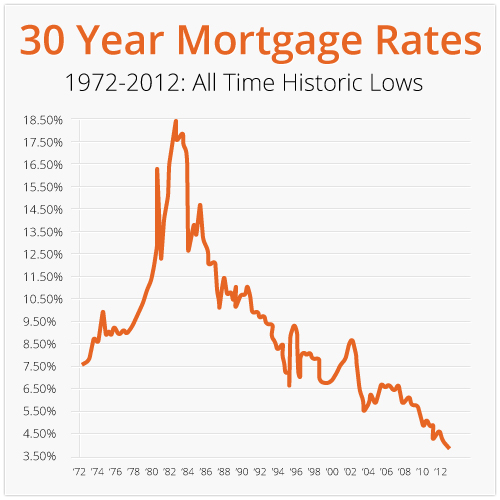

The aspiration of homeownership remains a cornerstone of the American dream, and at the heart of realizing this dream lies the mortgage. Among the myriad financing options available, the 30-year fixed-rate mortgage stands out as the most popular choice, favored by a vast majority of homebuyers for its stability and predictability. Today’s 30-year fixed rate isn’t just a number; it’s a critical barometer of the broader economic climate, a determinant of affordability, and a key factor in the financial planning of millions. Understanding where these rates stand, what influences them, and how they impact your financial decisions is paramount in the current dynamic housing market.

This article delves into the intricacies of the 30-year fixed-rate mortgage, exploring the forces that shape its daily fluctuations, offering strategies for securing the most favorable terms, and discussing the profound implications of current rates on both prospective and existing homeowners. We aim to provide an insightful and engaging perspective, empowering you with the knowledge to navigate one of the most significant financial commitments of a lifetime.

Understanding the 30-Year Fixed-Rate Mortgage

Before diving into current rates and market dynamics, it’s essential to grasp the fundamental nature of the 30-year fixed-rate mortgage. Its enduring popularity stems from a clear and compelling advantage: stability.

Definition and Mechanics

A 30-year fixed-rate mortgage is a loan used to purchase real estate where the interest rate remains constant for the entire 30-year (360-month) term of the loan. This means your principal and interest payment will not change over three decades, providing an unparalleled level of predictability in your monthly housing expenses. The amortization schedule is structured such that early payments are heavily weighted towards interest, gradually shifting more towards principal as the loan matures. Over the full term, borrowers typically pay significantly more in interest than the initial loan amount, highlighting the long-term cost associated with borrowing.

Why It’s Popular

The appeal of the 30-year fixed-rate mortgage is multifaceted. For starters, the extended payment period results in lower monthly payments compared to shorter-term mortgages (like a 15-year fixed rate) for the same loan amount, making homeownership more accessible and affordable on a monthly basis. This lower monthly obligation frees up cash flow, which can be crucial for managing other household expenses, saving for retirement, or investing.

Furthermore, the fixed nature of the interest rate provides an invaluable hedge against inflation and rising interest rates. In an unpredictable economic landscape, knowing exactly what your largest monthly expense will be for the next 30 years offers immense peace of mind. This predictability allows homeowners to budget effectively and plan for their financial future without the anxiety of fluctuating payments seen with adjustable-rate mortgages (ARMs). It’s a foundational financial product that underpins long-term financial stability for many families.

Factors Influencing Today’s Rates

Mortgage rates are not set arbitrarily; they are a complex interplay of various economic indicators, monetary policies, and market forces. Understanding these influences is key to deciphering “what is the 30-year fixed rate today” and anticipating future movements.

Economic Indicators

Several macroeconomic data points significantly sway mortgage rates. Inflation, perhaps the most critical, erodes the purchasing power of money over time. Lenders, to protect their returns, demand higher interest rates when inflation is high or expected to rise. Employment data, such as the monthly jobs report and unemployment rate, indicates the health of the economy. A robust job market suggests strong consumer spending and potential inflation, often pushing rates higher. Conversely, a weakening job market can signal an economic slowdown, potentially leading to lower rates. Gross Domestic Product (GDP) growth, representing the total output of goods and services, is another vital indicator; strong growth can fuel inflation and higher rates.

Federal Reserve Policy

While the Federal Reserve does not directly set mortgage rates, its monetary policy decisions have a profound indirect impact. The Fed primarily influences short-term interest rates through the federal funds rate. When the Fed raises the federal funds rate to combat inflation, it makes borrowing more expensive across the board, typically translating to higher mortgage rates. Conversely, cuts to the federal funds rate aim to stimulate economic activity, often leading to lower mortgage rates. The Fed also engages in quantitative easing (buying bonds) or tightening (selling bonds), which directly affects the supply and demand for mortgage-backed securities, a major component of the mortgage market.

Treasury Yields

The yield on the 10-year Treasury note is often considered a benchmark for long-term interest rates, including mortgage rates. This is because many mortgage lenders use the 10-year Treasury yield as a baseline for pricing their loans, adding a spread for profit and risk. When investors demand higher yields on Treasuries due to inflation concerns or other economic factors, mortgage rates tend to follow suit. The inverse is also true: declining Treasury yields often precede a drop in mortgage rates. Monitoring the 10-year Treasury yield provides a good indication of the direction mortgage rates are likely heading.

Market Demand and Supply

The basic economic principles of supply and demand also play a role. When there’s high demand for mortgages (e.g., during a robust housing market) and lenders have limited capacity or face higher funding costs, rates may increase. Conversely, intense competition among lenders or a slowdown in mortgage applications can lead to more attractive rates as lenders vie for business. The overall health of the housing market, including inventory levels and home prices, can also subtly influence lenders’ risk assessments and pricing strategies.

Geopolitical Events

Unforeseen global events, such as international conflicts, political instability, or major natural disasters, can introduce significant uncertainty into financial markets. In times of global stress, investors often flock to safe-haven assets like U.S. Treasury bonds, which can drive down Treasury yields and, paradoxically, sometimes lead to lower mortgage rates. However, sustained uncertainty can also lead to tighter credit conditions and higher rates as lenders become more risk-averse.

How to Find and Secure the Best 30-Year Fixed Rate

Knowing what influences rates is one thing; actively working to secure the most advantageous rate for your specific situation is another. Even small differences in interest rates can translate into tens of thousands of dollars over 30 years.

The Importance of Shopping Around

This cannot be stressed enough: do not settle for the first quote you receive. Mortgage rates can vary significantly between lenders, sometimes by as much as half a percentage point or more, even on the same day for the same borrower profile. Contact multiple lenders—banks, credit unions, and mortgage brokers—to obtain personalized quotes. Utilize online comparison tools, but always follow up with direct conversations to understand all terms and fees. Each lender assesses risk differently and has varying overheads, leading to diverse offerings.

Improving Your Financial Profile

Lenders evaluate your creditworthiness to determine the risk of lending to you, and this directly impacts the rate you’re offered.

- Credit Score: A strong credit score (generally 740+) signals responsible financial behavior and qualifies you for the lowest available rates. Focus on paying bills on time, keeping credit utilization low, and correcting any errors on your credit report.

- Debt-to-Income (DTI) Ratio: Your DTI is the percentage of your gross monthly income that goes towards debt payments. Lenders prefer a lower DTI (typically below 43%) as it indicates you can comfortably handle additional mortgage payments. Pay down existing debts, especially high-interest ones, before applying for a mortgage.

- Down Payment: A larger down payment reduces the loan amount and represents less risk for the lender. While 20% is often seen as ideal to avoid private mortgage insurance (PMI), even a slightly larger down payment than initially planned can sometimes secure a better rate.

Understanding Rate Quotes and APR

When comparing offers, it’s crucial to look beyond just the interest rate. The Annual Percentage Rate (APR) provides a more comprehensive picture of the true cost of the loan, as it includes the interest rate plus certain upfront fees and costs (like origination fees, discount points, and some closing costs). While the interest rate determines your monthly principal and interest payment, the APR helps you compare the total cost of different loan offers over the life of the loan. A lower interest rate with high fees might result in a higher APR than a slightly higher interest rate with fewer fees.

Locking in Your Rate

Once you find a favorable rate, inquire about locking it in. A rate lock guarantees that the lender will honor a specific interest rate for a set period (typically 30, 45, or 60 days) while your loan application is being processed. This protects you from potential rate increases before your loan closes. Understand the terms of the rate lock, including its duration and any associated fees. If rates drop significantly after you’ve locked, some lenders may offer a “float-down” option, but this often comes with a fee.

The Impact of Current Rates on Borrowers

Current 30-year fixed rates have a profound and immediate impact on both prospective buyers entering the market and existing homeowners considering their options.

Affordability and Monthly Payments

Higher interest rates directly translate to higher monthly mortgage payments for the same loan amount. This reduces purchasing power, meaning buyers might need to consider less expensive homes or make larger down payments to keep their monthly expenses manageable. For example, a difference of just one percentage point on a $300,000 mortgage can alter the monthly payment by hundreds of dollars, significantly affecting a household’s budget. Lower rates, conversely, enhance affordability, allowing buyers to qualify for larger loans or enjoy lower monthly costs for their desired home.

Refinancing Considerations

For existing homeowners, fluctuations in the 30-year fixed rate can trigger opportunities for refinancing. If current rates are significantly lower than the rate on an existing mortgage, refinancing could lead to substantial savings over the loan’s life, a lower monthly payment, or the ability to cash out equity. However, refinancing involves closing costs, so it’s essential to calculate the break-even point to determine if the savings outweigh the upfront expenses. A general rule of thumb is that a rate reduction of at least 0.75% to 1% makes refinancing worth considering, but this is highly dependent on individual circumstances and the length of time you plan to stay in the home.

Equity Building and Long-Term Costs

The interest rate also impacts how quickly you build equity in your home and the total cost of the loan over 30 years. With higher rates, a larger portion of your early payments goes towards interest, meaning principal reduction is slower, and equity accumulation is more gradual. Over three decades, even small differences in rates can accumulate into tens of thousands of dollars in additional interest paid. Understanding this long-term financial commitment is crucial for holistic financial planning and evaluating the true cost of homeownership.

Navigating the Mortgage Market: Future Outlook and Strategic Considerations

The mortgage market is inherently dynamic, influenced by a constant stream of economic data, policy decisions, and global events. While predicting future rates with absolute certainty is impossible, strategic considerations can help you navigate this complex landscape.

Expert Predictions and Market Volatility

Mortgage rate forecasts from economists and financial institutions often provide insights into potential future trends, though they are subject to change. These predictions consider factors like the Fed’s stance on inflation, projected GDP growth, and the strength of the labor market. It’s wise to consult a range of reputable sources, but always remember that market volatility means rates can shift rapidly. Understanding the general consensus and the underlying rationale can inform your decision-making without creating undue pressure to “time the market.”

When to Act: Timing the Market

Attempting to perfectly time the market to secure the absolute lowest rate is often a futile exercise, as rates are influenced by too many unpredictable variables. Instead, focus on your personal financial readiness and housing needs. If you are financially stable, have a solid down payment, a good credit score, and have found a home that meets your requirements, securing a favorable rate today might be more prudent than waiting indefinitely for a hypothetical lower rate that may never materialize. A strong personal financial position can often mitigate the impact of slight rate fluctuations.

Alternative Mortgage Options

While the 30-year fixed-rate mortgage is a popular choice, it’s worth briefly considering alternatives to ensure it’s the best fit for your situation. A 15-year fixed-rate mortgage, for instance, typically offers a lower interest rate and allows you to pay off your home much faster, building equity quicker and significantly reducing total interest paid—though with higher monthly payments. Adjustable-rate mortgages (ARMs) start with a lower fixed rate for an initial period (e.g., 5 or 7 years) before adjusting periodically. ARMs can be appealing for those who plan to sell or refinance before the fixed period ends, but they carry the risk of higher payments if rates rise. Government-backed loans like FHA, VA, and USDA loans offer specific benefits for eligible borrowers, often with more lenient qualification criteria.

The Role of a Financial Advisor

For such a significant financial decision, consulting with a qualified financial advisor can be invaluable. A professional can help you assess your overall financial health, understand the long-term implications of different mortgage options, and integrate your housing decision into your broader financial plan. They can provide personalized guidance, helping you weigh the pros and cons of fixed-rate versus adjustable-rate, and advise on optimal down payment strategies, ensuring your mortgage choice aligns with your individual financial goals.

Conclusion

The question “what is the 30-year fixed rate today” is more than a simple query; it’s a gateway to understanding a complex financial ecosystem that impacts millions of lives. From the stability it offers to the intricate web of economic factors that shape its daily movements, the 30-year fixed-rate mortgage remains a pivotal instrument in personal finance. By understanding its mechanics, recognizing the forces at play, diligently shopping for the best terms, and aligning your choices with your personal financial objectives, you can confidently navigate the mortgage market. Staying informed and making strategic decisions are your most powerful tools in achieving and maintaining the dream of homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.