The global financial landscape is currently undergoing its most significant transformation since the invention of double-entry bookkeeping. For decades, the concept of money was tethered to centralized institutions—banks, governments, and clearinghouses. However, the emergence of cryptocurrency has introduced a paradigm shift, redefining how we store value, transfer wealth, and perceive ownership. To understand how cryptocurrency works is to understand a new asset class that blends finance with decentralized logic, offering both unprecedented opportunities and unique risks for the modern investor.

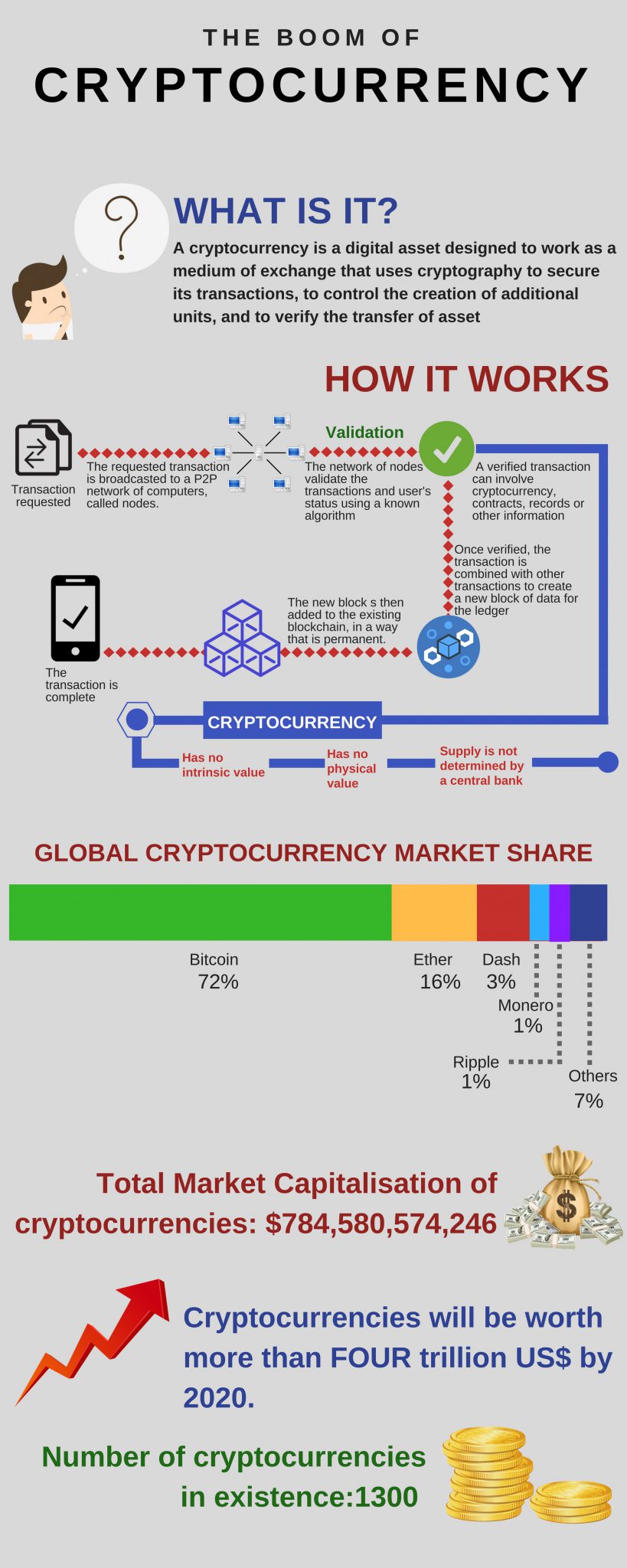

At its core, cryptocurrency is a digital or virtual currency secured by cryptography, making it nearly impossible to counterfeit or double-spend. Unlike the US Dollar or the Euro, most cryptocurrencies are decentralized networks based on blockchain technology—a distributed ledger enforced by a disparate network of computers. This article explores the mechanics of cryptocurrency through the lens of personal finance and investment, detailing how these assets function as financial tools in a digital-first economy.

Understanding the Financial Foundation of Digital Assets

To grasp how cryptocurrency functions as a monetary system, one must look beyond the “coins” and into the underlying structure that facilitates value. In traditional finance, a bank acts as the ultimate arbiter of truth; they verify that you have the funds you claim to have. In the world of cryptocurrency, this trust is outsourced to a transparent, immutable ledger.

Decentralization: Removing the Financial Middleman

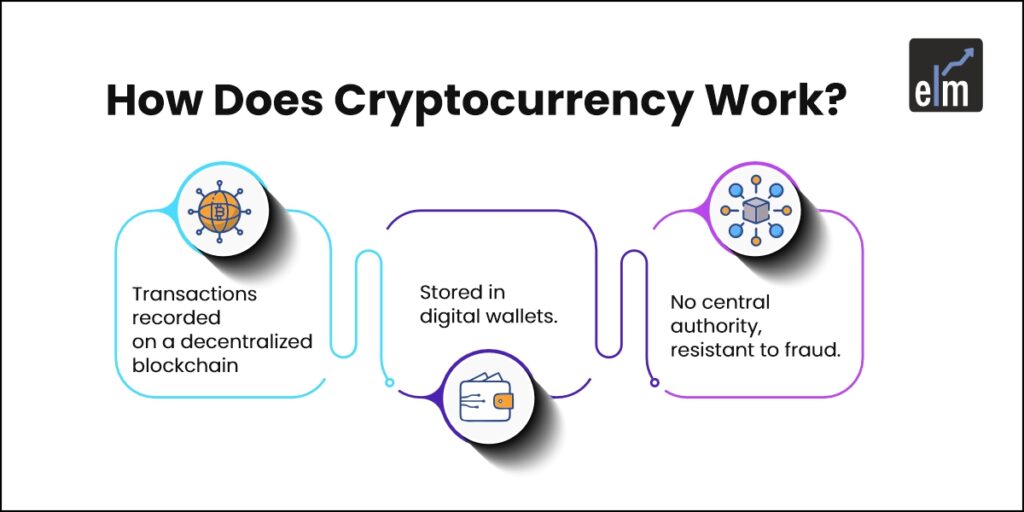

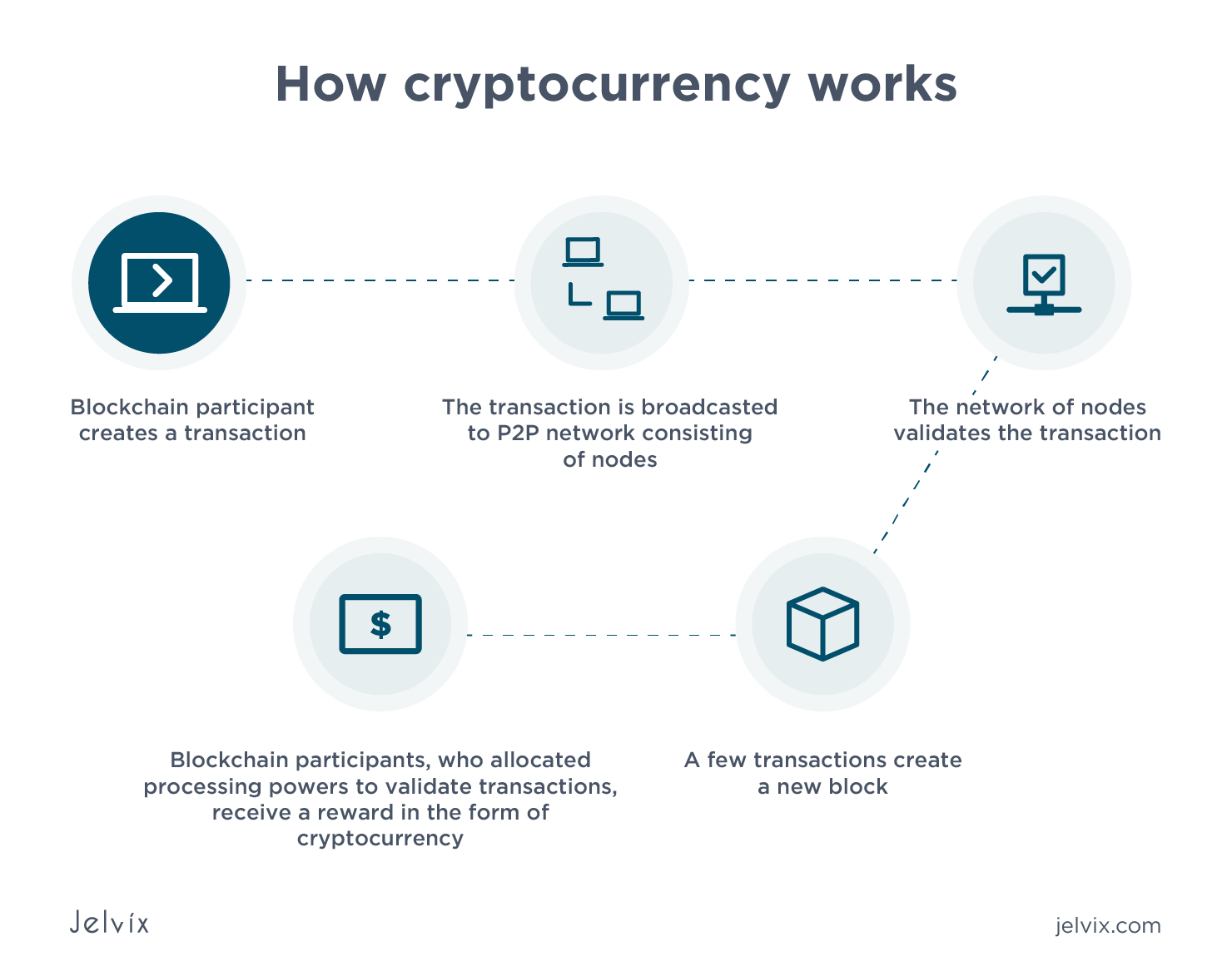

The primary innovation of cryptocurrency is the removal of intermediaries. In a traditional transaction, a fee is paid to a bank or a payment processor to verify a transfer. Cryptocurrency uses a peer-to-peer (P2P) network. When a transaction occurs, it is broadcast to a network of computers (nodes). these nodes validate the transaction using complex algorithms. Once verified, the transaction is added to a “block” and linked to the previous block, forming a chain. For the investor, this means lower transaction costs for cross-border transfers and 24/7 market access, unfettered by banking hours or geographic borders.

Tokenomics: Why Digital Coins Have Value

In the “Money” niche, value is often derived from scarcity. Traditional currencies (fiat) are subject to inflation because central banks can print more of them. Many cryptocurrencies, most notably Bitcoin, have a fixed supply. Bitcoin, for example, is capped at 21 million coins. This “hard money” characteristic is built into the software’s code. Tokenomics—the study of the supply and demand characteristics of a particular coin—is what determines its long-term viability as an investment. Factors such as “burn rates” (destroying tokens to reduce supply) or “halving events” (reducing the rate at which new coins are created) are critical mechanisms that influence the asset’s market price.

How to Navigate the Cryptocurrency Market

Entering the cryptocurrency space requires a different set of financial tools than those used for traditional stocks or bonds. Understanding the infrastructure of the market is essential for any individual looking to use cryptocurrency as a vehicle for wealth accumulation.

Exchanges and Wallets: Managing Your Digital Portfolio

An exchange is a digital marketplace where you can buy and sell cryptocurrencies using fiat money or other digital assets. These platforms, such as Coinbase or Binance, function similarly to stock brokerages but with a focus on liquidity and security in the crypto space.

However, “buying” the asset is only the first step. For the security-conscious investor, “custody” is the next hurdle. Cryptocurrency is stored in digital wallets, which consist of a public key (like an IBAN or account number) and a private key (like a digital signature or password). Investors must choose between “Hot Wallets” (connected to the internet for frequent trading) and “Cold Wallets” (offline hardware devices for long-term storage). In the realm of personal finance, the mantra “not your keys, not your coins” emphasizes the importance of self-custody to prevent losses from exchange hacks.

The Role of Fiat-to-Crypto On-Ramps

For cryptocurrency to function as an investment tool, there must be a seamless way to move money between the traditional banking system and the blockchain. “On-ramps” are the services that allow you to convert your salary or savings into digital assets. Conversely, “off-ramps” allow you to liquidate your crypto back into fiat currency to pay for real-world expenses. Understanding the fees associated with these movements is a vital part of managing a digital asset portfolio, as slippage and transaction costs can significantly eat into investment returns if not managed strategically.

Investment Strategies for the Modern Investor

Cryptocurrency is more than just a digital version of cash; it is an entire ecosystem of financial products. How you interact with this technology depends on your financial goals, risk tolerance, and time horizon.

Long-term Holding vs. Active Trading

The most common strategy in the crypto world is often referred to as “HODLing”—a play on “holding” that suggests staying invested through market volatility. Long-term investors view assets like Bitcoin or Ethereum as “digital gold” or “digital oil,” respectively, betting on the long-term adoption of the technology.

On the other hand, active trading involves leveraging market volatility to make short-term gains. This requires a deep understanding of technical analysis, market sentiment, and liquidity flows. From a financial perspective, trading is much higher risk and requires a disciplined approach to stop-losses and profit-taking to ensure that a portfolio isn’t wiped out during a “flash crash.”

Staking and Yield Farming: Generating Passive Income

One of the most revolutionary aspects of how cryptocurrency works is the ability to generate “yield” without a traditional bank. Many modern blockchains use a “Proof of Stake” (PoS) mechanism. In this system, holders of a coin can “stake” their assets to help secure the network. In exchange for this service, they are rewarded with additional coins.

This is roughly analogous to earning interest in a savings account or receiving dividends from a stock. Yield farming and Decentralized Finance (DeFi) take this a step further, allowing users to lend their digital assets to others via “smart contracts” to earn even higher returns. While these methods offer impressive passive income potential, they also introduce “smart contract risk”—the possibility that the code governing the transaction has a vulnerability.

Risk Management and Financial Security

No discussion on how cryptocurrency works is complete without addressing the volatility and security risks inherent to the niche. For an investor, protecting capital is just as important as growing it.

Volatility and Diversification

Cryptocurrency markets are known for extreme price swings. It is not uncommon for a major asset to drop 10% to 20% in a single day. From a personal finance perspective, this means that cryptocurrency should typically occupy a specific, controlled percentage of one’s total investment portfolio. Diversification within the crypto space is also key. While Bitcoin is the market leader, investing in “Altcoins” (alternative coins) or “Stablecoins” (cryptocurrencies pegged to the value of the US Dollar) can help balance the risk profile of a digital portfolio. Stablecoins, in particular, serve as a “safe haven” during periods of high volatility, allowing investors to move out of risky assets without exiting the crypto ecosystem entirely.

Tax Implications and Regulatory Landscapes

As cryptocurrency has grown, so too has the interest of tax authorities and regulators. In many jurisdictions, cryptocurrency is treated as property rather than currency. This means that every time you trade one coin for another, or use crypto to buy a cup of coffee, you may be triggering a capital gains tax event.

Furthermore, the regulatory landscape is constantly shifting. Governments are currently debating how to categorize different tokens—whether they are securities, commodities, or something entirely new. Staying informed on these regulations is a crucial part of financial planning. Failure to account for tax liabilities or ignoring the legal status of an exchange can lead to significant financial penalties, negating any gains made through savvy investing.

Conclusion: The Evolution of Personal Finance

Cryptocurrency works by combining cryptographic security with decentralized consensus, creating a system where value can be moved and stored without the need for a central authority. For the individual, it represents a new frontier of financial sovereignty. It offers the potential for high returns and a hedge against traditional market failures, but it demands a higher level of personal responsibility and education.

As we move further into a digital age, the lines between traditional banking and decentralized finance will continue to blur. Whether you view cryptocurrency as a speculative asset, a technological experiment, or the future of global commerce, its mechanics are fundamentally changing the way we think about money. By understanding the underlying structures of blockchain, the tools of the trade, and the strategies for risk management, investors can position themselves to navigate this complex but rewarding financial landscape with confidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.