In the complex ecosystem of global finance, few instruments carry as much weight or influence as the 10-year U.S. Treasury note. Often referred to as the “benchmark” security, it serves as a vital pulse point for the health of the United States economy and a foundational pillar for diversified investment portfolios. Whether you are a retail investor looking for a safe haven for your savings or a homeowner wondering why mortgage rates just climbed, the 10-year Treasury note is likely the silent engine driving those fluctuations.

To master the world of personal finance and investing, one must look beyond simple stocks and savings accounts. Understanding the mechanics, risks, and strategic advantages of 10-year Treasury notes is essential for anyone seeking to build long-term wealth while managing market volatility.

What Are 10-Year Treasury Notes and How Do They Work?

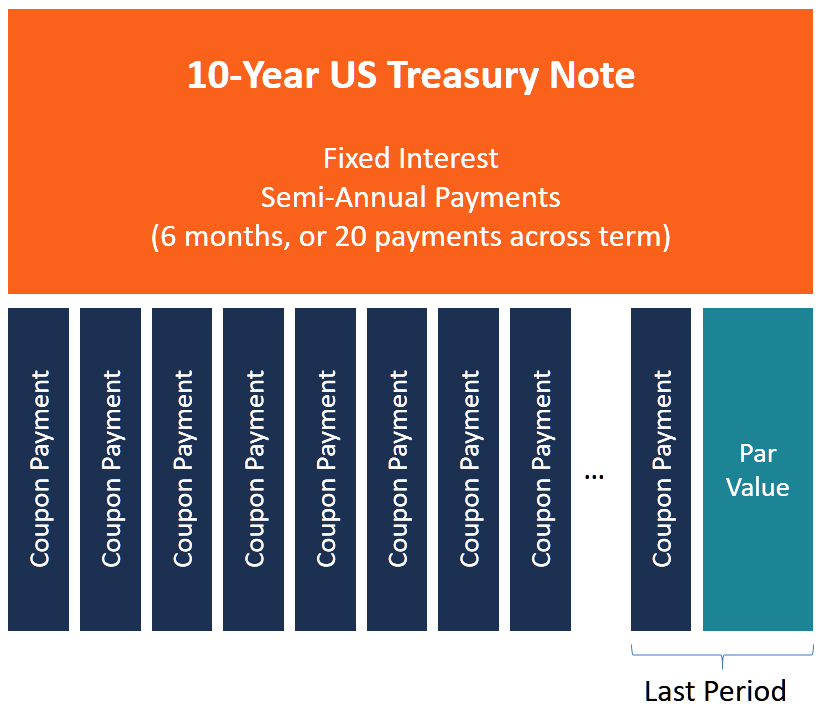

At its most fundamental level, a 10-year Treasury note (T-note) is a debt obligation issued by the United States Department of the Treasury. When you purchase a T-note, you are effectively lending money to the federal government for a period of ten years. In exchange for this loan, the government agrees to pay you a fixed rate of interest every six months until the note matures, at which point they return the full face value (par value) of the note to you.

Definition and Issuance

Treasury notes are part of a family of government securities that include Treasury bills (short-term), Treasury notes (intermediate-term), and Treasury bonds (long-term). The 10-year note sits in the “sweet spot” of the intermediate-term category. They are issued in increments of $100, making them highly accessible to individual investors, though they are traded in blocks of millions by institutional players like central banks and pension funds.

The U.S. government holds regular auctions to sell these notes to finance its operations and pay off existing debt. During these auctions, the interest rate (or “yield”) is determined by market demand. If many investors want the safety of government debt, the price goes up and the yield goes down. Conversely, if investors are seeking higher returns elsewhere, the government must offer a higher yield to attract buyers.

Fixed Interest Payments (Coupons)

The interest paid on a T-note is known as the “coupon.” For example, if you buy a $1,000 note with a 4% coupon rate, you will receive $40 a year, typically paid in two $20 installments. Because this rate is fixed at the time of issuance, T-notes provide a predictable stream of income, which is why they are a staple in “fixed-income” investing. This predictability is particularly attractive to retirees or those with a low risk tolerance.

Maturity and Principal Repayment

The “10-year” designation refers to the duration of the loan. From the date of issuance, the government has ten years to use your capital. On the date of maturity, the “term” ends. The final interest payment is made, and the original principal is returned to the investor. While you can sell your note on the secondary market before those ten years are up, holding it to maturity guarantees the return of your initial investment, provided the U.S. government does not default—an event that has historically never occurred.

Why the 10-Year Yield Matters to Every Investor

While the notes themselves are investment vehicles, the “yield” (the annual return on the investment) is arguably the most important number in the financial world. It acts as a baseline for almost every other type of interest rate.

The Benchmark for Consumer Loans and Mortgages

If you have ever applied for a 30-year fixed-rate mortgage, you may have noticed that mortgage rates tend to move in tandem with the 10-year Treasury yield. Lenders use the 10-year note as a “risk-free” benchmark. Since lending to the U.S. government is considered the safest possible investment, banks will always charge more to lend to a consumer. When the 10-year yield rises, banks raise interest rates on mortgages, auto loans, and corporate debt to maintain their profit margins relative to that “risk-free” alternative.

A Barometer for Economic Sentiment

The yield on the 10-year note is a window into the collective psyche of investors. When investors are optimistic about the economy, they tend to move money out of “safe” Treasuries and into “risky” stocks. This selling pressure causes Treasury prices to fall and yields to rise.

On the other hand, during times of geopolitical tension or economic recession, investors participate in a “flight to safety.” They buy 10-year notes in massive quantities, driving prices up and yields down. Therefore, a falling 10-year yield is often a signal that the market expects an economic slowdown.

Relationship with Inflation and Interest Rates

Inflation is the natural enemy of the fixed-income investor. If you are locked into a 3% return but inflation rises to 5%, you are effectively losing 2% of your purchasing power every year. Consequently, when inflation expectations rise, investors demand higher yields on 10-year notes to compensate for that loss. This is why the Federal Reserve keeps a close eye on the 10-year yield; it tells them whether the market believes their monetary policy is successfully containing inflation.

The Benefits and Risks of Investing in 10-Year Treasuries

No investment is without trade-offs. While 10-year T-notes are frequently cited as the gold standard of safety, they carry specific risks that every participant in the money markets should understand.

Safety and Government Backing

The primary draw of the 10-year note is its credit quality. These securities are backed by the “full faith and credit” of the U.S. government. Unlike corporate bonds, where a company might go bankrupt, the U.S. government has the power to tax and print money to meet its obligations. For an investor focused on capital preservation, there is no safer place to park cash for a decade.

Portfolio Diversification and Hedging

In a balanced portfolio, Treasuries act as a shock absorber. Usually, when the stock market crashes, Treasury notes gain value. This inverse relationship allows investors to hedge their bets. If your equity portfolio drops 20%, a rise in your bond holdings can help mitigate the overall loss, preventing emotional “panic selling” and keeping your long-term financial strategy on track.

Interest Rate Risk and Opportunity Cost

The greatest risk to a T-note holder is “interest rate risk.” If you buy a 10-year note today at a 3% yield and interest rates suddenly jump to 5% next year, your 3% note is now less valuable to other investors. If you need to sell it before it matures, you will likely have to sell it at a discount (less than what you paid).

Additionally, there is the risk of “opportunity cost.” By locking your money away for ten years at a fixed rate, you might miss out on the explosive gains of the stock market or higher interest rates offered by other financial instruments later in the decade.

How to Purchase and Manage Treasury Notes

In the modern era, accessing government debt has become remarkably simple for the average person. You no longer need a high-powered broker to participate in the bond market.

Buying Directly via TreasuryDirect

The most straightforward way to buy 10-year notes is through TreasuryDirect.gov, the official portal run by the U.S. Department of the Treasury. Here, you can buy notes at auction without paying a commission. The platform allows you to set up automatic reinvestments, where the principal from a maturing note is immediately used to buy a new one, creating a continuous cycle of interest income.

Secondary Market Trading and Brokerages

If you want more flexibility, you can buy 10-year notes through a traditional brokerage account (like Charles Schwab, Fidelity, or Vanguard). Buying on the secondary market allows you to see the “bid/ask” spread and sell your notes at any time before maturity. This is essential for investors who may need liquidity and cannot commit to holding the note for the full ten-year duration.

Treasury ETFs and Mutual Funds

For those who prefer a “hands-off” approach, Treasury Exchange-Traded Funds (ETFs) are an excellent option. Funds like the iShares 7-10 Year Treasury Bond ETF (IEF) hold a basket of Treasury notes. When you buy a share of the ETF, you get exposure to the 10-year yield without having to manage individual bonds or worry about maturity dates. This provides instant diversification and high liquidity.

The Role of 10-Year Notes in a Modern Investment Strategy

As you refine your approach to money management, the 10-year note should be viewed as a tactical tool rather than just a stagnant savings vehicle.

Tax Advantages and Exemptions

One often-overlooked benefit of Treasury notes is their tax treatment. While the interest you earn is subject to federal income tax, it is exempt from state and local taxes. For investors living in high-tax states like California or New York, this “tax-equivalent yield” can make Treasuries much more attractive than corporate bonds or high-yield savings accounts that are taxed at every level.

Rebalancing During Market Volatility

A sophisticated investor uses 10-year notes to “rebalance.” When the stock market is booming and your stock allocation grows too large, you can sell some stocks and move the profits into the stability of 10-year Treasuries. Conversely, when the market dips and Treasuries rise in value, you can sell your notes to buy “discounted” stocks. This “buy low, sell high” rhythm is facilitated by the relative stability of the 10-year note.

Conclusion: The Anchor of Your Financial Future

The 10-year Treasury note is more than just a government IOU; it is a fundamental building block of the global financial system. By understanding how these notes work—from their role as an economic benchmark to their utility as a tax-advantaged safe haven—you can make more informed decisions about your own money. Whether you use them to hedge against a recession, generate steady income, or simply to track where mortgage rates are headed, the 10-year Treasury note remains an essential instrument in the toolkit of every serious investor.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.