For millions of Americans, Social Security represents a cornerstone of financial security in retirement, during disability, or for their surviving family members. Understanding how Social Security credits are calculated is not merely an administrative detail; it’s a fundamental step in planning your financial future and ensuring you qualify for the benefits you’ve earned through your years of hard work. This intricate system, while designed to be straightforward, often raises questions regarding eligibility and the mechanics of earning these vital credits.

This article delves deep into the heart of Social Security credit calculation, demystifying the process and providing actionable insights. We’ll explore what these credits are, how they are earned based on your income, the maximum you can accumulate annually, and critically, how these credits translate into eligibility for different types of Social Security benefits. By the end, you’ll have a clear, professional, and insightful understanding of this crucial aspect of personal finance, empowering you to better plan for tomorrow.

Understanding the Foundation: What Are Social Security Credits?

At its core, Social Security operates on a system of earned credits. These credits are the fundamental units used by the Social Security Administration (SSA) to determine your eligibility for various benefits. Think of them as points you accumulate throughout your working life, and these points dictate whether you qualify for retirement income, disability protection, or even survivor benefits for your family.

The Building Blocks of Your Retirement Security

Every time you work and pay Social Security taxes (FICA taxes), you are earning credits towards future benefits. These taxes are automatically deducted from your paycheck by your employer or paid directly if you are self-employed. The more you work and earn up to a certain threshold, the more credits you accumulate. It’s a direct correlation: your contributions through taxes translate into credits that form the foundation of your entitlement to future Social Security payments.

These credits are crucial because Social Security benefits are not universal. They are an earned entitlement, meaning you must have worked a sufficient amount of time and contributed enough through payroll taxes to qualify. Without the necessary credits, even if you’ve paid some taxes, you may not be eligible for full (or any) benefits. This system ensures that those who have contributed to the trust funds are the ones who benefit from them.

Why Credits Matter: Eligibility for Essential Benefits

The importance of Social Security credits cannot be overstated. They are the gateway to virtually all Social Security programs. Whether you’re planning for your golden years, considering the safety net of disability insurance, or ensuring your loved ones are protected financially after your passing, credits are the key.

For instance, to receive retirement benefits, you generally need to accumulate a certain number of credits. Similarly, to qualify for Social Security Disability Insurance (SSDI), you must meet specific work credit requirements that depend on your age at the time you become disabled. Even survivor benefits, which provide financial support to your spouse, children, or parents after your death, are contingent upon your earning a minimum number of credits during your working life. Understanding these thresholds is vital for proactive financial planning and risk management.

Earning Your Credits: The Calculation Mechanics

The process of earning Social Security credits is tied directly to your annual earned income. The Social Security Administration sets a specific dollar amount of earnings that counts towards one credit each year. This amount is adjusted annually to account for changes in national average wages, ensuring the system remains relevant with economic shifts.

The Annual Income Threshold for a Credit

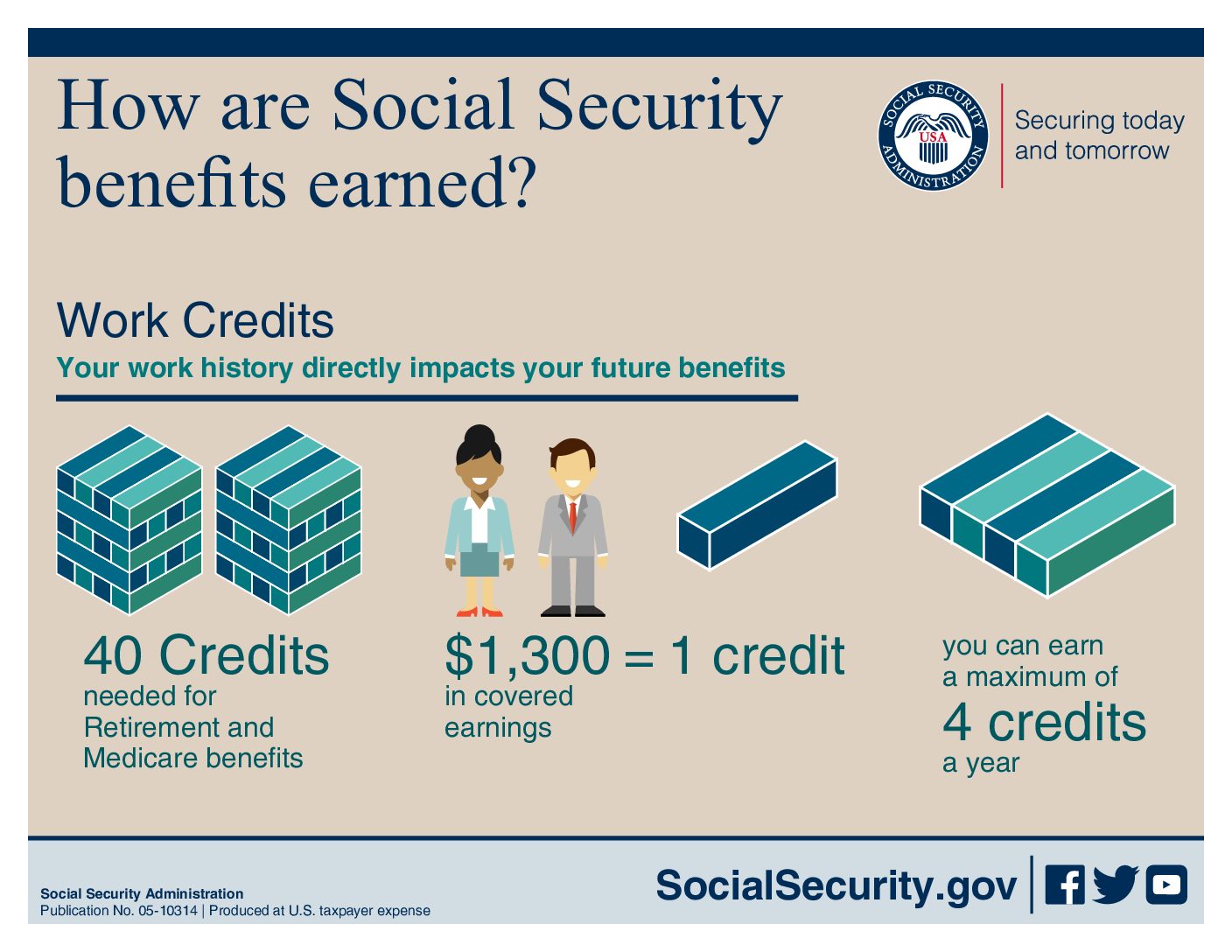

In any given year, you earn one Social Security credit for a specific amount of earnings. For example, in 2024, you earn one Social Security credit for every $1,730 in earnings. This means if you earn at least $1,730, you’ve earned one credit. If you earn twice that, you’ve earned two, and so on, up to the annual maximum.

It’s important to note that these earnings refer to gross income from wages or net earnings from self-employment. They must be earnings on which Social Security taxes were paid. Non-taxable income, such as certain investment income, generally does not count towards earning Social Security credits. The SSA carefully tracks these earnings through your employer’s reports and your self-employment tax filings.

The Maximum Credits You Can Earn Per Year

While you earn a credit for a specific amount of income, there’s an upper limit to how many credits you can accumulate in a single year. You can earn a maximum of four Social Security credits per year, regardless of how much income you make above the annual threshold for four credits.

Using the 2024 example: if one credit requires $1,730 in earnings, then to earn the maximum four credits, you would need to earn $1,730 x 4 = $6,920 during the year. Even if you earn $70,000, $170,000, or more in that year, you will still only receive the maximum of four credits. This system ensures that everyone, regardless of their income level beyond a certain point, accumulates credits at the same annual rate. This maximum annual cap is a key feature of the Social Security credit system, emphasizing work longevity over sheer income volume for qualification purposes.

The Role of Earned Income: Wages vs. Self-Employment

The method of earning credits is consistent whether you work for an employer or are self-employed, but the tax payment mechanism differs. If you work for an employer, your Social Security (FICA) taxes are automatically deducted from your paycheck. Your employer withholds your share and pays their matching share, remitting both to the IRS. These reported earnings are then credited to your Social Security record.

For self-employed individuals, the responsibility for paying Social Security and Medicare taxes falls on them directly through the Self-Employment Contributions Act (SECA) tax. When you file your annual tax return, your net earnings from self-employment are used to calculate your SECA tax. As long as your net earnings meet the annual threshold, you will earn Social Security credits in the same manner as an employee, up to the maximum of four per year. It’s crucial for self-employed individuals to accurately report their income and pay their taxes to ensure their Social Security earnings record is complete and accurate.

The Credit Requirement for Different Social Security Benefits

The total number of credits you need to qualify for benefits varies depending on the type of benefit and your age or circumstances. The most common requirement is 40 credits for retirement benefits, but other situations demand different thresholds.

Retirement Benefits: Your Path to Financial Independence

To qualify for Social Security retirement benefits, you generally need to have earned 40 credits. Since you can earn a maximum of four credits per year, this typically translates to working for at least 10 years. These 40 credits do not need to be earned consecutively; they can be accumulated over your entire working life. Once you’ve earned these 40 credits, you are “fully insured” and eligible to receive retirement benefits once you reach the minimum age (currently 62) and apply. The amount of your benefit, however, depends on your average indexed monthly earnings over your 35 highest-earning years, not just the number of credits.

Disability Benefits: A Safety Net When You Need It Most

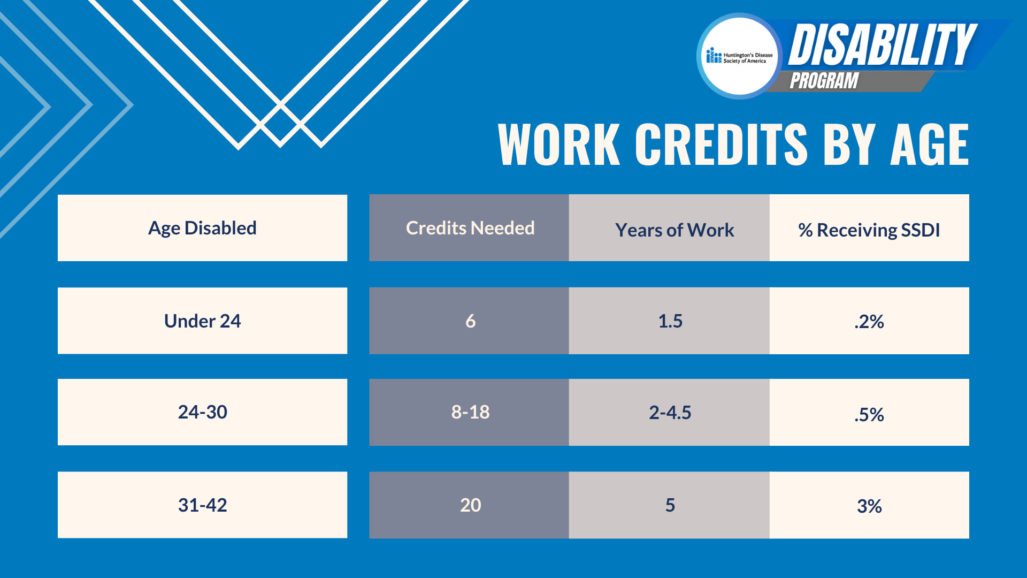

Qualifying for Social Security Disability Insurance (SSDI) is more nuanced. The number of credits you need depends on your age when you become disabled.

- Before age 24: You generally need 6 credits earned in the 3-year period ending when your disability starts.

- Ages 24 to 31: You generally need credits for half the time between age 21 and the time you become disabled (e.g., if you are 27, you need 3 years of credits out of the last 6 years, or 12 credits).

- Age 31 or older: You generally need at least 20 credits in the 10-year period immediately before you became disabled, plus the total 40 credits needed to be fully insured for retirement.

These requirements ensure that the disability insurance program primarily covers individuals who have a recent work history and have contributed consistently to the system.

Survivor Benefits: Protecting Your Loved Ones

Survivor benefits provide crucial financial support to eligible family members (spouse, children, dependent parents) after your death. The number of credits needed for your family to receive survivor benefits also depends on your age at the time of death.

- Fully Insured: If you are fully insured (typically 40 credits), your family is eligible for all types of survivor benefits.

- Currently Insured: Even if you aren’t fully insured, your children and their mother or father may be eligible for benefits if you have earned at least 6 credits in the 3-year period ending with your death. This “currently insured” status acts as a short-term safety net.

Understanding these different credit requirements allows individuals to assess their financial preparedness and make informed decisions about life insurance and other forms of financial protection.

Tracking Your Progress: How to Monitor Your Social Security Credits

Proactively monitoring your Social Security credits and earnings record is a critical step in personal financial management. Errors can occur, and an accurate record ensures you receive all the benefits you’re entitled to.

Accessing Your Social Security Statement Online

The easiest and most efficient way to track your credits and earnings is by creating a “my Social Security” account on the SSA’s official website (www.ssa.gov). Through this secure portal, you can:

- View your complete earnings history, year by year.

- See how many credits you’ve accumulated.

- Obtain estimates of your future retirement, disability, and survivor benefits.

- Review your current credit count and determine if you meet the fully insured status.

The SSA encourages all working individuals to set up an account and regularly review their statement, especially as they approach retirement or if they have had multiple employers or periods of self-employment.

Reviewing Your Earnings Record for Accuracy

When you access your Social Security Statement, pay close attention to your earnings record. Each year of your work history, along with the corresponding earnings reported to the SSA, will be listed. It’s important to cross-reference these amounts with your W-2 forms or self-employment tax returns. Look for:

- Missing years of earnings: If you worked a year but it’s not reflected, or the earnings are significantly lower than expected.

- Incorrect earnings amounts: Discrepancies between what you earned and what the SSA has recorded.

- Years with no earnings when you know you worked: This could indicate an issue with your employer reporting or your self-employment tax filings.

Promptly identifying and addressing these issues is crucial, as the SSA has limits on how far back they can correct earnings records.

Correcting Discrepancies in Your Work History

If you discover an error or discrepancy in your earnings record, it’s vital to contact the Social Security Administration as soon as possible. You’ll typically need to provide evidence to support your claim, such as W-2 forms, tax returns, pay stubs, or self-employment records. The SSA has a specific process for correcting earnings records, which usually involves filling out Form SSA-7008 (Request for Correction of Earnings Record) and submitting it with your supporting documentation. Taking the initiative to correct any errors ensures that your future benefit calculations are based on an accurate and complete work history.

Strategic Considerations and Future Planning

Understanding Social Security credits goes beyond mere calculation; it’s about strategic planning for your long-term financial well-being.

Maximizing Your Credit Earning Potential

While the maximum credits you can earn is capped at four per year, ensuring you consistently hit this threshold is paramount. For individuals with variable income, part-time work, or those transitioning between jobs, it’s important to monitor your earnings to ensure you meet the minimum for four credits annually. For example, if you’re considering reducing your work hours or taking a sabbatical, be mindful of how this might impact your ability to earn the necessary credits, especially if you haven’t yet reached the 40-credit threshold. Proactive financial planning can involve ensuring at least minimum earnings to secure those four credits each year, particularly for individuals in their early career stages.

The Long-Term Impact of Credits on Your Financial Future

The accumulation of Social Security credits is a long-game strategy. While 40 credits might seem like a distant goal for someone just starting their career, consistently earning them ensures a safety net for retirement and beyond. The earlier you begin contributing and tracking your credits, the more secure your financial future becomes. It provides a foundational layer of income that, when combined with personal savings, investments, and pensions, forms a robust retirement plan. Furthermore, understanding the credit requirements for disability and survivor benefits allows you to assess your family’s financial resilience in the face of unexpected life events.

Staying Informed About Social Security Updates

Social Security is a dynamic system, subject to legislative changes, economic adjustments, and policy updates. The annual earnings threshold for credits, cost-of-living adjustments (COLAs) for benefits, and other parameters are reviewed and updated regularly. Staying informed about these changes through reliable sources like the SSA’s official website, financial news outlets, and professional financial advisors is crucial. An informed individual is better equipped to adapt their financial planning strategies to ensure they continue to maximize their Social Security benefits and protect their financial well-being.

In conclusion, Social Security credits are the bedrock of your entitlement to vital benefits. By understanding how they are calculated, earned, and tracked, you gain powerful insights into securing your financial future. This knowledge empowers you to make informed decisions, monitor your progress, and ensure that the contributions you’ve made throughout your working life translate into the financial security you and your family deserve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.