Navigating the landscape of retirement involves more than just selecting the right stocks or ensuring your 401(k) distributions are on track. One of the most significant, yet often misunderstood, variables in a long-term financial plan is healthcare spending. At the heart of this expenditure is the Medicare deductible. While many people view Medicare as a comprehensive safety net, it is functionally a cost-sharing arrangement between the federal government and the beneficiary.

For anyone focused on personal finance and wealth preservation, understanding how these deductibles work is essential. A deductible is the amount you must pay out-of-pocket for covered health care services before your Medicare plan begins to pay. Because these figures change annually and are applied differently across the various “Parts” of Medicare, failing to account for them can lead to significant budgetary friction during your retirement years.

1. The Financial Mechanics of Medicare Deductibles

In the realm of personal finance, a deductible is a form of self-insurance. By agreeing to pay a certain amount upfront, you effectively lower the risk for the insurer—in this case, the Centers for Medicare & Medicaid Services (CMS). However, Medicare is unique because it does not have a single, universal deductible. Instead, it is bifurcated into different sections, each with its own rules, timelines, and financial implications.

The Role of Cost-Sharing in Retirement Budgeting

When building a financial model for retirement, most advisors suggest a “buffer” for healthcare. The Medicare deductible is the first line of expense in that buffer. Unlike a standard PPO or HMO plan you might have had through an employer, Medicare’s deductibles can be triggered multiple times a year depending on the “Part” in question. Understanding this helps in determining how much liquidity you need to maintain in a high-yield savings account or a money market fund to cover immediate medical bills.

Annual Adjustments and Inflationary Pressure

Medicare deductibles are not static; they are adjusted annually based on the cost of healthcare services and the overall economic climate. For a retiree on a fixed income, these incremental increases can act as a “stealth tax” on their savings. Monitoring the yearly updates from the Social Security Administration regarding Medicare premiums and deductibles is a vital part of an annual financial checkup.

2. Breaking Down the Costs: Part A and Part B Deductibles

To master your medical finances, you must distinguish between Part A (Hospital Insurance) and Part B (Medical Insurance). The way these deductibles are structured represents two very different types of financial risk.

Medicare Part A: The “Benefit Period” Trap

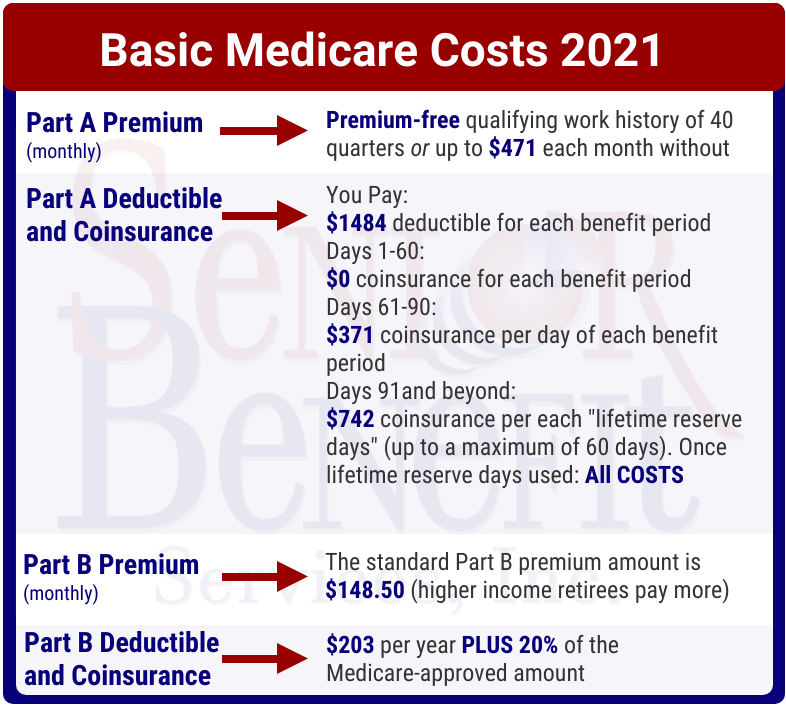

The Part A deductible is perhaps the most misunderstood concept in Medicare finance. As of the current fiscal year, the Part A deductible is significant (often exceeding $1,600). However, it is not an annual deductible. Instead, it applies to each “benefit period.”

A benefit period begins the day you are admitted to a hospital or skilled nursing facility and ends when you have not received any inpatient care for 60 consecutive days. This means if you are hospitalized in January, pay your deductible, and are discharged, but then return to the hospital in August after a 70-day gap, you must pay the deductible again. From a wealth management perspective, this represents a “recurring risk” that requires a more robust emergency fund than a standard one-and-done annual deductible.

Medicare Part B: The Standard Annual Threshold

Part B covers outpatient services, doctor visits, and durable medical equipment. Fortunately, the Part B deductible is much more predictable. It is an annual deductible, meaning you pay it once per calendar year. Once you meet this threshold (which is relatively low compared to Part A, usually in the low hundreds), Medicare typically covers 80% of the approved costs, leaving you with a 20% coinsurance.

For the savvy investor, Part B is easier to automate in a budget. However, the 20% coinsurance that follows the deductible is uncapped. Unlike private insurance, Original Medicare has no “out-of-pocket maximum,” which is a glaring financial vulnerability that must be addressed through secondary insurance or significant cash reserves.

3. The Financial Impact of Medicare Advantage and Part D

For those looking to cap their financial exposure, Medicare Part C (Advantage) and Part D (Prescription Drugs) offer different deductible structures managed by private insurance companies.

Evaluating Medicare Advantage (Part C) Deductibles

Medicare Advantage plans are the “all-in-one” alternative to Original Medicare. These plans often have lower or even $0 deductibles for medical services to attract beneficiaries. However, the trade-off is often found in the network restrictions and copayments.

From a brand and value-comparison perspective, shopping for an Advantage plan is much like shopping for any other financial product. You must weigh the “low deductible” marketing hook against the total cost of ownership, which includes premiums and maximum out-of-pocket limits. If you are someone who utilizes healthcare frequently, a plan with a $0 deductible but high copays might actually be more expensive than a traditional plan.

Navigating the Prescription Drug (Part D) “Donut Hole”

Part D plans also have deductibles, which are capped by federal law but vary by plan. The financial complexity here lies in the “initial coverage limit” and the “coverage gap,” historically known as the donut hole. While recent legislation is working to close this gap and cap out-of-pocket drug costs, the deductible remains the first hurdle. For retirees on expensive maintenance medications, the Part D deductible is a guaranteed January expense that should be factored into year-end tax and cash-flow planning.

4. Strategic Financial Planning: Managing Out-of-Pocket Risks

Once you understand what the deductibles are, the next step is implementing strategies to mitigate their impact on your net worth. Healthcare is often the largest “wild card” in a financial plan, but it can be tamed with the right tools.

Leveraging Health Savings Accounts (HSAs)

If you are still in your working years and have a High Deductible Health Plan (HDHP), the HSA is your greatest financial ally. The HSA offers a triple tax advantage: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses—including Medicare deductibles—are tax-free.

Strategic investors use the “shoebox method”: paying for medical expenses out-of-pocket now, letting the HSA grow in aggressive equity investments, and then reimbursing themselves tax-free during retirement to cover Medicare Part A and B deductibles. This turns a medical necessity into a powerful wealth-generation engine.

Medigap: Insuring the Insurance

To eliminate the unpredictability of the Part A and Part B deductibles, many retirees opt for Medicare Supplement Insurance, or “Medigap.” These policies are sold by private companies and are designed to pay for the “gaps” in Original Medicare.

Specifically, certain Medigap plans (like Plan G) cover 100% of the Part A deductible. While this requires a monthly premium, it converts a variable, high-risk expense (the hospital deductible) into a fixed, predictable line item in your monthly budget. For those who value “peace of mind” and certain cash flows, paying the premium to avoid the deductible is often a wise fiscal move.

Tax-Loss Harvesting and Medical Deductions

In years where medical expenses—including deductibles—exceed 7.5% of your Adjusted Gross Income (AGI), they may become tax-deductible if you itemize. This creates a unique opportunity for “financial rebalancing.” If you know you will hit a high deductible threshold due to a scheduled surgery, it might be the right time to realize capital gains or take a larger IRA distribution, as the medical deduction can help offset the tax liability.

5. Conclusion: Deductibles as a Component of Capital Allocation

Viewing a Medicare deductible simply as a “bill” is a narrow perspective. In the broader context of personal finance, it is a component of capital allocation. Every dollar spent on a deductible is a dollar that isn’t invested in the market or spent on lifestyle.

To master your retirement finances, you must:

- Anticipate the Part A Benefit Period: Don’t assume one deductible covers you for the year.

- Budget for the Part B Annual Hit: Treat it as a “sunk cost” in your January cash-flow analysis.

- Hedge with Supplement Plans: Evaluate if the premium of a Medigap plan provides a better “Return on Risk” than self-insuring the deductibles.

- Maximize Pre-Retirement Tools: Use HSAs to build a dedicated “Medicare Deductible Fund.”

By understanding the nuances of how and when Medicare deductibles are applied, you can move from a reactive financial posture to a proactive one. Healthcare costs do not have to be a threat to your legacy; with proper planning, they are simply another manageable variable in a well-constructed financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.