The year 1929 stands as a stark reminder of the fragility of financial markets and the devastating consequences of unchecked speculation and systemic vulnerabilities. Often referred to as the “Great Crash,” the market downturn that began in October of that year wasn’t merely a blip on the economic radar; it was a cataclysmic event that signaled the end of the “Roaring Twenties” and ushered in the Great Depression, a decade of unprecedented economic hardship. Understanding the complex web of factors that contributed to this monumental collapse offers invaluable insights into market dynamics, regulatory necessity, and the enduring principles of sound financial management. Far from being a simple case of investor panic, the 1929 crash was the culmination of a decade of economic imbalances, speculative excesses, and critical policy failures, whose lessons continue to resonate in modern financial discourse.

The Roaring Twenties: A Foundation of Instability

The decade preceding the crash, famously dubbed the “Roaring Twenties,” was characterized by rapid industrial growth, technological innovation, and a pervasive sense of optimism. Emerging from the shadow of World War I, America enjoyed an economic boom that saw rising corporate profits, increasing consumer spending, and a vibrant cultural scene. However, beneath this glittering façade of prosperity, fundamental economic weaknesses and dangerous financial practices were taking root, laying the groundwork for the impending collapse.

Unfettered Optimism and Speculation

The widespread belief in a perpetually rising market was perhaps the most potent psychological factor driving the speculative bubble. Ordinary citizens, encouraged by stories of overnight millionaires and seemingly endless gains, poured their life savings into the stock market. Brokers and financial commentators often propagated the notion that stocks were a foolproof investment, leading to a phenomenon known as “irrational exuberance.” This unchecked optimism created a self-fulfilling prophecy for a time, pushing stock prices to unsustainable levels far beyond their underlying intrinsic value. The average investor, often with limited financial literacy, saw the market as a guaranteed path to wealth, fueling a speculative frenzy that divorced asset prices from economic reality. This detachment is a crucial lesson in investment psychology, reminding us that market sentiment, while powerful in the short term, is a poor foundation for long-term value.

Easy Credit and Margin Buying

Central to the speculative fervor was the widespread availability of easy credit. Banks and brokers were eager to lend money to investors, often requiring only a small down payment—as little as 10%—to purchase stocks. This practice, known as buying on margin, allowed investors to control large blocks of stock with minimal personal capital. While amplifying potential gains in a rising market, it also magnified potential losses exponentially when prices fell. When the market began to turn, margin calls—demands for investors to deposit additional funds to cover their loans—triggered a massive sell-off. Unable to meet these calls, investors were forced to liquidate their holdings, driving prices down further in a vicious cycle. The proliferation of margin buying essentially allowed a greater number of people to participate in the speculation, using borrowed money to inflate asset prices, thereby creating a highly leveraged and inherently unstable market. This highlights the dangers of excessive leverage in any financial instrument, a lesson repeatedly learned throughout history.

Deep-Seated Economic Vulnerabilities

While the speculative bubble and easy credit were the most visible culprits, the American economy of the 1920s harbored several deep-seated structural flaws that made it particularly susceptible to a crisis. These underlying weaknesses meant that even without the stock market crash, the economic system was teetering on the brink of an eventual downturn.

Agricultural Distress and Industrial Overproduction

Despite the urban prosperity, a significant segment of the American economy, particularly agriculture, was in a prolonged depression throughout the 1920s. Farmers, who had expanded production during WWI to meet European demand, faced plummeting prices and mounting debt in the post-war era as European agriculture recovered. This severely reduced the purchasing power of a large portion of the population. Simultaneously, several key industries, like automobiles and housing, began to experience overproduction by the late 1920s. Factories produced goods faster than consumers could buy them, leading to accumulating inventories and eventual production cutbacks. This created a significant imbalance between supply and demand, foreshadowing a contraction in manufacturing and employment. The lack of a robust domestic demand base meant that the economy was structurally weak, unable to absorb shocks once the speculative engine stalled.

Unequal Wealth Distribution and Demand Imbalance

The economic gains of the Roaring Twenties were not evenly distributed. A disproportionately small percentage of the population controlled a vast amount of the nation’s wealth, leading to a substantial demand imbalance. While the wealthy had ample funds for investment and luxury goods, the vast majority of Americans struggled with stagnant wages and limited savings. This meant that the economy relied heavily on the spending of the affluent few and the credit-fueled purchases of the working class. When the wealthy began to pull back their investments or when credit tightened, there wasn’t enough broad-based consumer demand to sustain economic growth. This unequal distribution of purchasing power made the economy inherently fragile, lacking the broad consumer base necessary for sustained prosperity and making it vulnerable to any dip in spending from the top tier.

Flawed Monetary Policy and Regulatory Lapses

The Federal Reserve, established in 1913, was still relatively new and largely untested in managing a booming economy on the brink of collapse. Its policies in the late 1920s were, in retrospect, insufficient and often counterproductive. Initially, the Fed kept interest rates low, inadvertently fueling the speculative boom by making credit cheap. As the bubble grew, the Fed belatedly attempted to curb speculation by raising interest rates in 1928 and 1929. However, these actions were too little, too late, and primarily succeeded in making credit scarce for legitimate businesses while doing little to rein in the rampant stock market speculation, as money flowed into the market from other sources. Furthermore, the almost complete absence of government regulation over financial markets allowed unethical practices and systemic risks to proliferate. There were no robust mechanisms to oversee stock exchanges, regulate margin lending, or ensure transparency. This regulatory void allowed the speculative bubble to inflate without checks and balances, illustrating the critical role of well-designed financial regulation in preventing market excesses.

The Catalyst: From Peak to Precipice

By the autumn of 1929, the intricate web of speculation, easy credit, and underlying economic weaknesses had stretched to its breaking point. A series of events, both psychological and economic, coalesced to trigger the inevitable collapse.

The Market Peak and Initial Warning Signs

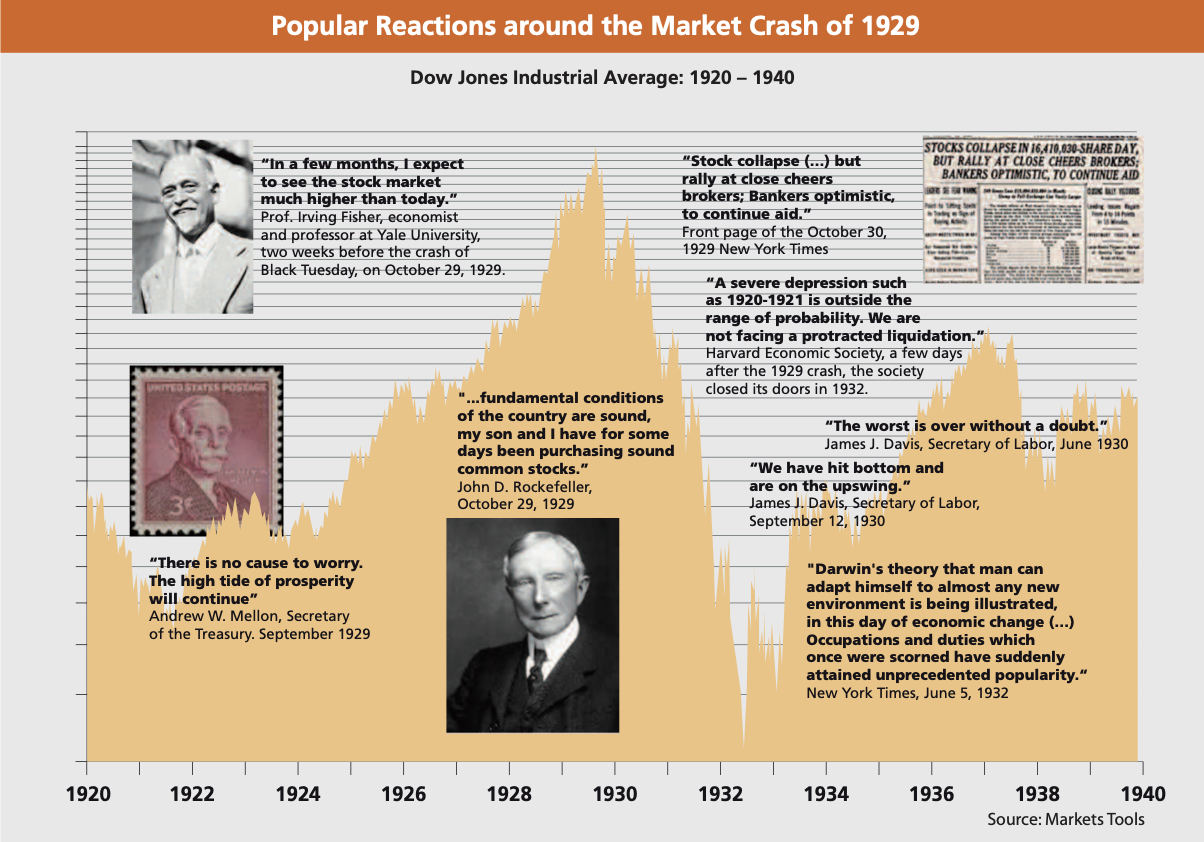

The stock market reached its peak on September 3, 1929, with the Dow Jones Industrial Average closing at 381.17. For several weeks thereafter, the market experienced increasing volatility and sporadic declines, signaling that the momentum was fading. While some astute investors and economists, such as Roger Babson, issued warnings about an impending crash, their voices were largely drowned out by the continued optimism of the majority. Small investors, many heavily leveraged, started to feel the pinch as minor dips wiped out their minimal equity. Large institutional investors and insiders began to quietly offload their holdings, sensing the shifting tides. These early tremors, though subtle to the casual observer, were critical indicators that the market’s speculative foundations were eroding.

Black Thursday and Black Tuesday: The Avalanche Begins

The true turning point arrived on Thursday, October 24, 1929, famously known as “Black Thursday.” A sudden, massive wave of selling hit the market, overwhelming the trading systems and sending prices spiraling downwards. Nearly 13 million shares traded hands, more than double the previous record, as panic set in. Leading bankers attempted to stem the tide by pooling resources to buy up blocks of stock, mirroring actions that had successfully averted panic in earlier crises. Their efforts provided a brief respite, and the market showed signs of stabilizing by Friday. However, the reprieve was short-lived. The real devastation occurred on Tuesday, October 29, 1929 – “Black Tuesday.” The market opened to an even greater torrent of selling, with roughly 16 million shares traded. The buying power of the bankers was exhausted, and there was no coordinated effort to halt the freefall. The market simply collapsed, with prices plummeting across the board, wiping out billions of dollars in paper wealth and shattering investor confidence overnight. This day marked the definitive end of the bull market and the beginning of a prolonged and painful bear market.

The Domino Effect and Global Repercussions

The immediate aftermath of the 1929 market crash was not just a financial correction; it initiated a devastating chain reaction that rapidly spread from Wall Street to Main Street and across international borders, morphing into the Great Depression.

Bank Failures and Credit Contraction

One of the most immediate and profound effects of the stock market collapse was the widespread failure of banks. Many banks had invested heavily in the stock market themselves, and the crash decimated their assets. More critically, banks had lent large sums to individuals and brokers for margin buying, and these loans became worthless as stock values evaporated. As public confidence waned, a wave of “bank runs” ensued, where depositors, fearing losing their savings, rushed to withdraw their money. Lacking sufficient reserves, thousands of banks were forced to close, wiping out the savings of countless Americans and further contracting the money supply. This credit crunch crippled businesses, making it nearly impossible for them to obtain loans for expansion or even day-to-day operations, leading to widespread bankruptcies and mass unemployment. The intertwined nature of the financial system meant that the stock market crash directly undermined the stability of the entire banking sector, a critical pillar of any modern economy.

International Economic Entanglements

The economic fallout was not confined to the United States. The global economy of the 1920s was interconnected, particularly due to post-World War I reparations and war debts. As the U.S. economy faltered, American banks recalled loans from European countries, particularly Germany and Austria, which relied on these funds to pay war reparations to France and Britain. In turn, France and Britain used these reparations to repay their own war debts to the U.S. This intricate financial circle broke down, leading to a wave of banking crises and economic contractions across Europe. Furthermore, the U.S. government, in an attempt to protect domestic industries, enacted high tariffs like the Smoot-Hawley Tariff Act in 1930. This provoked retaliatory tariffs from other nations, severely curtailing international trade and deepening the global economic downturn. The crash thus exposed the fragile interdependence of global finance and trade, demonstrating how a crisis in one major economy could quickly cascade into a worldwide depression.

Enduring Lessons and Regulatory Evolution

The catastrophic scale of the 1929 market crash and the subsequent Great Depression served as a harsh but invaluable teacher, fundamentally reshaping financial regulation and economic policy for generations to come.

Birth of Modern Financial Regulation

The most direct and lasting impact of the crash was the overhaul of the U.S. financial regulatory system. Prior to 1929, financial markets operated with minimal government oversight. In response to the crisis, the federal government enacted landmark legislation designed to prevent future collapses. The Glass-Steagall Act of 1933 separated commercial banking from investment banking, aimed at reducing speculative risks within traditional deposit-taking institutions. The Securities Act of 1933 and the Securities Exchange Act of 1934 created the Securities and Exchange Commission (SEC), an independent agency tasked with regulating the stock market, ensuring transparency, and protecting investors from fraud and manipulation. These reforms introduced strict disclosure requirements for companies, regulated margin trading, and established mechanisms to monitor market activity, forming the bedrock of modern financial law. These regulatory frameworks underscore the ongoing tension between market freedom and systemic stability, a balance governments continually strive to achieve.

The Importance of Prudent Financial Practices

Beyond regulatory changes, the 1929 crash ingrained crucial lessons about prudent financial practices, both for institutions and individual investors. It highlighted the dangers of excessive leverage, the perils of herd mentality, and the importance of valuing assets based on fundamentals rather than speculative hype. For policymakers, it underscored the need for vigilant monetary policy, the strategic use of fiscal measures to stabilize the economy, and the critical role of a robust social safety net. For investors, the crash served as a timeless reminder that markets are subject to cycles, and that diversification, long-term perspective, and a healthy skepticism towards “get-rich-quick” schemes are indispensable. The experience of 1929 continues to inform discussions about risk management, systemic safeguards, and the behavioral economics of financial markets, urging a cautious approach to prosperity and a deep respect for the power of collective fear and greed.

The 1929 market crash was a watershed moment in financial history, a complex interplay of speculative frenzy, structural economic weaknesses, and policy missteps. Its causes were multifaceted and deeply intertwined, illustrating how human psychology, economic imbalances, and a lack of regulatory oversight can converge to produce catastrophic outcomes. While the financial landscape and regulatory environment have evolved significantly since the Great Crash, the fundamental lessons it imparts—about the dangers of irrational exuberance, the critical role of sound financial governance, and the importance of understanding the real economy behind market fluctuations—remain as relevant and vital today as they were almost a century ago. Studying this historic event is not just an exercise in revisiting the past; it is an essential component of safeguarding future financial stability and fostering a more resilient economic future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.