Investing in the S&P 500 is a popular and often recommended strategy for those looking to gain diversified exposure to the U.S. stock market. As a benchmark for the performance of 500 of the largest publicly traded companies in the United States, it represents a significant portion of the total market value. While you can’t “buy” the S&P 500 index directly like a single stock, you can easily invest in financial products designed to track its performance. This guide will walk you through the essential steps and considerations for adding the S&P 500 to your investment portfolio, providing a professional, insightful, and engaging roadmap for your financial journey.

Understanding the S&P 500 Index and Its Appeal

Before diving into how to invest, it’s crucial to grasp what the S&P 500 truly represents and why it’s such a compelling investment vehicle for millions worldwide.

What is the S&P 500?

The S&P 500, or Standard & Poor’s 500, is a stock market index that represents the performance of 500 of the largest U.S. publicly traded companies by market capitalization. Compiled by S&P Dow Jones Indices, it is a market-capitalization-weighted index, meaning companies with larger market values have a greater impact on the index’s performance. It’s widely regarded as one of the best gauges of large-cap U.S. equities and a leading indicator for the U.S. economy.

The companies included in the S&P 500 span across all major sectors of the economy, including technology, healthcare, financials, consumer discretionary, industrials, and more. This broad representation provides inherent diversification, reducing the risk associated with investing in individual stocks. Rather than putting all your eggs in one basket, an S&P 500 investment spreads your capital across hundreds of industry leaders. The committee that selects the companies ensures they meet specific criteria for size, liquidity, and public float, making it a robust and representative collection of America’s corporate giants.

Why Invest in the S&P 500?

The appeal of the S&P 500 as an investment strategy is multifaceted, drawing in both novice and seasoned investors.

Firstly, diversification is perhaps its most significant advantage. By investing in a product that tracks the S&P 500, you are instantly diversified across 500 companies in various industries. This dramatically reduces company-specific risk; if one company performs poorly, its impact on your overall investment is minimal due to the broad exposure.

Secondly, the S&P 500 has a strong historical track record of long-term growth. While past performance is not indicative of future results, the index has delivered an average annual return of approximately 10-12% over various extended periods, including dividends. This consistent long-term appreciation makes it an attractive option for wealth accumulation, particularly for retirement planning or other long-term financial goals.

Thirdly, investing in the S&P 500 is a form of passive investing. This means you’re not actively picking individual stocks or trying to time the market. Instead, you’re betting on the overall growth and resilience of the U.S. economy and its leading companies. This approach often leads to lower fees compared to actively managed funds and requires less time and effort from the investor. It allows you to participate in market growth without needing to be an expert stock picker.

Finally, its accessibility is a major draw. Through various investment vehicles, which we will explore next, investing in the S&P 500 has become simpler and more affordable than ever before, democratizing access to broad market participation.

The Primary Ways to Invest in the S&P 500

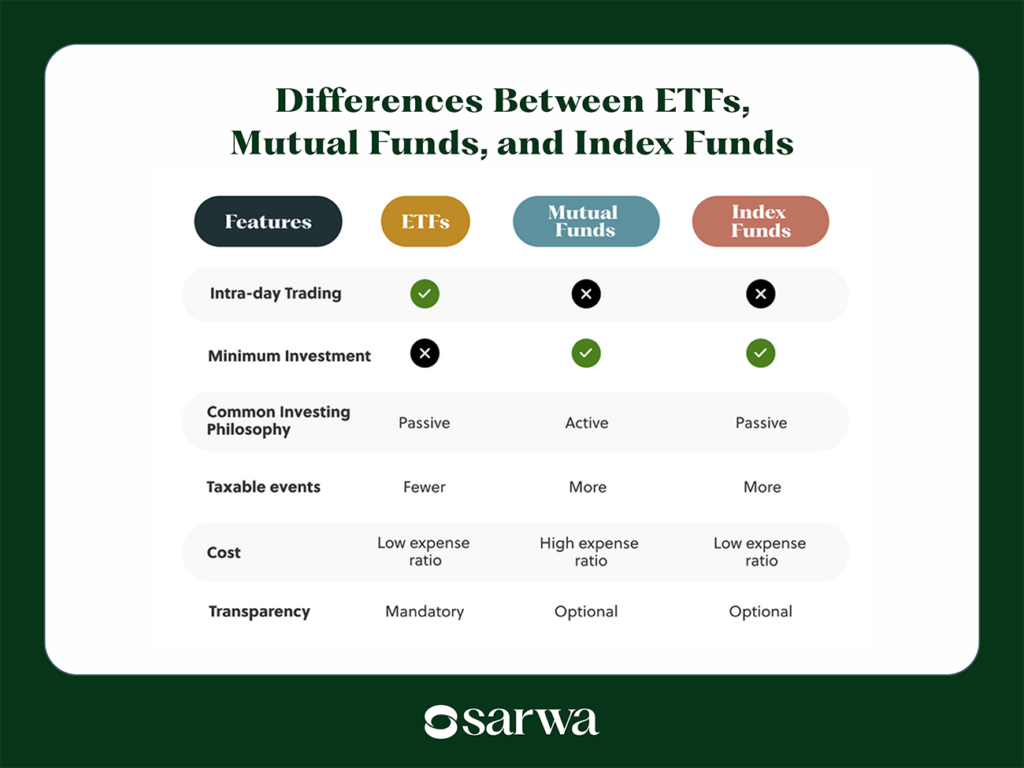

Since you cannot purchase the S&P 500 index directly, you invest in financial products designed to mirror its performance. The two most common and effective ways to do this are through Exchange-Traded Funds (ETFs) and Index Mutual Funds. Both offer similar benefits but have distinct operational differences.

S&P 500 Exchange-Traded Funds (ETFs)

Exchange-Traded Funds (ETFs) are investment funds that hold assets such as stocks, commodities, or bonds, and their value changes throughout the day just like a stock. ETFs tracking the S&P 500 aim to replicate the index’s performance by holding a portfolio of stocks in the same proportion as the index.

How They Work: When you buy an S&P 500 ETF, you are essentially buying a tiny share of all 500 companies in the index. The ETF provider (e.g., Vanguard, BlackRock, State Street) manages the fund, ensuring its holdings accurately reflect the S&P 500.

Advantages of S&P 500 ETFs:

- Liquidity: ETFs can be bought and sold throughout the trading day at market prices, offering flexibility that mutual funds do not.

- Low Expense Ratios: Because they are passively managed (they simply track an index rather than having fund managers actively picking stocks), S&P 500 ETFs typically have very low expense ratios, often below 0.10% annually. This means more of your money stays invested and growing.

- Diversification: Instant diversification across 500 companies with a single purchase.

- Accessibility: Most ETFs can be purchased with relatively small amounts of capital, often just the price of one share. Many brokers now offer fractional shares, making them even more accessible.

- Tax Efficiency: ETFs often have a more tax-efficient structure compared to traditional mutual funds, particularly regarding capital gains distributions.

Popular S&P 500 ETFs:

- SPDR S&P 500 ETF Trust (SPY): One of the oldest and most traded ETFs, managed by State Street Global Advisors.

- iShares Core S&P 500 ETF (IVV): Managed by BlackRock, known for its low expense ratio.

- Vanguard S&P 500 ETF (VOO): Managed by Vanguard, also noted for its extremely low expense ratio and broad appeal.

S&P 500 Index Mutual Funds

S&P 500 index mutual funds are another excellent way to gain exposure to the index. Similar to ETFs, these funds hold all the stocks that comprise the S&P 500 in the appropriate proportions, aiming to match the index’s performance.

How They Work: Unlike ETFs, mutual funds are bought and sold at their Net Asset Value (NAV) once per day, after the market closes. When you invest, you buy shares of the fund, which then uses your money (along with other investors’ money) to purchase the underlying stocks.

Advantages of S&P 500 Index Mutual Funds:

- Automatic Reinvestment: Many mutual funds offer automatic dividend reinvestment, allowing your earnings to compound effortlessly.

- Simplicity for Dollar-Cost Averaging: Their once-a-day pricing makes them ideal for automated, regular investments (e.g., investing a fixed amount every month), a strategy known as dollar-cost averaging.

- Broad Diversification: Like ETFs, they offer instant, broad diversification across the S&P 500.

- Professional Management (Passive Tracking): The fund manager ensures the fund accurately tracks the index, rebalancing as needed.

- Accessibility: While some may have higher minimum initial investment requirements than a single ETF share, many providers offer low minimums or waive them for automated investments.

Popular S&P 500 Index Mutual Funds:

- Vanguard 500 Index Fund Admiral Shares (VFIAX): A flagship fund from Vanguard, known for its low costs.

- Fidelity 500 Index Fund (FXAIX): Fidelity’s comparable offering, also with a very low expense ratio.

- Schwab S&P 500 Index Fund (SWPPX): Charles Schwab’s low-cost S&P 500 index fund.

When choosing between an ETF and a mutual fund, consider your preferred trading style (intraday trading vs. end-of-day), minimum investment requirements, and whether you prefer automating your investments. For most long-term investors, both options are excellent choices, often differing primarily in their structure and how they are bought and sold.

Opening an Investment Account

Regardless of whether you choose an S&P 500 ETF or an index mutual fund, the first practical step is to open an investment account with a reputable brokerage firm. This account will serve as the gateway to your investments.

Choosing a Brokerage Firm

The landscape of brokerage firms is diverse, offering various features, fee structures, and tools. Your choice will depend on your specific needs, experience level, and how much assistance you desire.

Types of Brokerage Firms:

- Online Discount Brokerages: These firms cater to self-directed investors, offering low-cost or commission-free trades for stocks and ETFs. They provide robust online platforms, research tools, and educational resources. Examples include Fidelity, Vanguard, Charles Schwab, E*TRADE, TD Ameritrade (now Schwab), and Robinhood.

- Robo-Advisors: If you prefer a more hands-off approach, robo-advisors (e.g., Betterment, Wealthfront) use algorithms to build and manage diversified portfolios based on your risk tolerance and financial goals. They typically invest in a mix of low-cost ETFs, including S&P 500 trackers.

- Full-Service Brokerages: These firms offer personalized financial advice, wealth management services, and a wide range of products, but typically come with higher fees or commissions. They are suited for investors who prefer direct human guidance.

Factors to Consider When Choosing:

- Fees and Commissions: Look for firms that offer commission-free trading for ETFs and low expense ratios for mutual funds.

- Investment Options: Ensure the brokerage offers the specific S&P 500 ETFs or mutual funds you’re interested in, as well as any other investment products you might want to explore in the future.

- Research Tools and Educational Resources: A good brokerage provides comprehensive research, market analysis, and learning materials to help you make informed decisions.

- Customer Service: Responsive and helpful customer support is invaluable, especially for new investors.

- Platform User Experience: An intuitive and easy-to-navigate platform enhances your investing experience.

- Account Minimums: Some firms have minimum deposit requirements, though many discount brokers now offer no minimums.

Selecting the Right Account Type

Once you’ve chosen a brokerage, you’ll need to decide on the type of investment account to open. This decision has significant implications for taxes and your financial goals.

Common Account Types:

- Taxable Brokerage Accounts: These are general investment accounts where your contributions are made with after-tax money, and any investment gains (dividends, interest, capital gains) are subject to taxes in the year they are realized. They offer maximum flexibility as there are no contribution limits or restrictions on withdrawals.

- Retirement Accounts: These accounts offer tax advantages designed to encourage long-term saving for retirement.

- Individual Retirement Accounts (IRAs):

- Traditional IRA: Contributions may be tax-deductible, and your investments grow tax-deferred. You pay taxes on withdrawals in retirement.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are tax-free.

- Employer-Sponsored Plans (e.g., 401(k), 403(b)): If your employer offers a retirement plan, you might be able to invest in S&P 500 index funds or ETFs through your plan’s investment options. These often come with employer matching contributions, which are essentially free money.

- Individual Retirement Accounts (IRAs):

- Other Specialized Accounts: You might also consider 529 college savings plans for education expenses or custodial accounts (UGMA/UTMA) for minors, though these are more niche applications.

Steps to Open an Account:

- Online Application: Most brokerages allow you to open an account entirely online. You’ll need to provide personal information (name, address, Social Security number), employment details, and financial information.

- Identity Verification: You’ll typically need to upload copies of identification documents (e.g., driver’s license, passport).

- Fund Your Account: Once approved, you can fund your account through various methods, including electronic bank transfers (ACH), wire transfers, or mailing a check.

Making Your First S&P 500 Investment

With your account open and funded, you’re ready to make your first investment. This process is straightforward but requires a little research and strategic thinking.

Researching and Selecting Your Fund

While many S&P 500 tracking funds perform similarly, subtle differences can impact your long-term returns.

Key Factors to Evaluate:

- Expense Ratio: This is the annual fee charged by the fund as a percentage of your investment. For S&P 500 index funds and ETFs, look for expense ratios below 0.10%. Over decades, even small differences in expense ratios can amount to significant sums.

- Tracking Error: This measures how closely the fund’s performance matches the actual index. Lower tracking error is better. Reputable funds generally have very low tracking errors.

- Assets Under Management (AUM): Larger funds often benefit from economies of scale, leading to lower operating costs.

- Fund Provider Reputation: Stick with well-established and respected fund providers like Vanguard, Fidelity, BlackRock (iShares), or State Street (SPDR).

- Tax Efficiency: Consider how dividends are handled and the fund’s turnover rate, which can affect capital gains distributions. ETFs are often more tax-efficient than traditional mutual funds for taxable accounts.

For most investors, a simple, low-cost S&P 500 ETF (like VOO, IVV, or SPY) or an S&P 500 index mutual fund (like VFIAX or FXAIX) offered by a major brokerage will suffice.

Placing Your Order

Once you’ve selected your fund, you’ll navigate to the trading section of your brokerage account.

Key Order Types:

- Market Order: This instructs your broker to buy or sell shares immediately at the best available current market price. While simple, the price you get might be slightly different from what you see due to rapid market fluctuations.

- Limit Order: This allows you to specify the maximum price you’re willing to pay (for buying) or the minimum price you’re willing to accept (for selling). Your order will only execute if the stock reaches your specified price. For long-term S&P 500 investments, a market order is often acceptable due to the funds’ high liquidity and relatively stable price movement, but a limit order can offer more control.

Dollar-Cost Averaging: A highly recommended strategy is dollar-cost averaging. Instead of investing a large lump sum all at once, you invest a fixed amount of money at regular intervals (e.g., $100 every month). This strategy helps mitigate the risk of investing a large sum at a market peak and can smooth out your average purchase price over time. Most brokerages allow you to set up automated investments for mutual funds, making this strategy effortless.

Reinvesting Dividends

S&P 500 funds pay out dividends, which are portions of the profits from the underlying companies. You typically have the option to receive these dividends as cash or to have them automatically reinvested into buying more shares of the fund. For long-term growth, automatic dividend reinvestment is almost always the preferred option. This harnesses the power of compounding, allowing your dividends to generate their own returns over time, significantly boosting your total wealth accumulation.

Important Considerations for S&P 500 Investing

Investing in the S&P 500 is a powerful strategy, but like all investments, it comes with considerations and risks. A thoughtful approach is key to long-term success.

Understanding Risks and Volatility

While the S&P 500 has a strong long-term track record, it is not without risk.

- Market Risk: The value of your investment will fluctuate with the broader stock market. Economic downturns, geopolitical events, and company-specific issues can lead to temporary declines in value.

- No Guarantees: There’s no guarantee of future returns. While historical averages are encouraging, past performance does not dictate future results.

- Inflation Risk: If your investment returns don’t outpace inflation, your purchasing power could erode over time.

The key is to remember that these are often short-term fluctuations. For long-term investors, market downturns can even present opportunities to buy more shares at lower prices.

The Importance of a Long-Term Perspective

The S&P 500 is best viewed as a long-term investment. Its power lies in compounding returns over decades. Trying to time the market by buying low and selling high is notoriously difficult and often leads to worse outcomes than a simple buy-and-hold strategy. Aim to invest for at least 5-10 years, and preferably much longer, to ride out market cycles and fully benefit from its growth potential.

Diversification Beyond the S&P 500

While the S&P 500 offers excellent diversification within U.S. large-cap equities, a truly diversified portfolio extends beyond it.

- International Exposure: Consider adding international stock ETFs or mutual funds to gain exposure to global markets, which can sometimes outperform the U.S. market.

- Fixed Income (Bonds): Bonds can provide stability and income, especially as you approach retirement. They often move inversely to stocks, acting as a ballast during market downturns.

- Other Asset Classes: Depending on your risk tolerance and goals, you might explore real estate, commodities, or other alternative investments.

A well-balanced portfolio aligns with your risk tolerance, time horizon, and financial goals. The S&P 500 is an excellent core holding, but rarely should it be your only holding.

Managing Expense Ratios and Fees

Consistently prioritize low expense ratios. Over several decades, even a 0.50% difference in annual fees can cost you tens or hundreds of thousands of dollars in lost returns. Always review the expense ratio before investing in any fund. Similarly, be mindful of any trading commissions or account maintenance fees your brokerage might charge. Many reputable brokers offer commission-free ETF trading and no annual maintenance fees.

Tax Implications

Be aware of the tax implications of your investments.

- Dividends: Dividends from S&P 500 funds are taxable in a taxable brokerage account unless they are reinvested within a tax-advantaged account like an IRA.

- Capital Gains: When you sell your S&P 500 fund shares for a profit, you incur capital gains tax. This is either short-term (if held for less than a year) or long-term (if held for more than a year), with long-term capital gains generally taxed at lower rates.

- Tax-Advantaged Accounts: Utilizing IRAs, Roth IRAs, or 401(k)s can significantly reduce your tax burden, allowing your investments to grow more efficiently. Maximize contributions to these accounts first, especially if your employer offers a match.

Seeking Professional Advice

If you feel overwhelmed or unsure about your investment strategy, consider consulting a qualified financial advisor. A fee-only fiduciary advisor can help you assess your financial situation, set goals, create a personalized investment plan, and choose the right mix of investments, including how the S&P 500 fits into your broader strategy.

In conclusion, investing in the S&P 500 is a straightforward and highly effective strategy for long-term wealth building, offering broad diversification and exposure to the growth of America’s leading companies. By understanding the investment vehicles available, choosing the right brokerage and account, and adopting a disciplined, long-term approach, you can confidently participate in the market and work towards achieving your financial aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.