured framework for ensuring that every worker has a baseline of financial dignity in their later years. Navigating these rules with precision is the difference between a standard retirement and one optimized for maximum financial security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.