For anyone managing their personal finances, understanding the various security features of their debit card is paramount. Among these, the security code plays a pivotal role in protecting your funds and authorizing transactions, particularly in the digital realm. Often referred to by different names, this code is a vital layer of defense against financial fraud, ensuring that only the legitimate cardholder can make purchases or access services.

Decoding Your Debit Card’s Security Measures

The security code on a debit card is a unique set of numbers designed to verify that the person attempting to make a purchase actually possesses the physical card. It serves as a critical safeguard against unauthorized use, especially in scenarios where the card itself isn’t physically present, such as online shopping or phone orders.

The Card Verification Value (CVV) / Card Security Code (CSC)

While commonly known as the CVV (Card Verification Value), this security code goes by several names depending on the card network. Visa refers to it as CVV2, MasterCard as CVC2 (Card Validation Code), American Express as CID (Card Identification Number), and Discover as CID. Regardless of the acronym, its purpose remains consistent: to add an extra layer of protection for card-not-present transactions. Unlike your Personal Identification Number (PIN), which authenticates transactions at ATMs or point-of-sale terminals where the card is swiped or inserted, the security code is exclusively used for verifying the card itself in remote transactions. It is not stored by merchants after a transaction, further enhancing its security function.

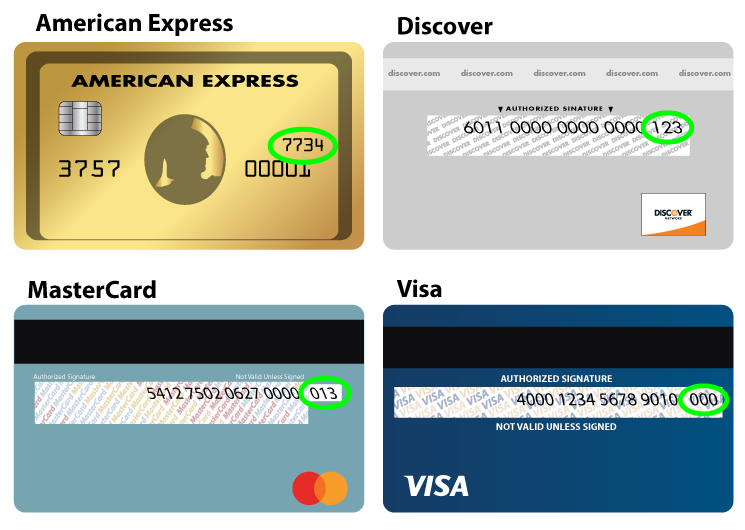

Location and Formats

The security code’s placement and length can vary slightly across different card types:

- Visa, MasterCard, and Discover Cards: On these cards, the security code is typically a three-digit number found on the back of the card, usually within or adjacent to the signature strip. It’s often printed in a distinct area, sometimes after the last four digits of the main card number.

- American Express Cards: For American Express, the security code is a four-digit number located on the front of the card, positioned above the main card number on either the right or left side.

It’s crucial to be able to quickly locate this code, as you’ll often be prompted for it during online purchases or when providing card details over the phone. Familiarity with its location on your specific debit card type is a small but important step in efficient and secure financial management.

Why it Matters for Your Funds

The security code is a non-embossed number, meaning it’s flat-printed rather than raised like the card number. This design choice makes it difficult for fraudsters to capture the code using common card-skimming devices that typically read embossed numbers. By requiring this code for online transactions, financial institutions and merchants aim to confirm that the person placing the order has legitimate physical access to the card. This significantly reduces the risk of fraud where only the primary card number, expiration date, or cardholder name might have been compromised, but not the physical card itself. For the individual, understanding and safeguarding this code directly translates to the protection of their deposited funds and overall financial security.

The Critical Role of the Security Code in Personal Finance

The security code isn’t just a random set of numbers; it’s a cornerstone of modern financial security protocols, particularly relevant in an increasingly digital economy. Its function directly impacts how individuals safely manage their money and conduct transactions without physical cash or traditional in-person verification.

Authorizing Online Purchases

The most frequent interaction individuals have with their debit card’s security code is during online shopping. When you enter your debit card number, expiration date, and name, the final piece of verification required by most secure websites is the security code. This step serves as an essential authentication factor, confirming that you, the legitimate cardholder, are physically holding the card. Without this code, an online transaction cannot be completed, effectively blocking anyone who might have stolen your primary card details but not the physical card itself. For individuals relying on online platforms for everything from groceries to bill payments, this code is the digital handshake that secures their financial information.

Protecting Against Card-Not-Present Fraud

Card-not-present (CNP) fraud is a significant concern for both consumers and financial institutions. This type of fraud occurs when a transaction is made without the physical card being present – typical of online, mail, or telephone orders. The security code was specifically introduced to combat CNP fraud. By demanding this code, merchants and banks ensure a higher level of confidence that the transaction is legitimate. If a fraudster obtains your card number and expiry date through data breaches but doesn’t have the security code, they will be unable to complete most online purchases. This mechanism saves cardholders from the financial headache of unauthorized charges and the time-consuming process of disputing transactions and recovering funds. It’s a proactive measure that empowers cardholders to protect their personal finances from remote theft.

Distinguishing from PIN

It is vital to understand the difference between your debit card’s security code and your Personal Identification Number (PIN). While both are crucial for security, they serve entirely different purposes and operate in distinct environments:

- PIN (Personal Identification Number): This is typically a four-digit code known only to you. It is used to authenticate transactions where your physical card is present, such as withdrawing cash from an ATM, making purchases at a point-of-sale terminal, or using a chip card reader. When you use your PIN, you are proving your identity as the cardholder. The PIN is transmitted securely and never printed on the card.

- Security Code (CVV/CVC/CID): This is a three or four-digit code printed on your card. It is never used for ATM withdrawals or in-person chip/swipe transactions. Its sole purpose is to verify that you have the physical card in your possession during card-not-present transactions (online, phone, mail orders). It authenticates the card, not necessarily the cardholder’s identity in the same way a PIN does.

Confusing these two can lead to insecure practices. For example, never share your PIN with anyone or write it down. While you might provide your security code to a trusted merchant for an online purchase, you would never provide your PIN. Keeping these distinctions clear is fundamental to robust personal financial security.

Best Practices for Safeguarding Your Debit Card Security Code

Given the critical role of the security code in protecting your financial assets, adopting diligent safeguarding practices is non-negotiable. Proactive measures can prevent unauthorized access to your funds and save you from the stress and expense of dealing with fraud.

Memorization vs. Written Records

Ideally, you should memorize your debit card’s security code. This eliminates the need to write it down, which inherently creates a security risk. If memorization isn’t feasible, exercise extreme caution if you feel compelled to record it. Never write the code directly on the card itself, nor store it alongside your card number or other identifying information. If you must write it down, do so in a discreet, encrypted, or highly secure location, completely separate from the physical card or any digital records of your card number. Many financial experts advise against writing down any sensitive card information at all. The goal is to make it as difficult as possible for someone to obtain both your card details and the security code simultaneously.

Online Shopping Security Tips

When using your debit card for online purchases, several practices can significantly enhance the security of your security code:

- Use Reputable Websites: Only enter your card details, including the security code, on trusted and secure websites. Look for “https://” in the website address and a padlock icon in the browser’s address bar. These indicators signify that the connection is encrypted, protecting your data during transmission.

- Avoid Public Wi-Fi for Transactions: Public Wi-Fi networks are often unsecured and can be susceptible to eavesdropping by malicious actors. Refrain from making purchases or entering sensitive financial information when connected to public Wi-Fi. Use a secure home network or cellular data instead.

- Be Wary of Phishing Attempts: Never click on suspicious links in emails or text messages that ask for your debit card details or security code. Legitimate banks and merchants will rarely ask for this information directly via unsolicited communications. Always navigate directly to the official website.

- Use Strong Passwords and Two-Factor Authentication (2FA): Where available, enable 2FA on your online shopping accounts. This adds an extra layer of security, typically requiring a code sent to your phone or email in addition to your password, even if your login credentials are compromised.

Vigilance Against Phishing and Skimming

Phishing and skimming are two common methods fraudsters use to steal card information.

- Phishing: This involves deceptive communication (emails, texts, fake websites) designed to trick you into revealing sensitive information. Be skeptical of any request for your security code, card number, or PIN that seems out of the ordinary or comes from an unfamiliar source. Verify the sender’s identity through official channels if in doubt.

- Skimming: While primarily targeting physical card numbers and PINs at ATMs or point-of-sale terminals, some advanced skimming devices might attempt to capture card details. Regularly inspect card readers and ATMs for any signs of tampering before inserting your card. Report any suspicious devices immediately.

Maintaining a high level of awareness and practicing caution are your best defenses against these tactics, ensuring your security code and ultimately your funds remain protected.

When Your Security Code is Compromised: Immediate Financial Steps

Despite your best efforts, financial fraud can occur. Knowing what to do immediately after discovering your debit card security code (or any other card detail) has been compromised is crucial to minimizing financial damage and restoring your personal financial security.

Recognizing Suspicious Activity

The first step is to identify that something is amiss. This often comes from:

- Unexpected Transaction Alerts: Many banks offer SMS or email alerts for every transaction. Enroll in these services. Any transaction you don’t recognize, especially a small test charge, could indicate compromise.

- Unfamiliar Charges on Statements: Regularly review your bank statements and online transaction history. Look for any purchases, withdrawals, or transfers you did not authorize. Even small, seemingly insignificant charges should raise a red flag.

- Notifications from Your Bank: Your financial institution may detect unusual activity and contact you. Always verify the authenticity of such communications before providing any information, preferably by calling the number on the back of your card directly.

Prompt detection is vital, as fraudulent charges can escalate quickly if not addressed immediately.

Reporting to Your Financial Institution

If you suspect your security code or any part of your debit card information has been compromised, contact your bank immediately. Most banks have a dedicated fraud department available 24/7. Use the customer service number provided on the back of your debit card or on your bank’s official website. When reporting:

- Be Prepared with Information: Have your account number, the details of any suspicious transactions, and the date and time you first noticed the issue ready.

- Request Card Cancellation: Ask your bank to immediately cancel the compromised debit card to prevent any further unauthorized transactions.

- Inquire About a New Card: Your bank will likely issue you a new card with a new number and security code.

- Understand Your Liability: Most financial institutions offer zero-liability policies for unauthorized debit card use, provided you report the fraud promptly. However, there might be time limits for reporting to qualify for full protection, so acting fast is critical for personal finance protection.

Monitoring Your Accounts and Credit

Reporting the compromise is the first step, but ongoing vigilance is also necessary:

- Continue Monitoring Your Bank Accounts: For several weeks or months after the incident, meticulously review your bank statements and online activity to ensure no new unauthorized charges appear. Fraudsters sometimes hold onto compromised details and attempt new charges later.

- Check Your Credit Report: While debit card fraud doesn’t directly impact your credit score like credit card fraud, identity thieves who gain access to your debit card details might attempt to open new accounts in your name, which would affect your credit. Obtain free copies of your credit report from AnnualCreditReport.com and review them for any unfamiliar accounts or inquiries.

- Change Passwords: If you used the compromised debit card on any online shopping sites, change the passwords for those accounts, especially if you reuse passwords across multiple platforms. Consider changing your online banking password as well, just as an extra precaution.

Taking these immediate and ongoing steps can significantly mitigate the financial and personal impact of a compromised debit card security code, reinforcing your overall financial stability.

The Evolving Landscape of Debit Card Security

The world of personal finance is in constant motion, and with it, the methods for securing debit cards are continually evolving. While the security code remains a fundamental layer of protection, it is increasingly supplemented by newer technologies designed to combat sophisticated fraud tactics and enhance transaction security.

EMV Chips and Contactless Payments

The introduction of EMV (Europay, MasterCard, Visa) chip technology marked a significant leap forward in debit card security. Unlike the magnetic stripe, which carries static data that can be easily copied, EMV chips generate a unique, encrypted code for each transaction. This “tokenization” makes it extremely difficult for fraudsters to create counterfeit cards from stolen data, virtually eliminating in-card-present fraud (i.e., when a physical card is used in a store).

Contactless payment technologies, such as “tap-to-pay” features found in many modern debit cards, also leverage EMV chip technology. When you tap your card, the transaction data is encrypted and transmitted securely using Near Field Communication (NFC). This method is often more secure than swiping a magnetic stripe because the card never leaves your hand and the data transmitted is unique for each transaction. For personal finance, this means greater peace of mind when making in-store purchases, as the risk of physical skimming is significantly reduced.

Tokenization and Advanced Encryption

Beyond the EMV chip, tokenization is becoming a broader strategy in digital security. When you store your debit card details with an online merchant or use a digital wallet (like Apple Pay or Google Pay), your actual 16-digit card number is often replaced by a unique, randomly generated “token.” This token is then used for transactions, instead of your real card number. If a merchant’s database is breached, the fraudsters only get access to these tokens, which are useless outside that specific merchant or payment ecosystem. This dramatically reduces the impact of data breaches on your personal financial security.

Advanced encryption standards are also continually being developed and implemented to protect data during transmission. From the moment you enter your security code online to when it’s processed by your bank, multiple layers of encryption ensure that your sensitive financial information remains unreadable to unauthorized parties. These behind-the-scenes technologies work in concert with visible security features like the security code to provide robust protection for your funds.

Balancing Convenience with Robust Protection

The ongoing challenge for financial institutions and payment networks is to strike a balance between providing robust security and maintaining convenience for cardholders. While numerous security layers exist, each additional step can potentially add friction to the transaction process. The debit card security code, for example, is a simple, effective, and relatively unintrusive security measure that has stood the test of time for card-not-present transactions.

As personal finance increasingly moves towards digital platforms, the reliance on a multi-layered security approach will only grow. This includes not just the physical security code, but also biometric authentication (fingerprints, facial recognition), behavioral analytics (monitoring spending patterns for anomalies), and real-time fraud detection systems. For the individual, staying informed about these advancements and adopting best practices in managing their debit cards remains key to navigating the financial landscape securely and confidently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.