In an increasingly complex financial world, the ability to effectively manage one’s money is not merely a desirable skill but a fundamental pillar of personal well-being and long-term security. From daily expenses to aspirational goals like homeownership, education, or a comfortable retirement, every financial decision we make shapes our future. This guide is designed to provide a comprehensive framework for improving your money management skills, offering practical strategies, insightful perspectives, and actionable steps to build a more robust financial life. It’s about empowering you to take control, reduce stress, and cultivate a path towards enduring financial freedom.

The Foundation: Understanding Your Financial Landscape

Before you can build a sturdy financial future, you must first understand the ground you’re standing on. This involves a clear, honest assessment of your current financial situation, the establishment of meaningful goals, and the implementation of a consistent tracking system.

Assessing Your Current Financial Health

The first step in any improvement journey is to know your starting point. Begin by calculating your net worth, which is simply the total value of your assets (what you own, e.g., savings, investments, property) minus your liabilities (what you owe, e.g., loans, credit card debt). This single figure provides a snapshot of your financial standing. Equally important is a thorough review of your income and expenses. Track every dollar coming in and going out for at least a month, ideally two or three. This detailed analysis will reveal where your money truly goes, highlighting potential areas of overspending or inefficiencies. Finally, understand your credit score. This three-digit number significantly impacts your ability to borrow money for major purchases like a house or car, and even influences insurance premiums. Regularly check your credit report for errors and take steps to improve your score by paying bills on time and keeping credit utilization low.

Setting Clear Financial Goals

Managing money effectively is significantly easier when you have a destination in mind. Goals provide motivation and direction. Categorize your goals into short-term (1-2 years, e.g., building an emergency fund, paying off a small debt), mid-term (3-5 years, e.g., saving for a down payment, a new car, or education), and long-term (5+ years, e.g., retirement, child’s college fund, early financial independence). For each goal, employ the SMART framework: ensure it is Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of “save money,” aim for “save $10,000 for a down payment on a house within three years.” Clearly defined goals allow you to prioritize your spending and saving efforts.

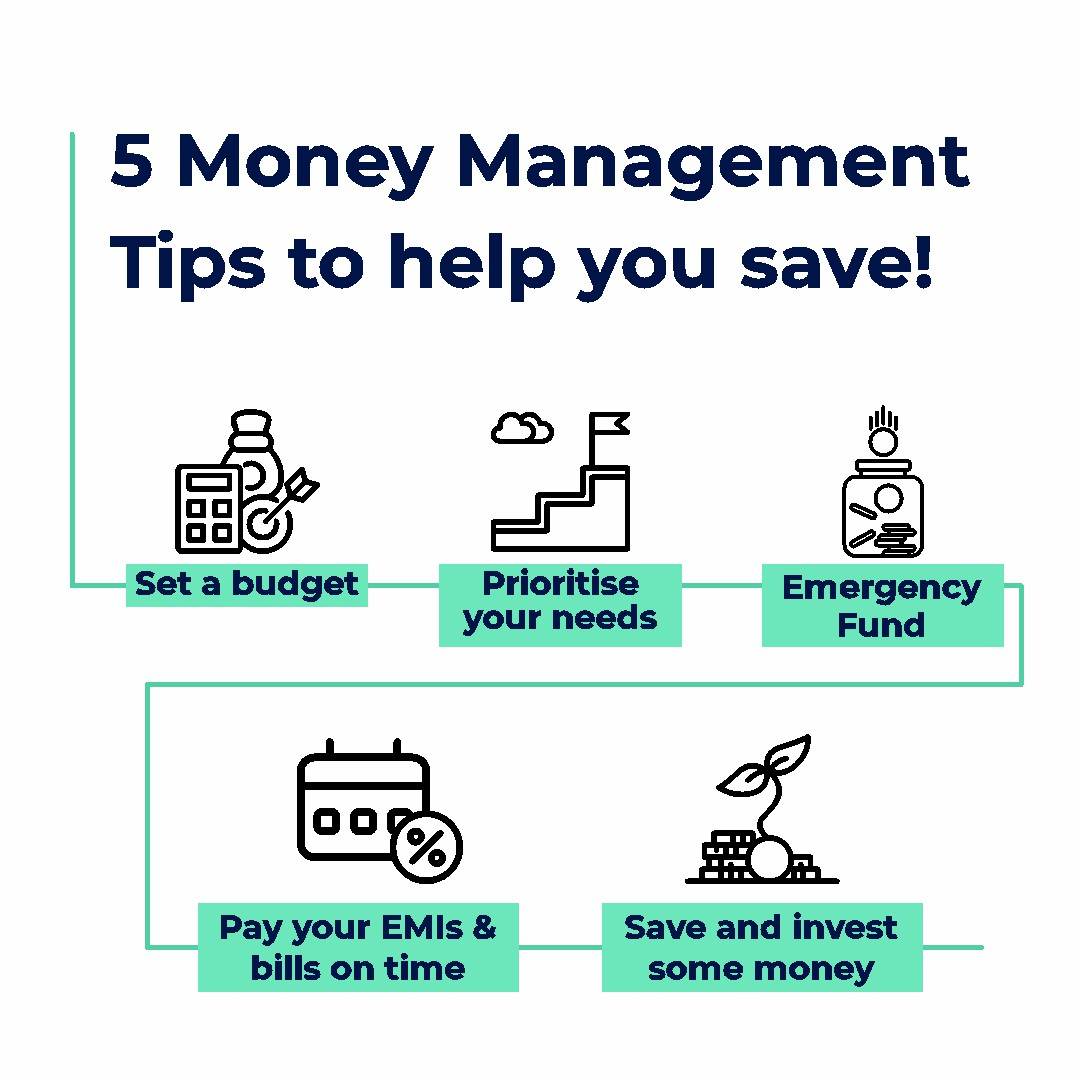

The Power of Budgeting and Tracking

Budgeting is not about restriction; it’s about intentional spending and allocation. It’s your financial roadmap. There are various budgeting methods, such as the popular 50/30/20 rule (50% needs, 30% wants, 20% savings/debt repayment), zero-based budgeting (every dollar is assigned a job), or the envelope system (physical cash for different categories). Choose the method that best suits your lifestyle and stick to it. Beyond creating a budget, consistent tracking is crucial. This means monitoring your spending against your budgeted categories. Whether you use a spreadsheet, a dedicated app, or a simple notebook, regularly reviewing your expenditures allows you to identify discrepancies, adjust your budget as needed, and ensure you’re staying on track towards your goals. Without tracking, a budget is merely a theoretical exercise.

Strategic Pillars for Financial Growth

Once you have a firm understanding of your financial present, the next step is to implement strategies that actively grow and protect your wealth. This involves tackling debt, building reserves, and making your money work harder for you.

Mastering Debt Management

Debt can be a powerful tool for major life purchases, but it can also be a significant impediment to financial progress if mismanaged, especially high-interest debt like credit card balances. Differentiate between “good” debt (e.g., a mortgage or student loan that can lead to increased assets or earning potential) and “bad” debt (e.g., high-interest consumer debt for depreciating assets). Prioritize paying off bad debt aggressively. Popular strategies include the debt snowball method (paying off smallest debts first for motivational wins) or the debt avalanche method (paying off highest-interest debts first to save money). Consider debt consolidation or balance transfers for high-interest credit card debt, but only if you have a solid plan to avoid accumulating new debt. The ultimate goal is to minimize interest payments and free up cash flow for saving and investing.

Building a Robust Emergency Fund

An emergency fund is your financial safety net, designed to cover unexpected expenses without derailing your financial progress or forcing you into high-interest debt. This fund should be easily accessible but separate from your everyday spending accounts. Aim to save at least three to six months’ worth of essential living expenses (rent/mortgage, utilities, food, transportation, insurance). For greater peace of mind or if you have an irregular income, extending this to nine or twelve months is advisable. Store your emergency fund in a high-yield savings account where it can earn a modest return while remaining liquid. Treat building this fund as a non-negotiable financial priority, even before aggressive investing.

Strategic Saving and Investing for the Future

Saving is putting money aside for a specific purpose in the short to mid-term; investing is putting money to work with the expectation of generating returns over the long term, typically through compound interest. Automate your savings by setting up regular transfers from your checking account to your savings or investment accounts immediately after payday. For investing, start early and invest consistently, even small amounts. Understand basic investment concepts like diversification (spreading investments across different asset classes to reduce risk), risk tolerance (your comfort level with potential losses), and compound interest (earning returns on your initial investment and on accumulated interest). Explore common investment vehicles such as stocks, bonds, mutual funds, exchange-traded funds (ETFs), and employer-sponsored retirement plans like 401(k)s (especially if there’s an employer match – free money!) and individual retirement accounts (IRAs). Don’t let fear or lack of knowledge deter you; start with low-cost index funds or robo-advisors if you’re a beginner.

Leveraging Tools and Habits for Sustained Success

Effective money management is not a one-time fix but an ongoing practice that benefits from modern tools and consistent positive habits.

Utilizing Financial Technology

The digital age offers a plethora of financial tools that can simplify and enhance your money management efforts. Budgeting apps like Mint, YNAB (You Need A Budget), or Personal Capital can automatically categorize transactions, track spending, and even provide net worth updates. Robo-advisors such as Betterment or Wealthfront can help you invest based on your goals and risk tolerance with minimal effort. Online banking platforms provide convenient features like automated bill pay, recurring transfers, and spending alerts. Explore these tools to find what best fits your needs, but remember that technology is a facilitator, not a substitute for understanding your finances. It empowers you to implement your strategies more efficiently.

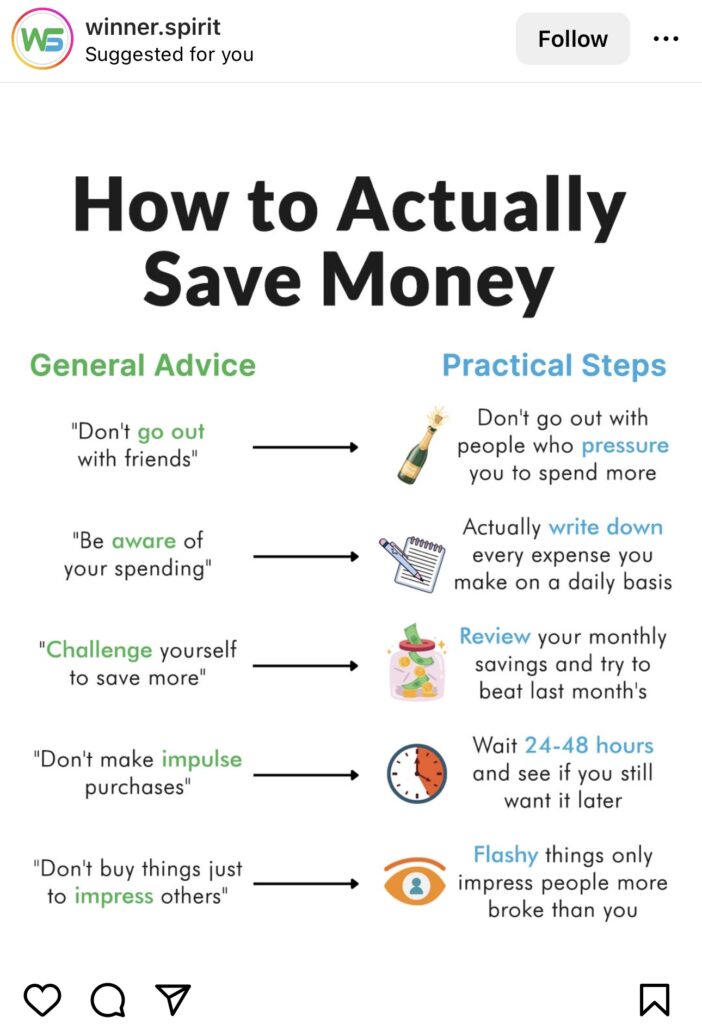

Cultivating Mindful Spending Habits

Beyond the numbers, developing a healthier relationship with money involves mindful spending. This means consciously distinguishing between needs (housing, food, utilities, transportation, essential healthcare) and wants (dining out, entertainment, designer clothes, subscriptions you don’t use). Practice delayed gratification by waiting before making non-essential purchases, giving yourself time to consider if an item truly adds value. Avoid impulse buying, especially online, by creating cooling-off periods. Understanding the psychological triggers behind your spending can help you make more intentional choices. The goal is to find joy in experiences and savings, rather than solely in acquiring material possessions, thereby aligning your spending with your true values and financial goals.

Regular Financial Reviews and Adjustments

Personal finance is dynamic, not static. Life circumstances change, incomes fluctuate, and economic conditions evolve. Therefore, it’s essential to conduct regular financial reviews – ideally monthly or quarterly. During these reviews, revisit your budget, assess your progress towards your goals, and make any necessary adjustments. Did your income change? Did you incur a new recurring expense? Are your goals still relevant? This iterative process ensures your financial plan remains aligned with your current life situation and aspirations. Flexibility and adaptability are key; treat your budget and financial plan as living documents that evolve with you.

Protecting Your Wealth and Planning for Tomorrow

Effective money management extends beyond immediate financial control to safeguarding your assets and planning for the long-term, including inevitable life events.

Understanding Insurance Needs

Insurance serves as a critical safety net, protecting your accumulated wealth and future earning potential from unforeseen catastrophes. Assess your needs for various types of insurance: health insurance (to cover medical costs), life insurance (to provide for dependents upon your passing), disability insurance (to replace income if you become unable to work), and property insurance (home, auto) to protect your assets. Do not underinsure; a single major event without adequate coverage can wipe out years of financial progress. Regularly review your policies to ensure they align with your current life stage and asset base.

Creating a Will and Estate Plan

Estate planning is not just for the wealthy; it’s a fundamental aspect of financial responsibility for everyone. A basic estate plan typically includes a will, which dictates how your assets will be distributed after your death, and a power of attorney, which designates someone to make financial and medical decisions on your behalf if you become incapacitated. A living will (advance directive) expresses your wishes regarding medical treatment. Without these documents, decisions about your assets and care could fall to the courts, potentially causing significant stress, delays, and expenses for your loved ones. Planning ensures your wishes are honored and your family is protected.

Continuous Learning and Adaptation

The world of personal finance is constantly evolving. New financial products emerge, tax laws change, and economic landscapes shift. To remain an effective money manager, commit to continuous learning. Read reputable financial books, follow trusted financial news sources and blogs, and stay informed about economic trends. Don’t be afraid to seek professional advice from a fee-only financial planner if you encounter complex situations or need expert guidance on specific investments or retirement planning. Viewing money management as a lifelong learning journey will empower you to adapt to new challenges and seize new opportunities.

Becoming better at managing money is a journey, not a destination. It requires discipline, patience, and a commitment to continuous learning. By building a strong financial foundation, implementing strategic growth pillars, leveraging modern tools and mindful habits, and proactively planning for the future, you can transform your relationship with money. The reward is not just a healthier bank account, but also greater peace of mind, reduced stress, and the freedom to pursue the life you envision. Start today, one intentional step at a time, and watch your financial future flourish.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.