For the average individual, a vehicle represents one of the most significant financial outlays of their lifetime, second only to real estate. However, unlike a home, which typically appreciates over time, a vehicle is a depreciating asset. Understanding the precise value of your vehicle is not merely a matter of curiosity; it is a critical component of personal finance management. Whether you are looking to trade in for a newer model, sell privately to boost your investment portfolio, or simply assess your net worth, knowing “what my vehicle is worth” requires a deep dive into market dynamics, asset management, and financial timing.

Understanding Your Vehicle as a Financial Asset

To manage your finances effectively, you must stop viewing your car as just a mode of transportation and start viewing it as a fluctuating line item on your balance sheet. The moment a new car is driven off the lot, it undergoes a sharp valuation adjustment, often losing 10% to 20% of its value immediately.

The Reality of Depreciation

Depreciation is the largest hidden cost of vehicle ownership. In the world of personal finance, understanding the rate at which your specific make and model loses value is essential. Most vehicles lose approximately 60% of their original value within the first five years. However, this rate is not uniform. Factors such as brand reputation for reliability, fuel efficiency, and technological longevity play significant roles. For instance, certain trucks and SUVs tend to hold their value better than luxury sedans, which often see a steeper decline due to high maintenance costs and rapid tech obsolescence.

Equity vs. Debt: Where Do You Stand?

A crucial part of determining your vehicle’s worth is calculating your equity. If you have an outstanding auto loan, your vehicle’s value must be measured against your remaining balance. “Positive equity” occurs when the vehicle is worth more than the loan, providing you with a financial cushion or a down payment for your next purchase. Conversely, “negative equity”—often referred to as being “underwater”—occurs when you owe more than the car’s market value. Monitoring your vehicle’s worth allows you to make strategic decisions, such as making extra principal payments to move into a positive equity position before you decide to sell.

Key Factors That Influence Market Value

Valuation is not a static number; it is a reflection of a complex interplay between the condition of the individual asset and the broader economic landscape. To get an accurate figure, you must look beyond the odometer.

Mileage and Mechanical Condition

In the secondary market, mileage is often used as a proxy for the remaining life of the asset. High mileage typically signals a higher probability of impending mechanical failure, which translates to a lower valuation. However, a well-documented service history can mitigate some of the “mileage penalty.” From a financial perspective, a car with 100,000 miles and a meticulous maintenance record may be worth more than a 70,000-mile car with neglected oil changes and worn brakes. Buyers—both private and professional—are willing to pay a premium for “peace of mind.”

Market Demand and Seasonality

Macroeconomic trends significantly impact vehicle worth. For example, during periods of high inflation or supply chain disruptions, the value of used vehicles can skyrocket due to a lack of new inventory. Additionally, seasonality plays a role; a convertible will command a higher price in the spring than in the dead of winter, while a four-wheel-drive SUV might see a valuation bump as the first snow approach. Understanding these cycles allows you to time your sale to maximize your financial return.

History Reports and Documentation

In the age of information, transparency is currency. A vehicle with a “clean” title and a history report (such as Carfax or AutoCheck) free of accidents or flood damage will always command a higher market price. From a business finance perspective, the documentation acts as a “due diligence” packet. Keeping every receipt for repairs and upgrades creates a paper trail that proves the asset has been cared for, allowing you to justify a higher asking price during negotiations.

Professional Valuation Tools and Methods

To answer the question of what your vehicle is worth, you must utilize the same tools that financial institutions and dealerships use. Relying on “gut feeling” or what a neighbor sold their car for is a recipe for financial loss.

Leveraging Digital Valuation Platforms

There are several industry-standard tools designed to provide a baseline for your vehicle’s value.

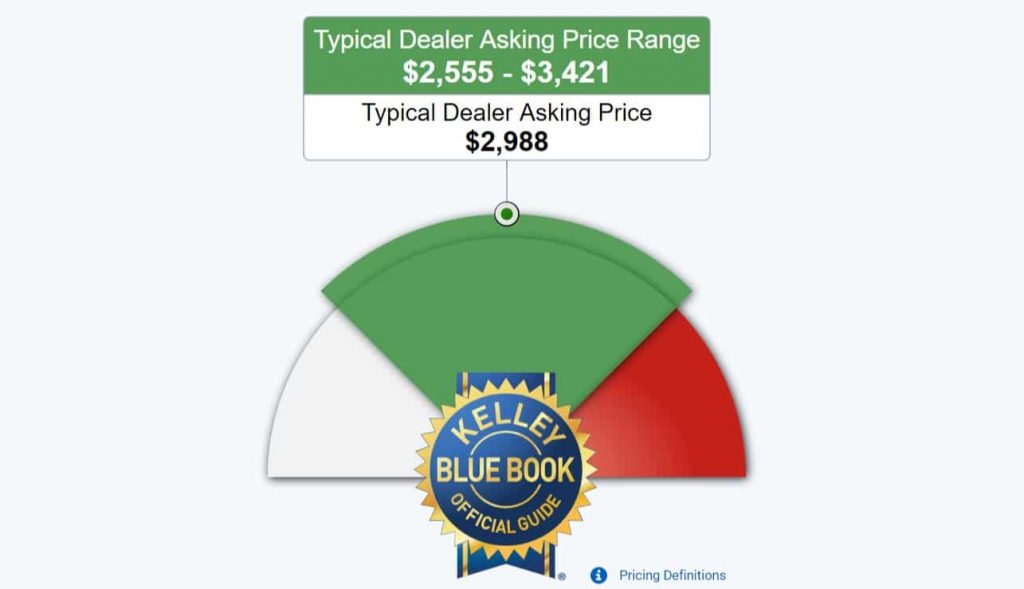

- Kelley Blue Book (KBB): Perhaps the most recognized name, KBB offers a range of values based on condition.

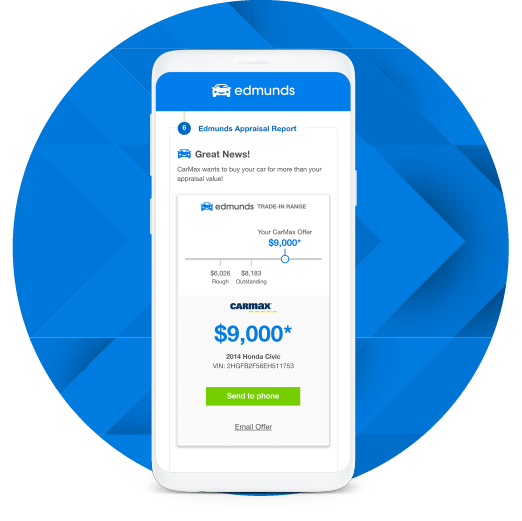

- Edmunds: Known for its “True Market Value” (TMV) pricing, which factors in what others are actually paying in your specific geographic area.

- NADAguides: Often used by lenders and insurance companies, this tool provides a more data-driven approach based on actual transaction prices.

By cross-referencing these platforms, you can find a “sweet spot” valuation that reflects the current reality of the market.

The Difference Between Private Party, Trade-In, and Retail Value

It is vital to understand that your vehicle does not have one single price, but rather three distinct values:

- Trade-In Value: This is what a dealer will give you. It is typically the lowest of the three because the dealer must factor in reconditioning costs and their own profit margin.

- Private Party Value: This is what you can expect to receive if you sell the car yourself to another individual. This is usually higher than trade-in value but requires more effort and marketing.

- Retail Value: This is the price a dealer would list the car for on their lot. While you will rarely get this price as a seller, knowing it helps you understand the ceiling of the market.

Strategies to Increase Your Vehicle’s Resale Value

Just as a homeowner might renovate a kitchen to increase property value, a vehicle owner can take specific steps to enhance the worth of their automotive asset before a sale.

Cost-Effective Maintenance and Detailing

First impressions have a direct financial impact. A professional “deep clean” or detailing service can cost a few hundred dollars but can add a thousand dollars or more to the perceived value of the vehicle. Addressing minor cosmetic issues, such as small dents (via paintless dent repair) or foggy headlights, can yield a high return on investment (ROI). Mechanically, ensuring all fluids are topped off and the tires have adequate tread can prevent a potential buyer from “nickel and diming” you during the negotiation process.

Timing Your Exit from the Asset

One of the most important aspects of personal finance is knowing when to liquidate an asset. Holding onto a vehicle for too long can lead to a “cliff” in value—usually around the 100,000-mile mark or when a major manufacturer warranty expires. By tracking your vehicle’s worth annually, you can identify the optimal moment to sell—the point where you have enjoyed the utility of the vehicle, but before the cost of repairs and the acceleration of depreciation erode your remaining equity.

Navigating the Sale: Turning Value into Liquidity

Once you have determined what your vehicle is worth and have prepared it for the market, the final step is the transaction itself. This is where your research pays off.

Private Sale vs. Dealership Buyouts

If your primary goal is to maximize the cash in your pocket, a private sale is almost always the superior financial choice. However, it comes with the “cost” of time—taking photos, listing the car, and meeting potential buyers. On the other hand, many modern online retailers (like Carvana or Vroom) and traditional dealerships offer “instant cash offers.” While these may be slightly lower than a private sale, the speed and elimination of risk can be seen as a financial benefit in terms of opportunity cost.

Tax Implications and Financial Planning

In many jurisdictions, selling a vehicle and immediately buying another can offer tax advantages. For instance, if you trade in a vehicle, you may only be required to pay sales tax on the difference between the new car’s price and your trade-in value. This “tax credit” can sometimes bridge the gap between a low trade-in offer and a higher private sale price. Always consult with a financial advisor or tax professional to ensure you are capturing all possible savings during the transaction.

Conclusion

Determining “what is my vehicle worth” is the first step in a broader strategy of sound financial management. By understanding depreciation, monitoring market trends, and utilizing professional valuation tools, you transform a simple car into a managed asset. Whether you are looking to reinvest the proceeds into a new venture or simply want to ensure you aren’t leaving money on the table at the dealership, a disciplined approach to vehicle valuation is an essential skill in the modern economy. Your vehicle is a significant piece of your financial puzzle; treat its valuation with the precision and attention it deserves.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.