In the world of high-stakes finance and commodity trading, the term “blue blood” has historically referred to the aristocratic elite. However, in the modern pharmaceutical and biotechnology sectors, blue blood is a literal, tangible asset—a biological “liquid gold” that underpins a multi-billion-dollar global safety infrastructure. While most of the animal kingdom relies on iron-based hemoglobin to transport oxygen, a select group of creatures utilizes copper-based hemocyanin, resulting in a vibrant blue hue.

From a financial perspective, these creatures are not just biological wonders; they are critical nodes in a global supply chain. This article explores the economic landscape of blue blood, the market forces driving its demand, and the investment risks posed by synthetic disruption in the life sciences sector.

The Billion-Dollar Biological Asset: Why Blue Blood is a Financial Powerhouse

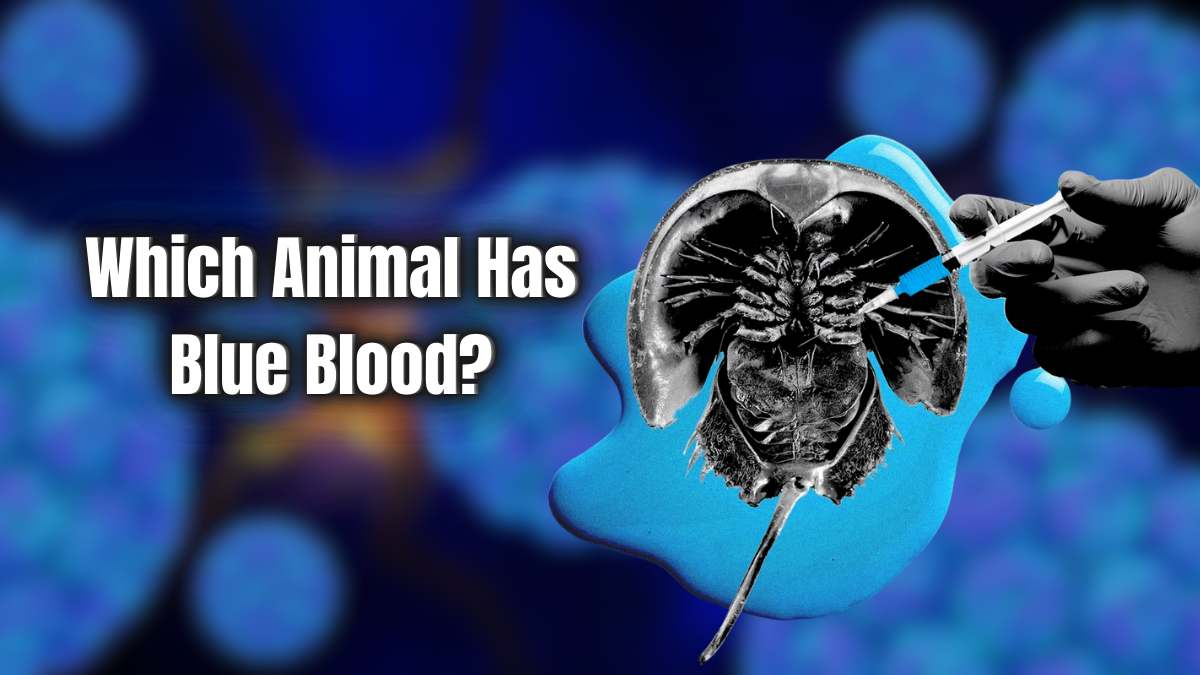

The primary driver of the “blue blood economy” is the horseshoe crab, specifically its unique immune system. Unlike human blood, the blood of the horseshoe crab contains amebocytes—cells that react instantaneously to endotoxins (pathogenic bacteria). This reaction is the basis for the Limulus Amebocyte Lysate (LAL) test, the global gold standard for ensuring that vaccines, injectable drugs, and medical devices are free from contamination.

The Market Valuation of LAL and Hemocyanin

The financial value of horseshoe crab blood is staggering. Estimates place the price of a single gallon of this blue liquid at approximately $60,000, making it one of the most expensive liquids on the planet. This high valuation is driven by its irreplaceable role in the pharmaceutical industry. Every time a new drug is brought to market or a batch of vaccines is produced, it must pass the LAL test.

For investors, this creates a niche but essential market. The companies that hold the licenses to harvest horseshoe crabs and produce LAL reagents—such as Charles River Laboratories, Lonza, and FUJIFILM Wako Chemicals—occupy a protected position in the medical supply chain. The high barrier to entry, consisting of both complex regulatory requirements and specialized harvesting logistics, creates a “moat” around these business models.

Supply Chain Monopolies and Regulatory Protection

The LAL market is a prime example of a regulatory-driven monopoly. Because the U.S. Pharmacopeia (USP) and other international regulatory bodies have historically mandated LAL testing as the primary safety protocol, the demand is inelastic. Regardless of price fluctuations in the broader economy, pharmaceutical companies must purchase these reagents to legally sell their products. This inelasticity provides a stable revenue stream for the firms involved in the extraction and processing of hemocyanin-based products.

The Horseshoe Crab: A Case Study in Specialized Resource Extraction

While octopuses and certain mollusks also possess blue blood, the Atlantic horseshoe crab (Limulus polyphemus) is the true economic engine of this niche. The process of extracting value from these creatures involves a complex logistical dance that sits at the intersection of wildlife management and high-tech manufacturing.

From Shoreline to Lab: The Logistics of Blood Harvesting

The business model relies on a seasonal harvest. Every spring, contractors collect hundreds of thousands of crabs from the Atlantic coast. These crabs are transported to specialized facilities where approximately 30% of their blood is extracted before they are returned to the ocean.

From a business finance perspective, this is a “harvesting” model rather than a “farming” model. This carries unique operational risks. Factors such as climate change, overfishing of the crab’s food sources, and coastal development can impact the “yield” of the season. Companies must manage these ecological variables with the same rigor that a traditional commodity firm manages mining or agricultural yields. The cost of logistics—specialized temperature-controlled transport and sterile laboratory processing—adds significant overhead to the final product price.

Calculating the ROI of Conservation vs. Exploitation

There is an inherent tension in the blue blood economy between short-term extraction and long-term sustainability. If the horseshoe crab population collapses, the billion-dollar safety industry collapses with it. Consequently, we are seeing a shift in how these companies approach “natural capital.”

Investors are increasingly scrutinizing the Environmental, Social, and Governance (ESG) profiles of biotech firms. A company that demonstrates sustainable harvesting practices—ensuring low mortality rates during the bleeding process—is seen as a more stable long-term investment. The “Return on Investment” (ROI) here is not just calculated in dollars per gallon, but in the longevity of the biological resource.

Emerging Markets and Synthetic Disruptors

In every high-value commodity market, high prices eventually invite innovation and disruption. The blue blood market is currently facing its “Tesla moment” with the rise of synthetic alternatives. This shift represents a significant point of interest for venture capital and growth-oriented investors.

Recombinant Factor C (rFC): The Tech-Driven Threat

The primary challenger to the blue blood monopoly is Recombinant Factor C (rFC). This is a synthetically produced version of the horseshoe crab’s clotting enzyme, created through genetic engineering. Because rFC does not require the harvesting of live animals, it offers a more stable, scalable, and ethically palatable supply chain.

From an investment standpoint, the transition to rFC is a classic “disruptive technology” play. Initially, rFC faced skepticism and regulatory hurdles. However, in recent years, major pharmaceutical players like Eli Lilly have begun shifting their testing protocols to synthetic alternatives. For the traditional LAL producers, this represents a major “stranded asset” risk. If the global regulatory bodies fully pivot to rFC, the infrastructure built around crab harvesting could become obsolete overnight.

Investment Risks in the Transition to Lab-Grown Alternatives

The volatility in this sector currently stems from regulatory uncertainty. In 2020 and 2023, the U.S. Pharmacopeia moved toward giving rFC equal standing with LAL, a move that sent ripples through the biotech investment community. Investors must weigh the established cash flows of LAL producers against the high-growth potential of synthetic biotech firms.

The risk profile is binary: if LAL remains the “gold standard,” the traditional players continue their dominance. If rFC is mandated for its sustainability, the market cap will shift toward companies specializing in synthetic protein manufacturing.

Strategic Opportunities for Investors in the Biotech and Life Sciences Sectors

For the sophisticated investor, the “blue blood” narrative serves as a gateway to broader opportunities in the life sciences and specialized bio-commodities. It highlights the importance of identifying critical, “invisible” components within the pharmaceutical supply chain.

Diversifying Portfolios with Specialized Bio-Commodities

Beyond the horseshoe crab, the blue blood of the octopus and the giant keyhole limpet is being investigated for use in cancer treatments and as oxygen carriers in blood substitutes. These are “frontier” investments. While they are currently in the R&D phase, they represent the next wave of biological wealth extraction.

Investors looking for alpha should focus on firms that are not just extracting raw materials, but are holding the intellectual property (IP) for how those materials are used in diagnostic and therapeutic applications. The value is moving from the “raw blood” to the “patented process.”

The ESG Implication of Biological Harvesting

In the current financial climate, the ethical treatment of biological resources is no longer just a PR concern; it is a financial one. Institutional investors are increasingly divesting from companies that rely on unsustainable “blood harvests.”

The transition to synthetic blue blood is a major ESG win. Companies that lead this transition are likely to attract significant capital from “impact investors” and green funds. Therefore, the strategic play is to identify the companies that are cannibalizing their own traditional LAL revenue in favor of synthetic rFC. These are the firms that understand the future of the market and are de-risking their operations against future environmental regulations.

Conclusion: The Future of the Blue Blood Market

The question of “what creatures have blue blood” leads us far beyond a simple biology lesson and into the heart of global medical finance. The horseshoe crab and its blue-blooded kin have provided the foundation for safe medical advancement for decades, creating a high-value, high-barrier market.

However, the intersection of technology and finance is shifting. As synthetic biology matures, the literal “blue blood” economy will likely transition into a “digital blue” economy, where lab-grown proteins replace harvested ones. For investors, the opportunity lies in navigating this transition—balancing the lucrative, reliable returns of traditional biological extraction against the inevitable rise of sustainable, tech-driven alternatives. In the world of “liquid gold,” the most valuable asset is no longer the blood itself, but the innovation that allows us to move beyond it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.