For millions of Americans, Social Security represents the cornerstone of financial security in their later years. It is the bedrock upon which retirement portfolios are built, providing a steady, inflation-adjusted stream of income that is guaranteed for life. However, one of the most common questions financial advisors face is deceptively simple: “How much is Social Security?”

The answer, unfortunately, is rarely a single number. Because the Social Security Administration (SSA) uses a complex formula based on your unique work history, the age at which you claim, and your lifetime earnings, the amount varies significantly from person to person. To navigate your financial future effectively, you must understand the mechanics behind these calculations and how your choices today dictate your monthly check tomorrow.

1. The Foundation of the Calculation: Your Earnings History

To determine how much Social Security you will receive, the SSA first looks at your entire work history. Unlike some private pension plans that might only look at your final five years of salary, Social Security is a marathon, not a sprint.

The Role of Your 35 Highest-Earning Years

The SSA calculates your benefit based on your “Average Indexed Monthly Earnings” (AIME). To find this, they look at your earnings over your entire career and select the 35 years in which you earned the most, adjusted for inflation. If you worked fewer than 35 years, the SSA enters “zero” for the remaining years, which can significantly drag down your average and, consequently, your monthly benefit. For those looking to maximize their payout, ensuring a full 35-year work history is the first step toward a higher check.

Understanding the “Bend Points” Formula

Once your AIME is established, the SSA applies a formula to determine your Primary Insurance Amount (PIA). This formula is progressive, meaning it is designed to replace a higher percentage of income for lower-wage earners than for higher-wage earners. The formula uses “bend points”—specific dollar thresholds that change annually. For example, the SSA might replace 90% of your first few hundred dollars of average monthly earnings, 32% of the middle range, and only 15% of earnings above a certain level. This ensures a safety net for all while still rewarding those who contributed more into the system.

How Inflation Adjustments (COLA) Impact Your Payout

A unique and vital feature of Social Security is the Cost-of-Living Adjustment (COLA). Every year, the SSA reviews the Consumer Price Index to determine if the cost of goods and services has risen. If it has, benefits are increased to ensure that retirees do not lose purchasing power. While some years see 0% increases, others—especially during periods of high inflation—can see jumps of 8% or more. This makes Social Security a powerful hedge against inflation that few other financial instruments can match.

2. The Impact of Timing: When You Claim Matters

Perhaps the most significant factor in the “how much” equation is not what you earned, but when you decide to start receiving checks. You have a window of opportunity that typically begins at age 62 and extends to age 70.

Filing at Age 62: The Cost of Early Retirement

While you can technically begin receiving Social Security at age 62, doing so comes at a permanent cost. If you claim early, your monthly benefit is reduced by a fraction of a percent for each month before your Full Retirement Age (FRA). For someone whose FRA is 67, claiming at 62 results in a permanent 30% reduction in their monthly benefit. While this provides immediate cash flow, it significantly reduces the total lifetime “wealth” generated by the program if you live a long life.

Reaching Full Retirement Age (FRA)

Your Full Retirement Age is the point at which you are entitled to 100% of your calculated benefit (your PIA). For anyone born in 1960 or later, the FRA is 67. Reaching this milestone is often seen as the “neutral” point in financial planning. At this age, you can also work as much as you want without having any of your benefits temporarily withheld due to the “earnings test” limit, which applies only to those who claim before their FRA.

The 8% Bonus: Incentives for Delaying Until Age 70

For those who can afford to wait, the rewards are substantial. For every year you delay claiming Social Security past your FRA (up until age 70), your benefit increases by approximately 8% per year in “delayed retirement credits.” This means that by waiting from age 67 to 70, you can increase your monthly check by 24%. This is a guaranteed, inflation-indexed return that is virtually impossible to find in the private market, making it one of the most effective ways to boost your retirement income.

3. Estimating Your Specific Benefit Amount

While individual calculations vary, we can look at current averages and maximums to get a sense of the landscape. As of 2024, the numbers reflect a wide range of financial realities for American workers.

Average Monthly Benefits for Different Groups

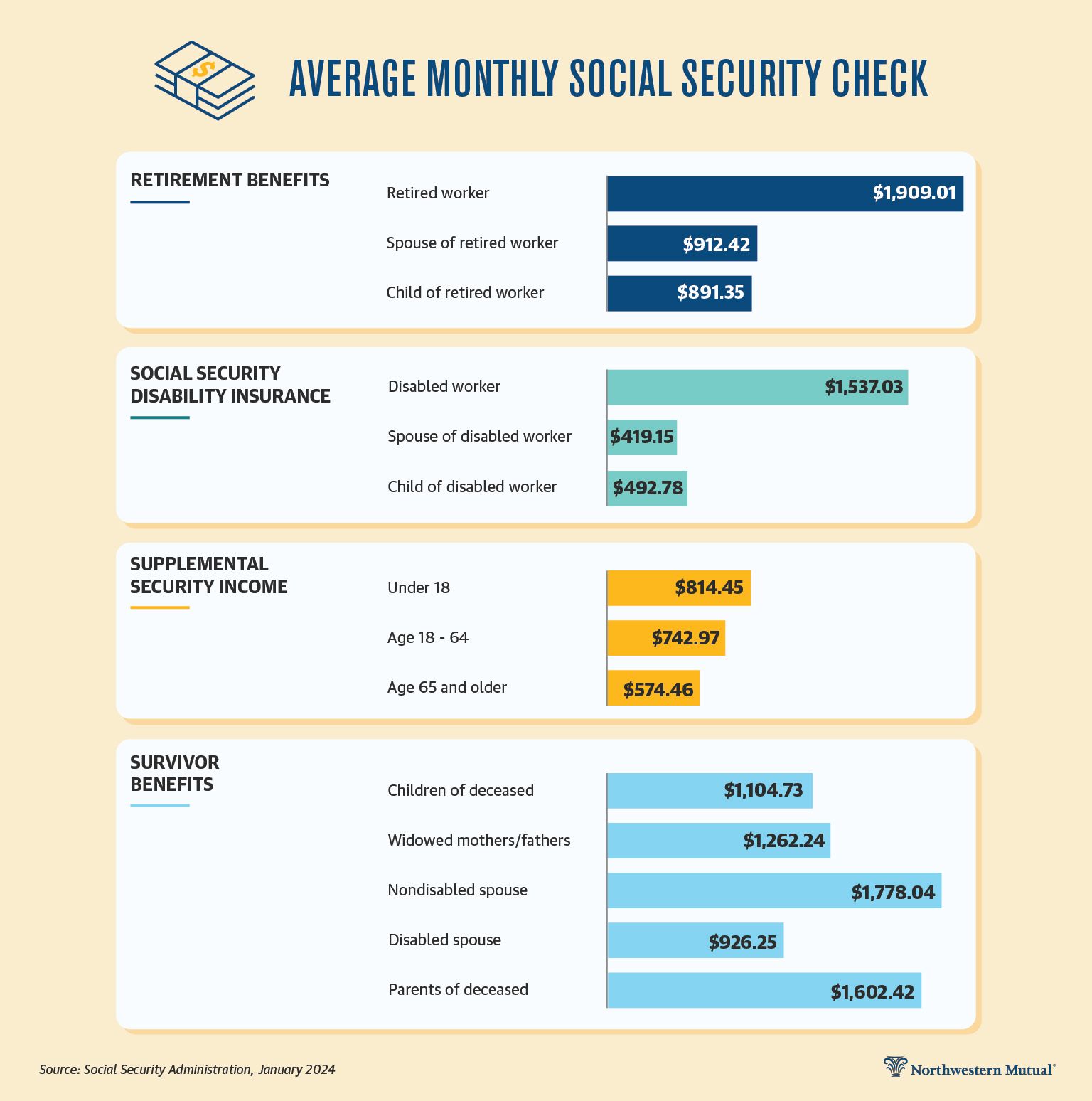

As of early 2024, the average monthly Social Security benefit for a retired worker is approximately $1,900. While this provides a baseline, it is rarely enough to cover all expenses in modern retirement. For couples where both spouses have worked, the combined household benefit often nears $3,000 to $4,000, which provides a much sturdier foundation. Knowing these averages helps retirees realize that Social Security is intended to be a supplement—usually replacing about 40% of pre-retirement income—rather than a total replacement.

The Maximum Taxable Earnings Limit

There is a ceiling on how much you can contribute to Social Security, and consequently, how much you can get out. The “taxable maximum” is the cap on earnings subject to the Social Security tax (in 2024, this is $168,600). If you earn more than this amount, you do not pay Social Security taxes on the excess, but those earnings also do not count toward your future benefit. For high earners who have hit this cap for 35 years and delay filing until age 70, the maximum monthly benefit can exceed $4,800.

Using the Social Security Administration’s Tools

The most accurate way to answer “how much” is to create a “my Social Security” account on the official SSA website. This tool provides personalized estimates based on your actual earnings record. It allows you to toggle between different claiming ages to see exactly how much you would receive at 62, FRA, or 70. Checking this statement annually is a vital part of proactive personal finance, as it allows you to catch any errors in your earnings history before they become permanent.

4. External Factors That Influence Your Net Benefit

It is important to remember that the “gross” amount you see on your SSA statement is not always the “net” amount that hits your bank account. Several factors can trim your monthly check.

Taxation of Social Security Benefits

Many retirees are surprised to learn that Social Security benefits can be taxable. If your “combined income” (adjusted gross income + nontaxable interest + half of your Social Security benefits) exceeds a certain threshold, you may owe federal income tax on up to 85% of your benefits. For individuals, this threshold starts at $25,000; for married couples filing jointly, it starts at $32,000. Proper tax planning, such as managing withdrawals from traditional IRAs, can help minimize this “tax torpedo.”

Medicare Premium Deductions

For the vast majority of retirees, Medicare Part B premiums are automatically deducted from their Social Security checks. As health care costs rise, these premiums can take a noticeable bite out of your monthly income. When estimating “how much” you will have for groceries and housing, you must factor in these deductions, which often increase annually alongside the COLA.

The Windfall Elimination Provision (WEP) and GPO

If you worked in a job where you did not pay Social Security taxes (such as certain government or civil service positions) and also qualify for Social Security from other work, your benefits may be reduced. The Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) are designed to prevent “double-dipping” into both a government pension and Social Security in a way that the SSA deems unfair. Understanding these provisions is critical for teachers, police officers, and other public servants.

5. Strategic Planning for Long-Term Solvency

Determining how much you will receive is only half the battle; the other half is deciding how that money fits into your broader financial ecosystem.

Bridging the Gap with 401(k)s and IRAs

Since Social Security typically only replaces 40% of income, the remaining 60% must come from personal savings, such as 401(k)s, IRAs, or brokerage accounts. A common strategy for those who want to maximize their Social Security is to use their private savings to “bridge the gap” between retirement and age 70. By spending down some retirement assets early to allow Social Security to grow by 8% a year, you effectively “buy” a higher inflation-protected annuity for the rest of your life.

Spousal and Survivor Benefit Considerations

“How much” is also a question of household security. A lower-earning spouse is often eligible for a spousal benefit worth up to 50% of the higher earner’s PIA. Furthermore, survivor benefits allow a widowed spouse to inherit 100% of the deceased spouse’s monthly benefit (if it is higher than their own). For the higher-earning spouse, delaying benefits until age 70 isn’t just about their own check; it is about ensuring the highest possible “insurance policy” for their surviving spouse.

Conclusion: A Dynamic Piece of the Financial Puzzle

Social Security is more than just a government program; it is a dynamic financial asset. While the “average” check might be $1,900, your personal “how much” is a variable you can influence through your career longevity, your income growth, and your patience in claiming. By understanding the underlying math—from the 35-year average to the 8% annual delay credits—you can move from guesswork to a strategy that ensures a dignified and financially secure retirement. Social Security remains one of the most successful social programs in history, and with the right planning, it can be the most stable component of your personal wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.