The term “HUD statement” can evoke a sense of mystery and complexity, often encountered during the often overwhelming process of buying or selling a home. For those navigating the real estate landscape, understanding this crucial document is not just beneficial; it’s essential. A HUD statement, officially known as the Real Estate Settlement Procedures Act (RESPA) Integrated Disclosure (ID) form, or more commonly, the Closing Disclosure (CD), is a standardized form designed to provide consumers with clear and understandable information about the costs and terms of their mortgage loan. It serves as a vital tool for transparency, ensuring that buyers and sellers are fully aware of all the financial aspects of their real estate transaction before closing. This article will delve into what a HUD statement looks like, breaking down its key components and explaining their significance within the context of personal finance.

The evolution of the HUD statement is rooted in a desire for greater consumer protection. Historically, settlement statements were often complex and varied, making it difficult for borrowers to compare loan offers and understand the true cost of their mortgage. Recognizing this, regulatory bodies mandated standardized forms to simplify the process and prevent predatory lending practices. While the term “HUD statement” is still widely used, the current iteration is the Closing Disclosure (CD), implemented by the Consumer Financial Protection Bureau (CFPB) as part of the TCF (TILA-RESPA Integrated Disclosure) rule. This transition aimed to further enhance clarity and provide borrowers with more time to review their loan terms before committing to a closing. Understanding the CD is paramount to making informed financial decisions in real estate.

Understanding the Purpose and Structure of the Closing Disclosure

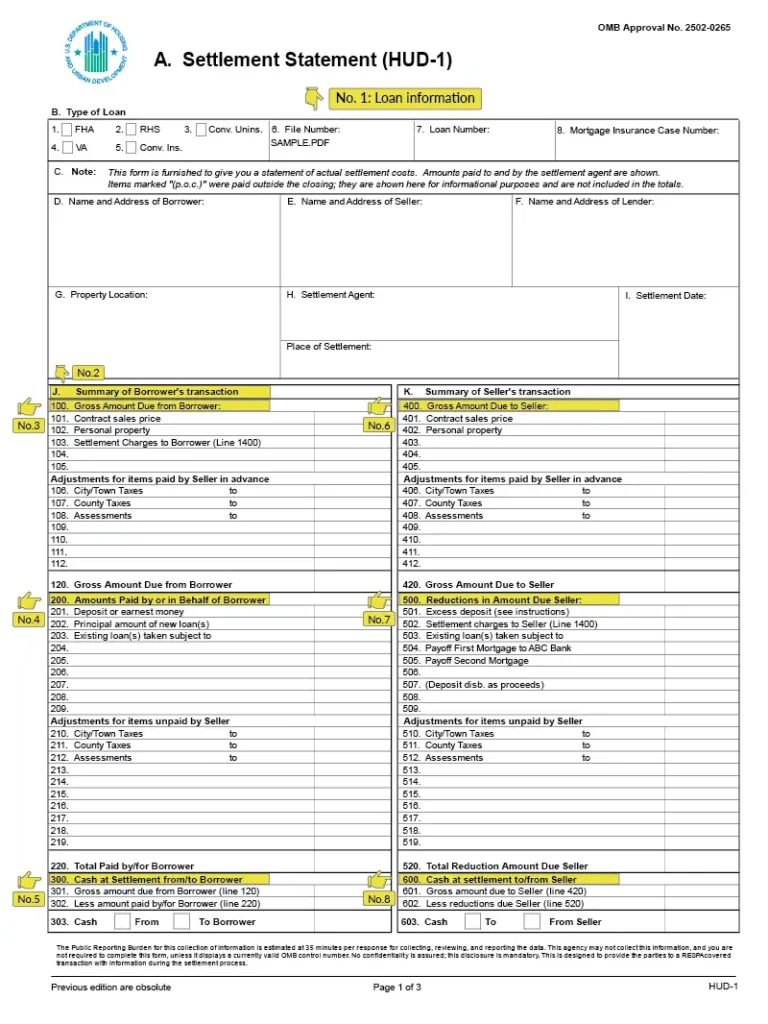

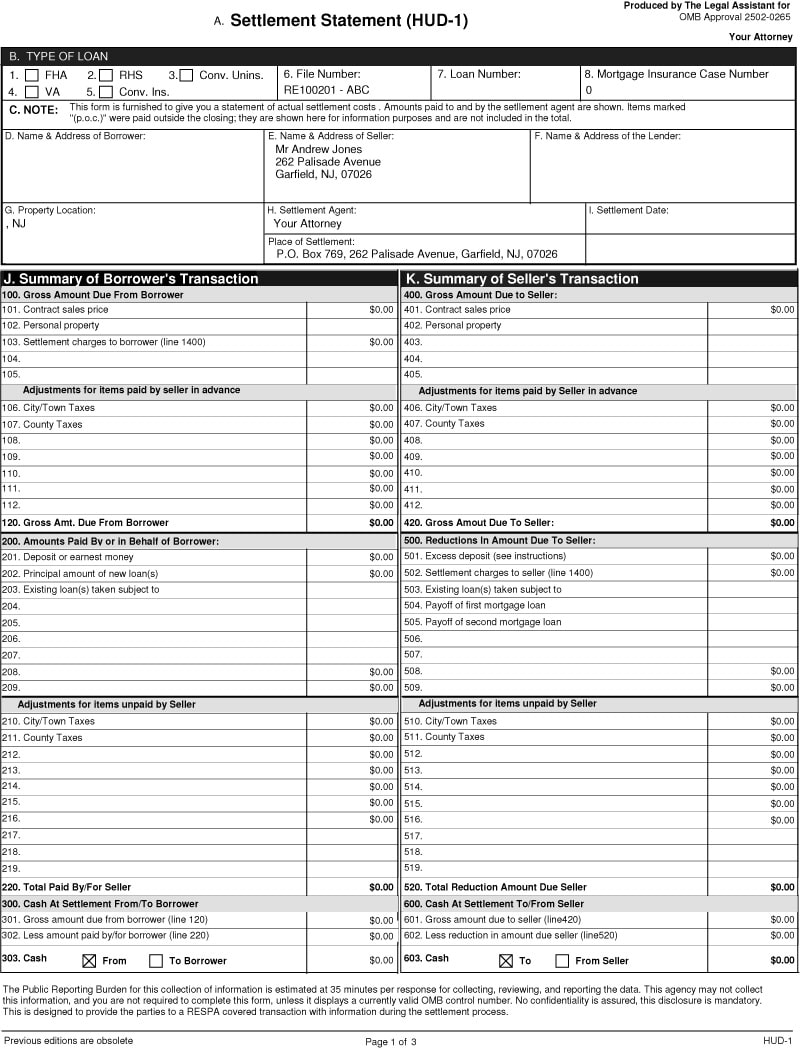

The primary purpose of the Closing Disclosure (CD), often referred to as the HUD statement, is to consolidate all the financial details of a real estate transaction into a single, easy-to-understand document. It replaces two older forms, the HUD-1 Settlement Statement and the Truth-in-Lending disclosure, creating a more integrated and transparent system. The CD is designed to be provided to the borrower at least three business days before the scheduled closing, allowing ample time for review and comparison with the Loan Estimate (LE) that was provided when the loan was applied for. This “three-day rule” is a cornerstone of consumer protection, giving borrowers a critical window to identify any discrepancies or unexpected charges.

The structure of the Closing Disclosure is meticulously organized into several key sections, each addressing a specific aspect of the transaction. This structured approach ensures that all relevant information is presented logically and systematically. By familiarizing oneself with these sections, borrowers can effectively decipher the financial landscape of their mortgage. The document is divided into pages, with the first page providing an overview of the loan and its terms, followed by subsequent pages detailing various costs and credits. The layout is designed to be user-friendly, with clear headings, concise explanations, and a consistent format across all lenders.

Loan Terms and Personal Financial Details

The initial pages of the Closing Disclosure are dedicated to outlining the fundamental terms of the mortgage loan and the personal financial information of the borrower. This section provides a high-level overview of the loan itself, giving borrowers a quick reference to key figures that will impact their long-term financial commitments. It’s crucial to review this section carefully to ensure that the loan details presented align with what was agreed upon during the application process.

Loan Summary and Interest Rate

This subsection details the principal loan amount, the interest rate, and the estimated monthly principal and interest (P&I) payment. It will also specify whether the interest rate is fixed or adjustable, and if adjustable, it will outline the initial adjustment period and any caps on rate increases. Understanding the interest rate is fundamental to calculating the total cost of the loan over its lifetime. A seemingly small difference in interest rate can translate into thousands of dollars over the life of a 30-year mortgage. Borrowers should verify that the stated interest rate matches their approved loan offer.

Estimated Monthly Payment Breakdown

Beyond the P&I, this section breaks down the estimated total monthly payment, which typically includes not only P&I but also escrows for property taxes and homeowner’s insurance. Some loans may also include private mortgage insurance (PMI) or Homeowner’s Association (HOA) dues. Accurately understanding this breakdown is vital for budgeting purposes. Unexpected increases in the monthly payment can strain personal finances, so it’s important to ensure these figures are realistic and align with expectations.

Loan Costs and Lender Credits

This part of the loan terms section will detail any lender credits offered, which can be used to offset closing costs. Conversely, it will also highlight any origination fees or other charges the lender directly imposes. Comparing these figures against the Loan Estimate is a critical step. Significant deviations can signal a need for further clarification from the lender.

Transaction Overview and Settlement Charges

The subsequent pages of the Closing Disclosure focus on the specifics of the real estate transaction itself and itemize all the settlement charges. This is where the myriad of costs associated with buying or selling a property are laid bare. This section is often the most detailed and requires careful scrutiny.

Cash to Close Calculation

This is arguably the most critical part of the Closing Disclosure for the buyer. It clearly states the total amount of money the buyer needs to bring to the closing table. This figure is derived by subtracting various credits and the loan amount from the total sale price and adding all the associated closing costs and prepaid items. Any adjustments or discrepancies here must be addressed before closing. It’s crucial to reconcile this figure with the buyer’s personal financial resources.

Itemized List of Settlement Charges

This comprehensive list details every fee and charge associated with the real estate transaction. It’s divided into several categories, making it easier to understand where the money is going. This includes:

- Origination Charges: Fees charged by the lender for processing the loan, such as application fees, underwriting fees, and discount points.

- Services You Cannot Shop For: Fees for services where the borrower does not have a choice of provider, such as appraisal fees, credit report fees, and flood determination fees.

- Services You Can Shop For: Fees for services where the borrower can choose their own provider, such as title insurance, escrow services, and attorney fees. Lenders must provide a list of providers they recommend, but borrowers are not obligated to use them.

- Prepaid Items: Costs that are paid in advance, such as homeowner’s insurance premiums, property taxes, and prepaid per diem interest. These are often prorated based on the closing date.

- Initial Escrow Payment: The amount deposited into an escrow account at closing to cover future property taxes and homeowner’s insurance.

The buyer has the right to shop for providers for services in the “Services You Can Shop For” category. Comparing quotes from different providers can lead to significant savings. This section also highlights any potential areas for negotiation or cost reduction.

Final Loan Costs vs. Loan Estimate

A crucial aspect of the Closing Disclosure is its comparison to the Loan Estimate. The CFPB mandates that certain closing costs on the CD cannot increase from the LE by more than a specified tolerance. The CD will clearly indicate whether the final figures have changed from the LE and by how much. Any significant increases in these categories will prompt a re-issuance of the CD and an extension of the three-day review period, providing further protection. Understanding these tolerance levels is vital for detecting any unwarranted cost hikes.

The Significance of the HUD Statement in Personal Finance

The HUD statement, in its current form as the Closing Disclosure, plays a pivotal role in managing personal finances, particularly for major life events like purchasing a home. It demystifies the complex financial landscape of a real estate transaction, empowering individuals to make informed decisions and avoid costly mistakes. Its transparent presentation of costs and loan terms allows for better financial planning and budgeting.

Budgeting and Long-Term Financial Planning

By providing a clear breakdown of monthly payments, including P&I, taxes, insurance, and potentially PMI or HOA dues, the CD enables borrowers to accurately forecast their ongoing housing expenses. This information is critical for creating a realistic budget and ensuring that the mortgage payment is sustainable within the borrower’s overall financial picture. Furthermore, understanding the total cost of the loan, including interest paid over its term, allows for more effective long-term financial planning, such as retirement savings or other investment strategies. Knowing the precise figures helps in making informed decisions about how much house one can truly afford.

Identifying Potential Red Flags and Discrepancies

The detailed itemization of all settlement charges on the CD is an invaluable tool for detecting any unexpected or questionable fees. By comparing the CD to the initial Loan Estimate, borrowers can identify any unauthorized increases or new charges that were not previously discussed. This level of scrutiny is crucial for preventing predatory lending practices and ensuring that the borrower is not being overcharged. A thorough review of the CD can reveal discrepancies that might otherwise go unnoticed, saving the borrower significant amounts of money and stress.

Making Informed Decisions About Mortgage Options

The clarity of the Closing Disclosure allows borrowers to better understand the nuances of their mortgage. By examining the interest rate, loan term, and any associated fees, individuals can make more informed decisions about whether the chosen mortgage product is the best fit for their financial goals. For instance, understanding the impact of discount points on the interest rate can help determine if paying points upfront is financially advantageous over the life of the loan. In essence, the CD empowers individuals to be active participants in their financial journey, rather than passive recipients of loan terms.

Navigating the Closing Disclosure Effectively

Successfully navigating the Closing Disclosure requires a proactive and meticulous approach. It’s not a document to be signed blindly. Armed with a clear understanding of its components and purpose, individuals can approach the closing process with confidence.

The Importance of Reviewing the Loan Estimate First

Before even receiving the Closing Disclosure, it’s imperative to thoroughly review the Loan Estimate (LE). The LE provides an initial estimate of the loan terms and closing costs. Understanding the LE serves as a baseline for comparison. Any significant deviations on the Closing Disclosure should be immediately questioned and clarified. This preliminary review sets the stage for a more effective examination of the final document.

Asking Questions and Seeking Clarification

No one should hesitate to ask questions if any part of the Closing Disclosure is unclear. Lenders are required to provide explanations. It’s better to ask numerous questions during the review period than to discover an issue after the closing. This might involve consulting with the mortgage lender, a real estate agent, or a real estate attorney to ensure complete understanding of all the financial implications.

The Three-Day Review Period: A Critical Window

The mandatory three-day review period before closing is a non-negotiable consumer protection. This time should be utilized to meticulously examine every detail of the Closing Disclosure. It’s advisable to compare it side-by-side with the Loan Estimate, paying close attention to any changes in figures, fees, or terms. This period is your opportunity to catch errors or unexpected changes that could impact your financial well-being.

In conclusion, the HUD statement, now in the form of the Closing Disclosure, is a cornerstone of transparency in real estate transactions. It provides a comprehensive and standardized overview of all financial aspects of a mortgage loan and settlement process. By understanding its structure, purpose, and the significance of each section, individuals can approach their home purchase or sale with greater confidence, ensuring they are making sound financial decisions that align with their long-term personal finance goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.