For many Americans, Social Security represents the bedrock of their retirement strategy. Yet, despite its importance, the actual mechanics behind the monthly check remain a mystery to the average worker. It is often viewed as a simple percentage of one’s final salary, but the reality is far more nuanced. The Social Security Administration (SSA) uses a complex, multi-step formula designed to provide a progressive safety net, ensuring that lower-income earners receive a higher percentage of their career earnings than high-income earners.

Navigating the financial landscape of retirement requires a deep dive into the “Average Indexed Monthly Earnings” (AIME) and the “Primary Insurance Amount” (PIA). Understanding these metrics is not merely an academic exercise; it is a vital component of personal finance that allows individuals to make informed decisions about when to stop working and how to supplement their income.

The Foundation: Eligibility and Average Indexed Monthly Earnings (AIME)

Before the SSA can calculate how much you are owed, they must determine if you are eligible and what your “career average” looks like. This process begins decades before you actually file for benefits.

The 40-Credit Requirement

To qualify for Social Security retirement benefits, you must first earn enough “credits.” In 2024, you receive one credit for every $1,730 in earned income, up to a maximum of four credits per year. To reach the threshold for retirement benefits, most workers need 40 credits, which typically equates to 10 years of work. While these credits determine eligibility, they do not determine the amount of the benefit; that is handled by your actual earnings history.

Wage Indexing: Adjusting for Inflation

The Social Security calculation does not simply look at the raw dollar amounts you earned in 1985 or 1995. Because the value of a dollar changes over time, the SSA uses “wage indexing” to bring your past earnings up to modern standards. They use the average wage index from the year you turn 60 and apply it to all previous years of work. This ensures that the $20,000 you earned in your youth is weighted fairly against the $80,000 you might earn later in your career, accounting for the general rise in the standard of living.

The 35-Year Rule

Perhaps the most critical component of the AIME calculation is the 35-year window. The SSA identifies your 35 highest-earning years (after indexing for inflation). These years are summed and then divided by 420 (the number of months in 35 years). The resulting figure is your Average Indexed Monthly Earnings.

Crucially, if you have fewer than 35 years of work history, the SSA does not shorten the denominator. They still divide by 420, filling in the missing years with zeros. From a financial planning perspective, this means that working even a few extra years to replace “zero-income” years can significantly boost your monthly benefit.

The Primary Insurance Amount (PIA) and Bend Points

Once the SSA has established your AIME, they apply a formula to determine your Primary Insurance Amount (PIA). This is the base amount you are entitled to receive if you retire at your Full Retirement Age (FRA). The formula is intentionally progressive, meaning it replaces a larger portion of income for lower-wage workers.

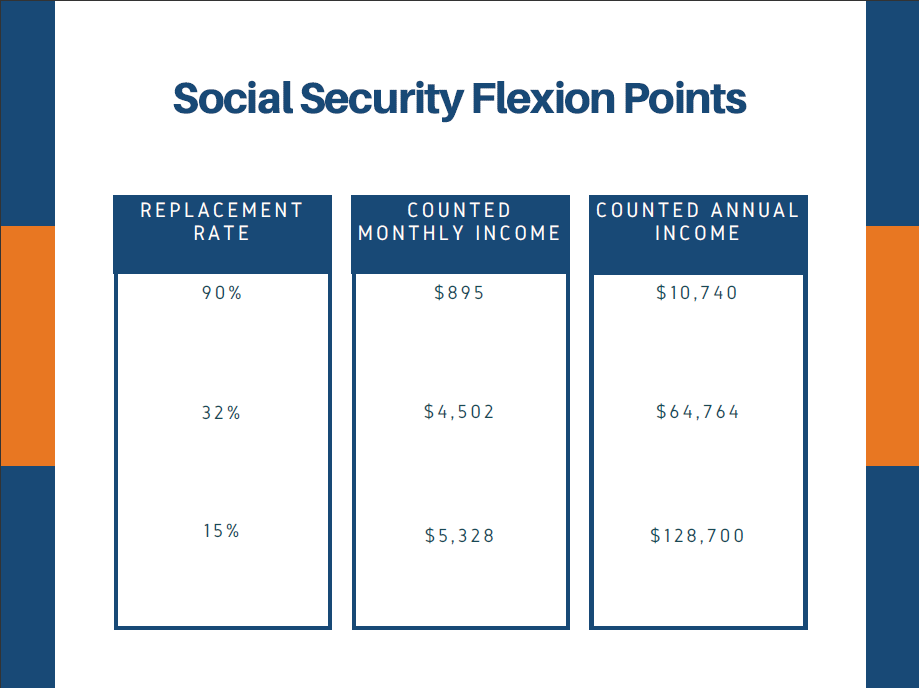

Breaking Down the Progressive Formula

The PIA formula is based on three distinct percentages, known as “bend points.” These bend points change annually based on national wage trends. For an individual reaching age 62 in 2024, the formula calculates the PIA by taking:

- 90% of the first $1,174 of AIME.

- 32% of AIME over $1,174 and through $7,078.

- 15% of AIME over $7,078.

The sum of these three amounts is rounded down to the next lower dime to arrive at the PIA. This structure explains why Social Security is not a “one-size-fits-all” percentage of your salary; it provides a robust floor for low earners while offering diminishing marginal returns for those at the top of the income bracket.

How Bend Points Protect Lower Earners

The “Money” logic behind these bend points is to mitigate poverty among the elderly. By capturing 90% of the first chunk of income, the system ensures that those who earned lower wages throughout their lives still have a functional baseline for survival. For high-income earners, the 15% bracket reflects the philosophy that those with higher lifetime earnings have a greater capacity for private savings and investment (such as 401(k)s or IRAs) to supplement their Social Security income.

The Impact of Timing: Retirement Age and Benefit Adjustments

The PIA calculated in the previous step is not necessarily what you will see in your bank account. The actual payout is heavily influenced by when you choose to begin receiving benefits. In the world of personal finance, this is perhaps the most significant “leverage point” an individual has over their Social Security.

Full Retirement Age (FRA)

Your Full Retirement Age is the age at which you are entitled to 100% of your PIA. For those born in 1960 or later, the FRA is 67. If you were born earlier, your FRA might be 66 and a certain number of months. Filing for benefits exactly at your FRA ensures you get the “pure” amount calculated by the AIME/PIA formula.

The Cost of Early Filing

You can choose to claim Social Security as early as age 62, but there is a steep financial penalty for doing so. If you claim early, your benefit is permanently reduced by a fraction of a percent for each month before your FRA. If your FRA is 67 and you claim at 62, your monthly check will be roughly 30% smaller than if you had waited. This reduction is designed to be “actuarially neutral,” meaning that, theoretically, you would receive the same total lifetime amount whether you take smaller checks for a longer period or larger checks for a shorter period. However, with increasing life expectancies, early filing is often a losing financial proposition for those in good health.

Delayed Retirement Credits (DRC)

Conversely, for every month you delay filing beyond your FRA (up until age 70), your benefit increases by 2/3 of 1%. This equates to an 8% annual increase. In the current financial climate, finding a guaranteed, inflation-adjusted 8% return on investment is nearly impossible. Therefore, for many retirees, delaying Social Security as long as possible is one of the most effective ways to maximize their “Money” profile in their later years.

External Factors Influencing Your Final Payout

Beyond your earnings and your filing age, several other financial variables can alter the final calculation of your Social Security benefits. Understanding these variables is essential for comprehensive business and personal finance planning.

The Maximum Taxable Earnings Limit

Social Security is funded by payroll taxes, but there is a cap on how much of your income is subject to these taxes. In 2024, this limit is $168,600. Any income earned above this amount is not taxed for Social Security, and consequently, it is not counted toward your AIME. This creates a “maximum possible benefit,” which limits how much the highest-earning individuals can receive from the system, regardless of whether they earn $200,000 or $2,000,000 a year.

Cost-of-Living Adjustments (COLA)

One of the most valuable features of Social Security is its protection against inflation. Every year, the SSA evaluates the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If prices have risen, the SSA applies a Cost-of-Living Adjustment (COLA) to benefits. This adjustment ensures that the purchasing power of your benefit does not erode as the cost of groceries, housing, and healthcare increases. For retirees on a fixed income, the COLA is a vital mechanism for long-term financial stability.

Windfall Elimination Provision (WEP) and Government Pension Offset (GPO)

The standard calculation can change significantly for individuals who have worked in “non-covered” employment—typically government jobs where they paid into a separate pension system instead of Social Security. The Windfall Elimination Provision (WEP) can reduce the PIA of a worker who also receives a pension from a non-covered job. Similarly, the Government Pension Offset (GPO) can reduce or eliminate spousal or survivor benefits for those with government pensions. Navigating these rules is a specialized area of financial planning that requires careful attention to avoid unexpected shortfalls.

Strategic Financial Implications

Understanding how Social Security is calculated is more than just understanding a government formula; it is about recognizing the asset value of your future benefits. For a retiree receiving $3,000 a month, that benefit is effectively equivalent to having an investment portfolio of roughly $900,000 (assuming a 4% withdrawal rate).

By analyzing the AIME and PIA, individuals can identify the “sweet spots” in their career. They can see the tangible value of working 35 full years and the massive ROI of delaying benefits from age 62 to 70. In the broader context of personal finance, Social Security should be treated as a low-risk, inflation-indexed annuity. When integrated correctly with other assets like real estate, stocks, and private pensions, a well-timed Social Security claim serves as the foundation for a secure and prosperous retirement. In an era of economic volatility, mastering these calculations provides a rare sense of certainty and control over one’s financial destiny.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.