Understanding your credit score is fundamental to navigating the financial landscape. It’s not merely an abstract number; it’s a powerful indicator that lenders use to assess your creditworthiness, your reliability in repaying borrowed money. While a high score opens doors to favorable loan terms, lower scores can present significant obstacles, impacting your ability to secure mortgages, car loans, and even rent an apartment. This article delves into the nuances of what constitutes a “bad” credit score, exploring the factors that influence it, the consequences of having one, and strategies for improvement, all within the realm of personal finance.

Defining the Credit Score Spectrum

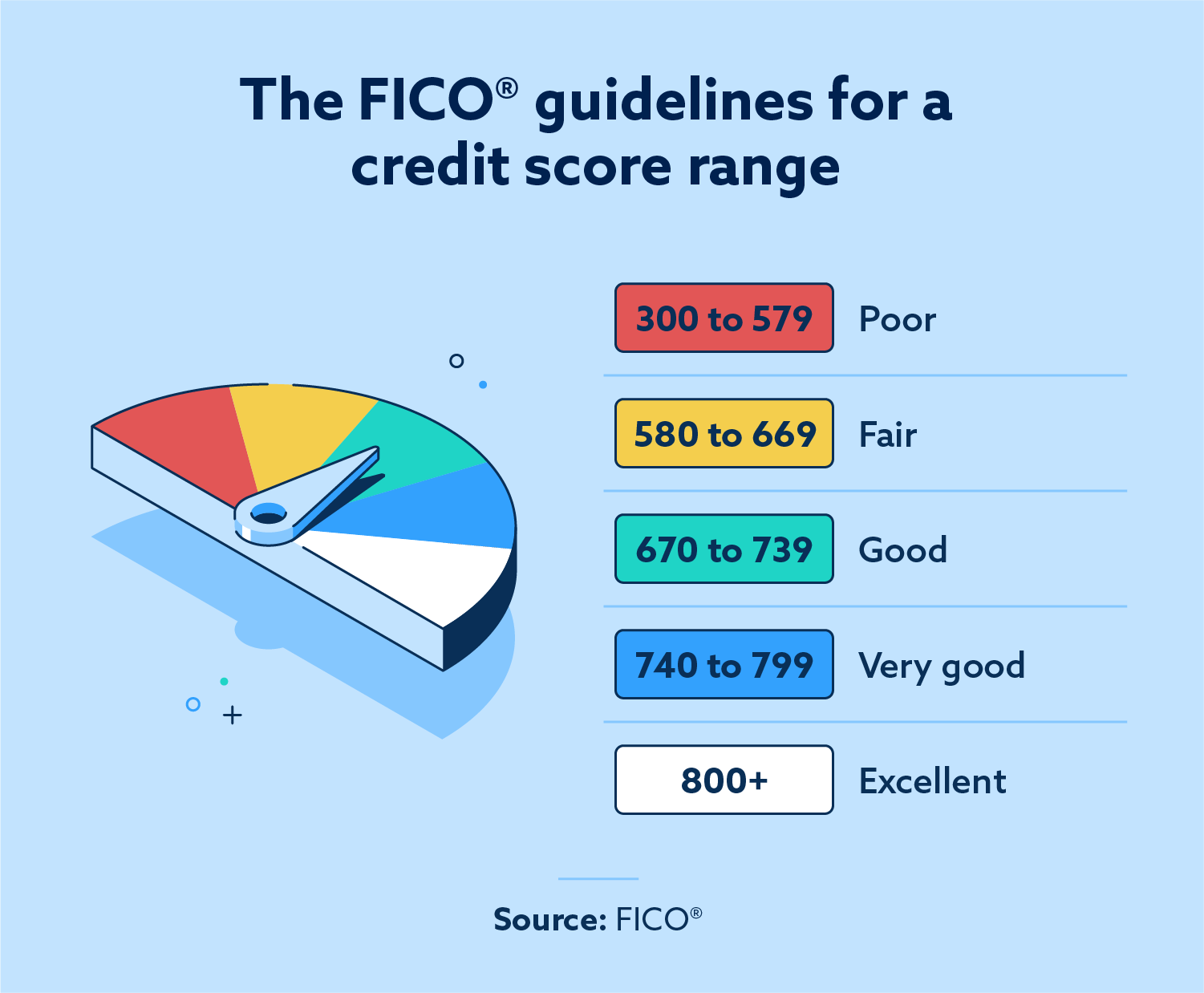

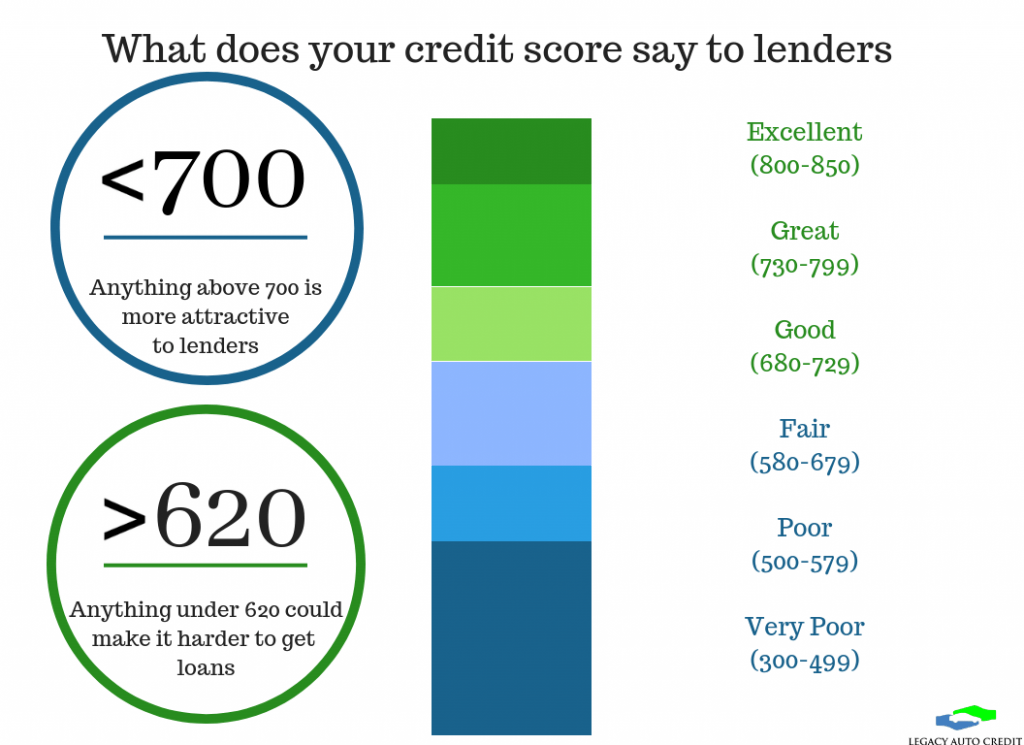

Credit scores are typically generated using complex algorithms developed by credit bureaus like Equifax, Experian, and TransUnion. The most widely used scoring model is FICO, with its scores generally ranging from 300 to 850. Within this range, different segments are recognized, each carrying distinct implications.

The FICO Score Ranges and Their Meanings

The FICO scoring system provides a standardized way to interpret creditworthiness. While the exact cutoffs can vary slightly and lenders may have their own internal thresholds, a general understanding of these ranges is crucial:

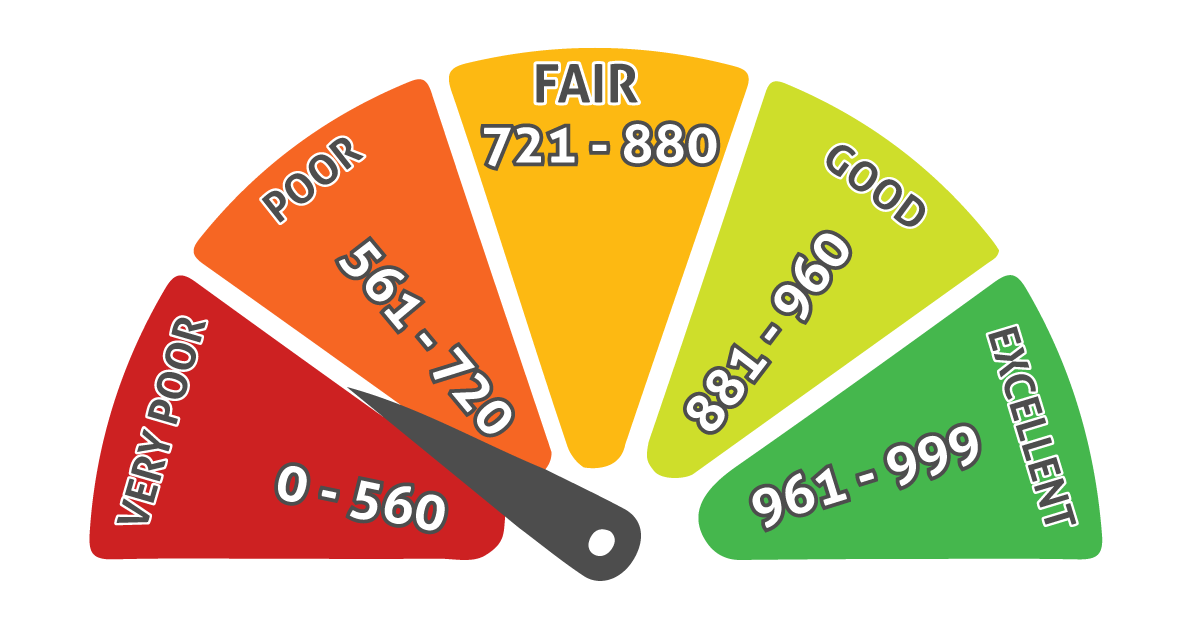

- Exceptional Credit (800-850): This is the pinnacle of creditworthiness. Individuals in this range are seen as extremely low-risk borrowers, typically qualifying for the best interest rates and loan terms available.

- Very Good Credit (740-799): Also highly desirable, this range indicates a strong history of responsible credit management. Borrowers here will likely receive competitive offers.

- Good Credit (670-739): This is often considered the benchmark for approval on most standard loans and credit cards. While not exceptional, it signifies a generally reliable borrower.

- Fair Credit (580-669): This is where the “bad” credit territory begins to emerge. While some lenders may still approve applications, interest rates will likely be higher, and loan amounts might be limited. This range often signals a need for improvement in credit habits.

- Poor Credit (300-579): This range definitively classifies a borrower as high-risk. Obtaining credit becomes significantly more challenging, and when approved, it often comes with very high interest rates, substantial fees, and strict repayment terms. This is the zone most people associate with a “bad” credit score.

It’s important to note that these are general guidelines. Some lenders might consider scores below 700 to be “fair” or even “bad,” especially for specific types of loans like mortgages where the risk tolerance can be lower. Conversely, some subprime lenders might work with scores in the lower ranges, but at a considerable financial cost to the borrower.

Why a Low Score Matters: Beyond Loan Applications

The impact of a poor credit score extends far beyond just loan applications. In today’s interconnected financial world, your credit history is a powerful data point used in various aspects of your life.

- Rental Applications: Landlords increasingly check credit scores to gauge a prospective tenant’s reliability in paying rent on time. A low score can lead to outright rejection or a requirement for a larger security deposit or a co-signer.

- Insurance Premiums: In many states, insurance companies, including those for auto and homeowners insurance, use credit-based insurance scores. Studies have shown a correlation between credit behavior and the likelihood of filing claims, leading to higher premiums for individuals with lower credit scores.

- Employment Opportunities: Certain employers, particularly those in positions involving financial responsibility or access to sensitive information, may review credit reports as part of their background checks. A history of financial mismanagement could be seen as a red flag.

- Utility Services: Utility companies (electricity, gas, water, and sometimes even cell phone providers) may require a security deposit from individuals with low credit scores to mitigate the risk of non-payment.

- Negotiating Power: A strong credit score gives you leverage. You can shop around for the best rates and terms. A bad score significantly diminishes this negotiating power, often leaving you with limited, less favorable options.

Factors Contributing to a Bad Credit Score

Understanding the components that make up your credit score is the first step toward improving it. Credit bureaus analyze your financial behavior over time, and certain actions or inactions can significantly damage your score.

Payment History: The Cornerstone of Credit

By far the most influential factor in your credit score is your payment history. This reflects how consistently you pay your bills on time.

- Late Payments: Even a single 30-day late payment can negatively impact your score. The severity of the impact increases with the number of days the payment is overdue (e.g., 60 days, 90 days, or more). Multiple late payments, especially recent ones, are a strong indicator of risk.

- Defaults and Collections: If you fail to make payments for an extended period, your account may be “charged off” by the lender and sent to a collection agency. This is a severe negative mark on your credit report and can remain for up to seven years.

- Bankruptcy: Filing for bankruptcy is one of the most damaging events to a credit score. It signifies a significant inability to repay debts and can remain on your credit report for seven to ten years, depending on the type of bankruptcy.

Credit Utilization: The Balancing Act of Borrowing

Credit utilization refers to the amount of credit you’re using compared to your total available credit. Keeping this ratio low is crucial for a healthy score.

- High Balances: Maxing out credit cards or carrying high balances relative to your credit limits significantly harms your score. This suggests you might be overextended and reliant on credit to manage your finances.

- General Rule of Thumb: Experts generally recommend keeping your credit utilization ratio below 30% for each card and overall. The lower, the better. For instance, if you have a credit card with a $10,000 limit, keeping the balance below $3,000 would be ideal.

Length of Credit History: Time as a Factor

The longer you’ve had credit accounts in good standing, the better it generally is for your score. This demonstrates a consistent history of responsible borrowing.

- Older Accounts: Well-managed, older credit accounts can bolster your score because they provide a longer track record for lenders to assess.

- Closing Old Accounts: While it might seem counterintuitive, closing older, positive credit accounts can sometimes hurt your score, especially if they have zero balances. This can reduce your overall available credit, potentially increasing your utilization ratio, and shorten your average account age.

Credit Mix and New Credit: Diversification and Prudence

While payment history and utilization are paramount, other factors also play a role.

- Credit Mix: Having a mix of different types of credit, such as credit cards, installment loans (like mortgages or car loans), and student loans, can be beneficial. It shows you can manage various forms of debt responsibly. However, this factor is less impactful than the others.

- New Credit and Inquiries: Frequently opening new credit accounts in a short period can negatively affect your score. Each application for credit typically results in a “hard inquiry” on your credit report, which can slightly lower your score. Multiple inquiries suggest you might be in financial distress or taking on too much debt too quickly.

The Ripple Effect: Consequences of a Bad Credit Score

The implications of a bad credit score are multifaceted and can create a cycle that’s challenging to break without proactive effort.

Higher Borrowing Costs: The Price of Risk

When lenders deem you a high-risk borrower, they compensate for that risk by charging higher interest rates.

- Mortgage Loans: A lower credit score can mean significantly higher monthly mortgage payments over the life of the loan. For a substantial loan amount, this can translate into tens or even hundreds of thousands of dollars in extra interest paid.

- Auto Loans: Similar to mortgages, bad credit will result in higher interest rates on car loans, making vehicle purchases more expensive.

- Credit Cards: You’ll likely be offered credit cards with lower credit limits and much higher annual percentage rates (APRs). These cards may also come with substantial annual fees.

Limited Access to Credit: The “No” List

Beyond just higher costs, a bad credit score can simply prevent you from accessing certain types of credit altogether.

- Subprime Lenders: While some lenders specialize in working with borrowers with poor credit, their terms are often exceptionally unfavorable, making them a last resort.

- Credit Card Denials: Many standard credit card applications will be automatically denied for individuals with scores in the “fair” or “poor” categories.

Increased Fees and Deposits: The Cost of Initial Trust

As mentioned earlier, the impact of bad credit extends to non-loan related financial interactions.

- Security Deposits: Expect to pay larger security deposits for rental properties, utilities, and even some cell phone plans. These deposits are essentially a buffer for the service provider against your potential non-payment.

- Insurance Premiums: Higher insurance premiums can add a significant ongoing cost to your budget, even if you’ve never filed a claim.

Psychological and Lifestyle Impact: The Stress of Financial Constraints

Beyond the tangible financial costs, living with a bad credit score can impose significant psychological stress and limit lifestyle choices. The constant worry about not qualifying for a loan, the rejection from landlords, and the higher costs can be emotionally taxing. It can limit your ability to make significant life changes, such as buying a home, purchasing a reliable vehicle, or even securing a better apartment.

Strategies for Improving a Bad Credit Score

The good news is that a bad credit score is not a permanent sentence. With consistent effort and smart financial habits, it is possible to rebuild your creditworthiness over time.

Prioritize On-Time Payments: The Foundation of Repair

This cannot be overstated: paying all your bills on time, every time, is the single most critical step in improving your credit score.

- Set Up Auto-Pay: For recurring bills like rent, utilities, and loan payments, set up automatic payments from your bank account to avoid missing due dates. Ensure you have sufficient funds in your account to cover these payments.

- Payment Reminders: Utilize calendar alerts, phone reminders, or budgeting apps to keep track of upcoming due dates for all your financial obligations.

- Communicate with Lenders: If you anticipate a problem making a payment, contact your lender before the due date. They may be willing to work with you on a payment plan or offer a temporary solution to avoid a delinquency.

Reduce Credit Card Balances: Tackle High Utilization

Lowering your credit utilization ratio is another high-impact strategy.

- Pay Down Balances Aggressively: Focus on paying down the balances on your credit cards, especially those with the highest utilization. Aim to get each card’s balance below 30% of its limit.

- Avoid New Spending: While you’re working on paying down balances, try to refrain from making new purchases on credit cards until your utilization is in a healthier range.

- Consider Balance Transfers (with Caution): If you have high-interest credit card debt, a balance transfer to a card with a 0% introductory APR can save you money on interest. However, be mindful of transfer fees and ensure you can pay off the balance before the introductory period ends.

Be Patient and Monitor Your Progress: The Long Game

Credit repair is a marathon, not a sprint. It takes time for positive changes to reflect on your credit report and for your score to improve significantly.

- Obtain Your Credit Reports: Regularly obtain your free credit reports from each of the three major bureaus (Equifax, Experian, TransUnion) at AnnualCreditReport.com. Review them for accuracy and dispute any errors.

- Credit Monitoring Services: Consider using credit monitoring services that can alert you to changes in your credit report and score, helping you stay on track.

- Build Positive Credit: If you struggle to get approved for traditional credit, consider secured credit cards or credit-builder loans. These are designed to help individuals with no or poor credit history establish a positive track record. You deposit funds upfront, which then becomes your credit limit or loan amount, and responsible repayment builds your credit.

In conclusion, understanding what constitutes a bad credit score is crucial for financial well-being. It’s a score that signals risk to lenders and can lead to higher costs and limited access to credit across various aspects of your life. By understanding the factors that influence your score, recognizing the consequences of a low score, and diligently implementing strategies for improvement, you can gradually rebuild your credit and unlock more favorable financial opportunities. The journey may require patience and discipline, but the rewards of a strong credit score are substantial and long-lasting.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.