Navigating the landscape of student loan repayment can often feel like deciphering a complex financial puzzle. A critical first step, and one that many borrowers surprisingly struggle with, is simply knowing who their student loan servicer is. This isn’t just a minor administrative detail; it’s the gateway to managing your debt, understanding your repayment options, and ultimately, securing your financial future. Whether you’re fresh out of college, returning to repayment after a period of forbearance, or simply consolidating your financial records, identifying your servicer is paramount. Without this crucial information, you’re essentially trying to pay a bill without knowing who to send the money to, leaving you vulnerable to missed payments, accruing interest, and potential damage to your credit score.

This guide will demystify the process, providing clear, actionable steps for locating your student loan servicer, whether your loans are federal or private. We’ll delve into why this information is so vital, the primary resources at your disposal, and what to do once you’ve successfully identified the entity responsible for managing your educational debt. Taking control of this seemingly small piece of information is a significant leap towards responsible financial management and stress-free loan repayment.

Why Knowing Your Servicer is Crucial for Financial Well-being

Understanding who services your student loans is more than just good organizational practice; it’s a fundamental aspect of effective personal finance. Your servicer is your primary point of contact for all things related to your loan – from payment processing to exploring hardship options. Without this link, you’re operating in the dark, risking financial missteps that could have long-term consequences.

Understanding Your Loan Obligations

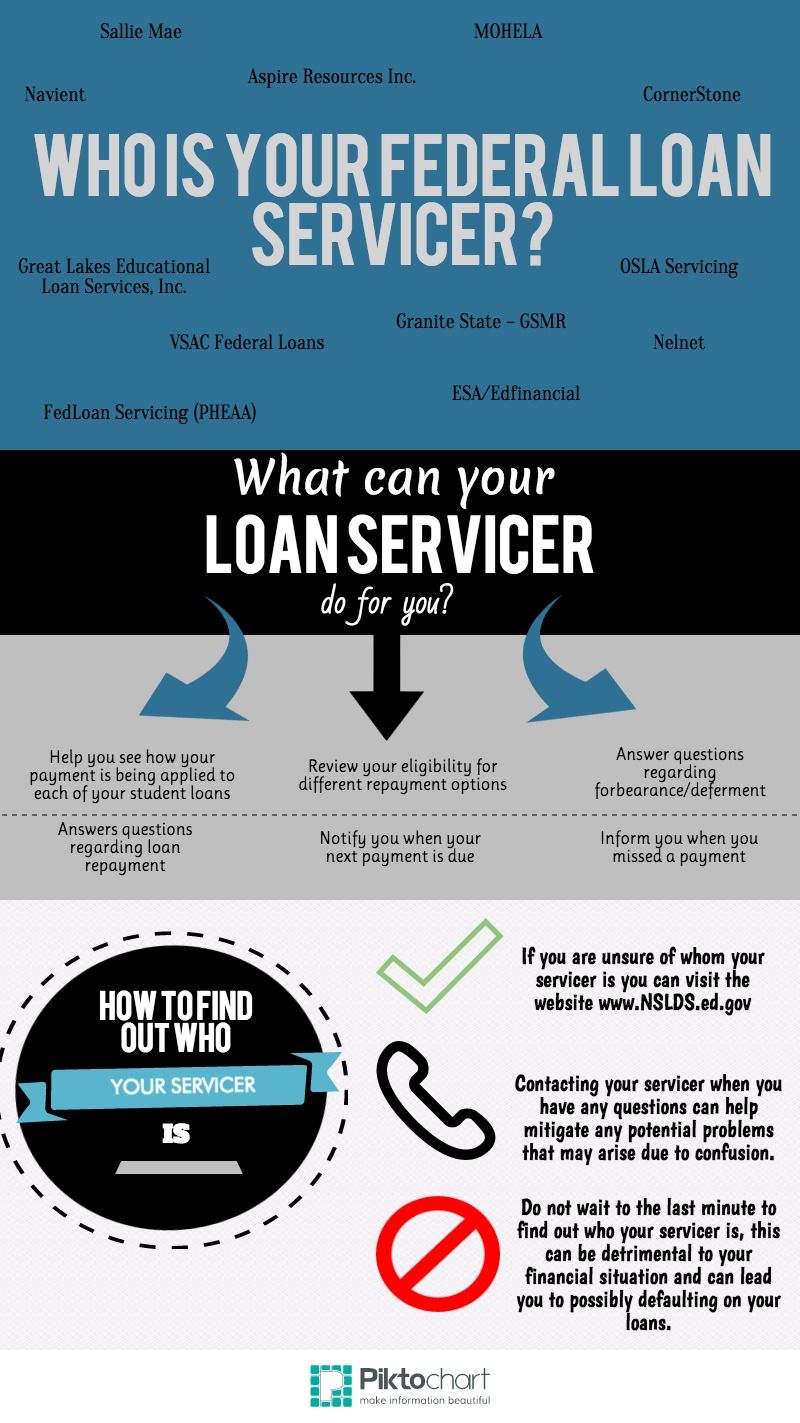

Your student loan servicer is the administrator of your loan. They send you bills, process your payments, and keep track of your loan balance and interest accrual. Knowing who they are means you can access detailed information about your specific loan terms, including interest rates, repayment schedules, and the total amount owed. This transparency is essential for budgeting effectively and planning your financial future. Without it, you might miss important updates or changes to your loan terms, which could lead to unexpected financial burdens. For instance, if your interest rate changes or a new fee is introduced, your servicer is the one who will communicate this to you. Being connected to them ensures you receive and understand these critical updates, allowing you to adjust your financial strategy accordingly and maintain control over your debt.

Accessing Repayment Options and Support

One of the most significant reasons to know your servicer is to unlock access to a variety of repayment options and support programs. Federal student loan servicers, in particular, can guide you through income-driven repayment (IDR) plans, deferment, or forbearance options if you’re facing financial hardship. They can explain the pros and cons of each, help you determine eligibility, and assist with the application process. Private loan servicers also offer some flexibility, though typically less than federal programs. Engaging with your servicer can prevent default and offer a lifeline during difficult times. If you lose your job or experience a medical emergency, your servicer can help you pause payments or adjust your monthly amount, preventing you from falling behind and damaging your credit. This proactive engagement is a cornerstone of responsible debt management, ensuring that you utilize all available tools to keep your finances on track.

Avoiding Default and Financial Pitfalls

Falling into default on student loans carries severe repercussions, including damage to your credit score, wage garnishment, and even the withholding of tax refunds. Often, default occurs not because a borrower is unwilling to pay, but because they are unable to connect with the right entity to discuss their situation or understand their options. Your servicer is your partner in avoiding default. By maintaining open communication and being aware of who they are, you can proactively address payment difficulties, explore solutions before problems escalate, and protect your financial health. They can provide counseling, explain the consequences of non-payment, and help you navigate pathways to rehabilitation or consolidation if you’re already in distress. Without knowing your servicer, you lose this crucial line of communication, making it significantly harder to resolve payment issues and increasing your risk of default.

The Primary Hubs for Federal Student Loan Information

For the vast majority of borrowers with federal student loans, the process of finding your servicer has been streamlined thanks to centralized government resources. The key to unlocking this information lies in knowing where to look and having the right credentials.

StudentAid.gov: Your Central Federal Loan Portal

The definitive source for all your federal student loan information is StudentAid.gov, managed by the U.S. Department of Education. This website is a comprehensive portal where you can view your entire federal student aid history, including grants, scholarships, and all your federal student loans. More importantly, it clearly lists all the loan servicers assigned to your federal loans, along with their contact information and the specific loans they manage.

To access your information on StudentAid.gov, you will need to log in using your Federal Student Aid (FSA) ID. This is the same ID you used to complete the Free Application for Federal Student Aid (FAFSA®) form. If you’ve forgotten your FSA ID or never created one, the website provides easy steps to retrieve it or set one up. Once logged in, navigate to your “My Aid” section. Here, you’ll find a detailed summary of your federal loans, including the original loan amounts, current balances, and, critically, the names and contact details of your current loan servicers. This platform is invaluable for tracking your federal debt, monitoring payment progress, and understanding the status of your loans, offering a complete picture of your obligations in one accessible location.

Your Federal Student Aid (FSA) ID

Your FSA ID is more than just a username and password; it’s your secure digital signature for accessing and managing your federal student aid information. It verifies your identity when you access your records on StudentAid.gov. Without a valid FSA ID, you won’t be able to log in and retrieve your loan servicer details. If you’ve never created an FSA ID, or if you’ve forgotten yours, the StudentAid.gov website offers clear instructions. It typically requires your Social Security number, date of birth, and an email address or mobile phone number. It’s essential to keep your FSA ID secure, as it grants access to sensitive financial information. If you’re struggling to log in, ensure you’re using the correct username and password, and utilize the recovery options provided on the site. Remember, the FSA ID is not tied to a specific loan servicer but to the Department of Education’s overarching system, making it your universal key to federal student loan data.

How to Navigate StudentAid.gov for Servicer Details

Once you’ve successfully logged into StudentAid.gov with your FSA ID, finding your servicer is straightforward:

- Dashboard Overview: Upon logging in, you’ll typically land on a dashboard that summarizes your federal student aid.

- “My Aid” Section: Look for a section or tab labeled “My Aid” or “View My Aid.” Click on this to access detailed information about your loans and grants.

- Loan Details: Within the “My Aid” section, you’ll see a breakdown of your federal loans. Each loan or group of loans will usually list the name of the servicer assigned to it, along with their contact information (website, phone number).

- Historical Data: StudentAid.gov also allows you to see the history of your loans, including any transfers between servicers. This can be particularly useful if your loan servicer has changed over time, which is a common occurrence.

By following these steps, you can quickly and accurately identify all your federal student loan servicers, allowing you to take the next step in managing your debt responsibly.

Strategies for Locating Private Student Loan Servicers

Unlike federal loans, which are consolidated under a single government database, private student loans are issued by various banks, credit unions, and private lenders. This decentralized nature can make finding your servicer slightly more challenging, but several effective strategies can help you pinpoint the right entity.

Reviewing Your Credit Report

Your credit report is an invaluable resource for tracking all your active credit accounts, including private student loans. Each lender or servicer that reports to the major credit bureaus (Experian, EquiFax, and TransUnion) will appear on your report.

- Access Your Report: You are entitled to a free copy of your credit report from each of the three major credit bureaus once every 12 months through AnnualCreditReport.com. This is the only official, government-authorized website for free credit reports.

- Identify Creditors: Once you have your report, meticulously review the “accounts” or “trade lines” section. Look for entries labeled as “student loan,” “educational loan,” or similar descriptions.

- Servicer Information: Next to each private student loan entry, you should find the name of the lender or the current servicer. The report will also typically include the account number and sometimes contact information. This is often the quickest and most comprehensive way to identify private loan servicers you may have forgotten about or whose names have changed.

Checking Old Loan Documents

If you’ve maintained good records, your original loan documents are a treasure trove of information. The promissory note you signed when you took out the loan will clearly state the original lender and often the initial servicer. Subsequent disclosure statements, annual loan summaries, or any correspondence related to your loans could also contain vital clues. Look for:

- Promissory Notes: The contract you signed outlines the terms and conditions and identifies the original lender.

- Billing Statements: Old paper or electronic statements will show who was sending you bills and processing payments.

- Welcome Packets: When your loan was first disbursed, you likely received a packet with all the details, including servicer information.

Even if the servicer has changed hands since then, knowing the original lender can provide a starting point for inquiries.

Contacting Your Original Lender

If you remember which bank or financial institution originally provided your private student loan, contacting them directly can be an effective strategy. Even if they no longer service your loan, they will have a record of your account and can typically tell you who purchased or is now servicing the loan. Have your personal information (name, date of birth, Social Security number) ready, as well as any old account numbers you might have. Most banks have dedicated student loan departments or customer service lines that can assist with these inquiries. This is particularly useful if your credit report doesn’t immediately yield the servicer’s name or if you suspect a transfer has occurred that isn’t yet reflected on your report.

Bank Statements and Payment Records

Another practical approach is to review your past bank statements or credit card statements. If you’ve ever made a payment on your private student loan, the name of the servicer or lender will likely appear on the transaction details. Search your online banking portal or physical statements for:

- Automated Payments: If you set up auto-pay, the recipient’s name will be listed.

- Manual Payments: Check for transfers, checks written, or debit card payments made to a student loan company.

- Cancelled Checks: The payee information on a cancelled check will clearly state who received your payment.

This method helps confirm who you were most recently paying, providing a strong lead on your current servicer.

What to Do Once You’ve Identified Your Servicer

Once you’ve successfully identified your student loan servicer(s), whether federal or private, the next crucial step is to actively engage with them. This proactive approach is fundamental to effective debt management and ensuring a smooth repayment journey.

Create an Online Account

The very first action you should take is to visit your servicer’s website and create an online account. This account will be your primary portal for managing your loans. Through this online platform, you can:

- Monitor your balance and interest accrual: See exactly how much you owe and how interest is adding up.

- Make payments: Set up one-time or recurring payments, which often qualify you for a small interest rate reduction on federal loans.

- View payment history: Track all your past payments and confirm they were applied correctly.

- Access statements and tax documents: Download monthly statements and year-end tax forms (like Form 1098-E for student loan interest deduction).

- Update contact information: Ensure your servicer can always reach you with important updates.

Having an active online account empowers you to stay on top of your loans and avoid missing critical information.

Understand Your Loan Details Thoroughly

With access to your servicer’s portal, take the time to delve into the specifics of each of your loans. Key details to understand include:

- Interest rates: Note whether your rates are fixed or variable.

- Repayment schedule: Understand your minimum monthly payment and the remaining term of your loan.

- Total outstanding balance: Get a clear picture of your total debt.

- Loan types: Differentiate between subsidized, unsubsidized, PLUS, and private loans, as each has different features and benefits.

A comprehensive understanding of these details will enable you to make informed decisions about your repayment strategy and accurately forecast your financial obligations.

Explore Repayment Plans and Options

This is particularly relevant for federal student loan borrowers. Your servicer is the expert on the various repayment plans available and can help you determine the best fit for your financial situation. For federal loans, options include:

- Standard Repayment Plan: A fixed monthly payment over 10 years.

- Graduated Repayment Plan: Payments start low and gradually increase over time.

- Extended Repayment Plan: Lower payments over a longer period (up to 25 years).

- Income-Driven Repayment (IDR) Plans: Payments are capped at a percentage of your discretionary income and adjust based on your income and family size. These include PAYE, REPAYE, IBR, and ICR.

- Deferment and Forbearance: Temporary options to postpone or reduce payments during periods of financial hardship.

Even private loan servicers may offer some limited options, such as temporary payment reductions or forbearance, so it’s always worth inquiring if you’re struggling. Understanding and utilizing these options can significantly alleviate financial stress.

Proactive Communication is Key

Establish a habit of proactive communication with your servicer. Don’t wait until you’re in default or facing an immediate crisis to reach out. If your financial situation changes (e.g., job loss, reduction in income, marriage), contact your servicer immediately. They can often help you adjust your payment plan or explore temporary relief options before you miss a payment. Similarly, if you have questions about your statement, interest charges, or anything else related to your loans, pick up the phone or send a secure message through your online account. Open and honest communication is your best defense against unexpected issues and ensures you maintain a good standing with your loans.

Common Challenges and Troubleshooting

Even with the best intentions, navigating student loan repayment can present challenges. Loans can be sold, circumstances can change, and the threat of scams always looms. Being prepared for these eventualities can save you significant stress and financial peril.

Loans Sold or Transferred

It’s common for student loans, both federal and private, to be sold or transferred from one servicer to another. This doesn’t change the terms of your loan, but it does change who you send your payments to and who you communicate with.

- Notification: When a loan is transferred, both your old and new servicers are legally required to notify you. These notifications usually come via mail or email, so it’s crucial to keep your contact information updated with your servicer and to check your mail regularly.

- Seamless Transition: During a transfer, payments are typically routed correctly, but there can be a brief period of adjustment. Always confirm with the new servicer that your payment history has been accurately transferred.

- Where to Check: If you suspect a transfer but haven’t received notification, check StudentAid.gov for federal loans (it reflects the most current servicer) or your credit report for private loans.

Staying vigilant for these notifications and verifying information can prevent missed payments and confusion.

Deceased Borrower or Defaulted Loans

Specific circumstances require different approaches to finding your servicer and managing the loans.

- Deceased Borrower: Federal student loans are typically discharged upon the borrower’s death, meaning the remaining balance is forgiven. Private loan policies vary; some may be discharged, while others may require the estate or a co-signer to repay. For federal loans, a family member should contact the servicer with a death certificate. For private loans, contact the lender directly to understand their policy.

- Defaulted Loans: If your loans are in default, the servicer may change, or the debt may be assigned to a collection agency or guaranty agency. For federal loans, you might need to contact the Department of Education’s Default Resolution Group. For private loans, the collection agency or a specific department within the original lender would be the point of contact. The goal is to rehabilitate the loan or explore settlement options to mitigate the impact on your credit.

These situations are sensitive and complex, making prompt identification of the correct entity even more critical.

Avoiding Scams

Unfortunately, the student loan landscape is a fertile ground for scammers. Be extremely wary of companies that:

- Charge upfront fees: Legitimate services, like applying for IDR plans, are free through your servicer or StudentAid.gov.

- Promise immediate loan forgiveness: While forgiveness programs exist, they have strict eligibility requirements and timelines. Scammers often make unrealistic promises.

- Ask for your FSA ID: Never share your FSA ID with anyone. This is your personal identifier for federal student aid.

- Pressure you for quick decisions: Legitimate organizations will give you time to consider your options.

Always go directly to your servicer’s official website (ensure the URL is correct) or StudentAid.gov for federal loan assistance. If something sounds too good to be true, it almost certainly is. Protect your personal and financial information diligently.

In conclusion, understanding “how to find my student loan servicer” is a fundamental step in navigating your financial obligations. By leveraging federal resources like StudentAid.gov and meticulously reviewing personal financial documents and credit reports for private loans, you can efficiently identify the entities managing your debt. Once connected, proactive engagement with your servicer, understanding your loan details, exploring repayment options, and remaining vigilant against scams are all essential practices for responsible student loan management. Taking these steps empowers you to take control of your financial future, transforming a potentially daunting challenge into a manageable journey towards financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.