Economic regulation represents the framework of rules, laws, and administrative codes that govern the behavior of businesses and individuals within a financial ecosystem. Far from being a mere collection of restrictive “red tape,” regulation serves as the invisible infrastructure that allows modern markets to function with a sense of predictability and fairness. In an ideal economic system, regulation balances the drive for private profit with the necessity of public interest, ensuring that the pursuit of wealth does not lead to systemic collapse or the exploitation of participants.

For investors, business owners, and everyday consumers, understanding the nuances of regulation is essential. It dictates how capital flows, how risks are mitigated, and how competition is maintained. Without a robust regulatory framework, the “invisible hand” of the market might quickly turn into a fist, favoring those with the most power at the expense of market integrity. This article explores the multifaceted role of regulation within the “Money” niche, focusing on its impact on finance, investment, and business operations.

Defining Economic Regulation: The Foundation of Modern Markets

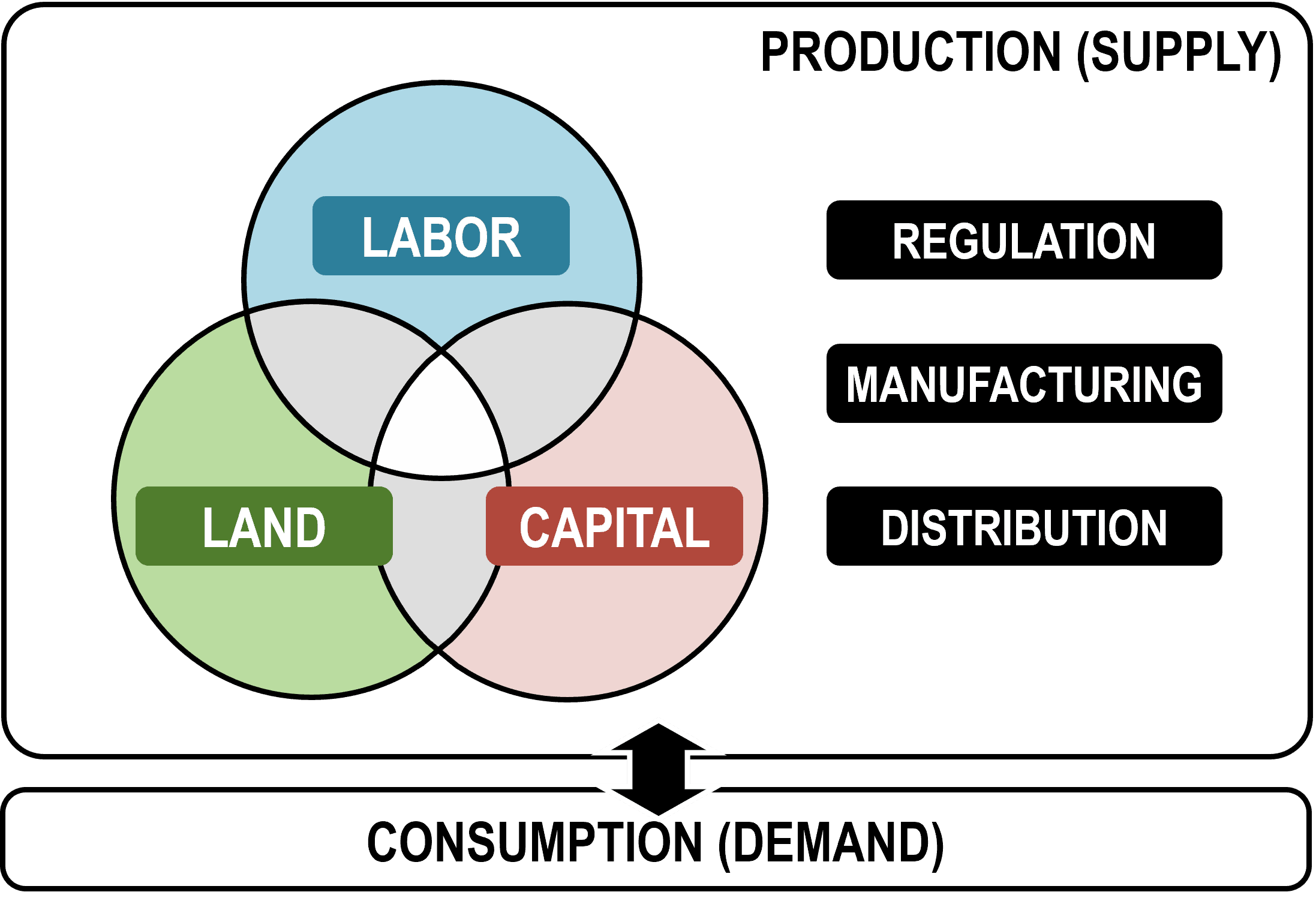

At its core, economic regulation is the intervention of the government or designated agencies in the market to influence the behavior of private entities. This intervention is typically justified by “market failures”—situations where the free market, left to its own devices, fails to allocate resources efficiently or fairly.

The Rationale Behind Government Intervention

The primary driver of regulation is the correction of externalities and information asymmetry. In the world of finance, information is the most valuable currency. If a corporation knows its internal finances are failing but continues to solicit investment without disclosure, the market fails. Regulation, such as the mandate for audited financial statements, ensures that all participants have access to accurate information. Furthermore, regulation addresses monopolies. When a single entity gains total control over a sector, price discovery vanishes. Anti-trust regulations are designed to break these bottlenecks, fostering a competitive environment where prices are determined by supply and demand rather than executive fiat.

Direct vs. Indirect Regulation

Regulation can be categorized into direct and indirect forms. Direct regulation involves specific mandates on prices, entry into a market, or the quality of service. For example, utility companies are often subject to price caps because they operate as natural monopolies. Indirect regulation, on the other hand, focuses on the broader environment. This includes tax codes, labor laws, and environmental standards. While these may not dictate the price of a stock or a product, they significantly impact the cost of doing business and, by extension, the valuation of companies and the attractiveness of certain investment sectors.

The Impact of Regulation on Investment and Asset Protection

For anyone involved in personal finance or institutional investing, regulation is the primary safeguard for their capital. The financial markets are inherently risky, but regulatory bodies work to ensure that those risks are transparent and manageable rather than fraudulent.

Enhancing Market Transparency and Fairness

In the United States, the Securities and Exchange Commission (SEC) serves as the “watchdog” of Wall Street. Its regulations regarding “insider trading” are pivotal. If individuals with non-public information were allowed to trade freely, the average investor would be at a permanent disadvantage, eventually leading to a withdrawal of capital from the markets. By enforcing transparency, regulation builds the trust necessary for retail and institutional investors to participate in the stock and bond markets. This trust is what provides companies with the liquidity they need to grow, creating a virtuous cycle of investment and economic expansion.

Mitigating Systemic Risk in Banking

The banking sector is perhaps the most heavily regulated industry in any economic system. This is because banks are the custodians of the public’s money. Regulations such as the Basel Accords establish international standards for “capital adequacy”—essentially requiring banks to hold a certain amount of liquid assets against their riskier loans. Following the 2008 financial crisis, regulations like the Dodd-Frank Act were implemented to prevent “too big to fail” institutions from taking excessive risks with depositor money. For the individual, these regulations mean that their savings are protected (often via deposit insurance like the FDIC) and that the financial system is less likely to suffer a catastrophic “run” that could wipe out personal wealth.

Regulation’s Role in Business Strategy and Corporate Finance

From the perspective of a business owner or a Chief Financial Officer (CFO), regulation is often viewed as a compliance cost. However, a more sophisticated view recognizes regulation as a strategic boundary that can actually drive innovation and long-term value.

Compliance as a Competitive Advantage

While the cost of complying with financial regulations (such as Sarbanes-Oxley or GDPR) can be high, companies that excel in governance often enjoy a lower cost of capital. Investors are more willing to lend money at lower interest rates to businesses that demonstrate rigorous compliance and ethical financial reporting. In this sense, regulation acts as a filter; it separates high-quality, sustainable businesses from those that are cutting corners. In the modern era, the rise of ESG (Environmental, Social, and Governance) regulations has forced companies to look beyond quarterly profits, encouraging investments in sustainable practices that can protect the business from future legal and environmental liabilities.

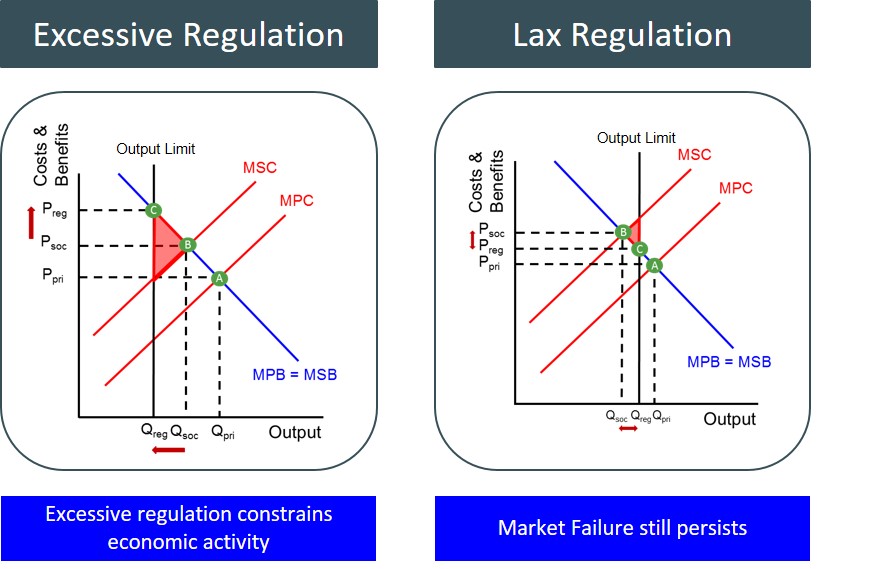

The Cost of Over-Regulation vs. The Risks of Deregulation

The debate within economic circles often centers on the “Goldilocks” zone of regulation—not too much, not too little. Over-regulation can stifle side hustles and small businesses by creating high “barriers to entry.” If a startup needs a fleet of lawyers just to navigate the initial paperwork, innovation is hampered. Conversely, deregulation—the removal of rules—can lead to rapid short-term growth but often at the cost of long-term stability. The history of the “Money” niche is littered with examples of deregulated markets that boomed and then spectacularly crashed, such as the Savings and Loan crisis of the 1980s. Finding the balance is the constant challenge of economic policy.

Macroeconomic Stability and the Role of Central Regulatory Bodies

Beyond individual businesses and investments, regulation plays a critical role in the “big picture” of the economy. This is often managed through central banks and international organizations that regulate the flow of money itself.

Monetary Policy as a Regulatory Tool

Central banks, such as the Federal Reserve, regulate the economy through monetary policy. By adjusting interest rates and controlling the money supply, they regulate inflation and employment levels. When the economy is “overheating” (inflation is too high), the central bank raises rates, making it more expensive to borrow money. This is a form of macro-regulation that affects every facet of finance, from mortgage rates to corporate bond yields. Understanding these regulatory signals is key for anyone involved in investing or business finance, as it dictates the timing of capital expenditures and the shifting of asset allocations.

Global Financial Integration and Cross-Border Standards

In a globalized economy, regulation is no longer confined to national borders. Entities like the International Monetary Fund (IMF) and the World Trade Organization (WTO) help harmonize regulations across countries. For businesses looking to expand internationally, these regulations provide a standard playbook. For example, international accounting standards (IFRS) allow an investor in London to reliably compare the financial health of a company in Tokyo with one in New York. This cross-border regulatory cohesion reduces the friction of international trade and allows for the global movement of capital, which is the engine of modern wealth creation.

Conclusion: The Evolving Landscape of Economic Regulation

Regulation in an economic system is not a static set of rules but an evolving response to new financial realities. As we move further into the digital age, we are seeing the emergence of new regulatory frontiers, such as the oversight of cryptocurrency, decentralized finance (DeFi), and AI-driven algorithmic trading.

For the individual focused on “Money”—whether through personal finance, investing, or business—regulation should be viewed as the “rules of the game.” While these rules can sometimes be frustrating or costly, they are what prevent the game from descending into chaos. A well-regulated economic system provides the stability needed for long-term planning, the transparency required for confident investing, and the protection necessary to ensure that the fruits of labor and capital are preserved. By staying informed about regulatory shifts, participants in the economic system can better navigate risks and seize the opportunities that arise within a structured, fair, and flourishing marketplace.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.