Understanding your monthly income is a fundamental aspect of sound financial management. Whether you’re an individual striving for personal financial stability, a freelancer navigating variable earnings, or a business owner tracking profitability, accurately computing your monthly income is the bedrock upon which informed financial decisions are built. This process is not merely an exercise in arithmetic; it’s a crucial step towards budgeting effectively, setting financial goals, managing debt, and ultimately, achieving financial well-being. In the realm of personal finance, a clear picture of your monthly income empowers you to make strategic choices about spending, saving, and investing. For businesses, it’s the pulse of their operation, indicating revenue streams, cash flow, and the overall health of the enterprise. This article will guide you through the essential steps and considerations for accurately computing your monthly income, ensuring you have the clarity needed to take control of your financial future.

Understanding the Nuances of Income

Before diving into calculations, it’s vital to grasp the different types of income and how they are treated. Not all money that comes into your possession is considered “income” in the same way. Distinguishing between gross and net income, as well as understanding various income sources, is paramount for an accurate assessment.

Gross vs. Net Income: The Essential Distinction

The first and most critical distinction to make is between gross income and net income. This difference is not just semantic; it has significant practical implications for budgeting and financial planning.

Gross Income: The Top-Line Figure

Gross income represents the total amount of money earned before any deductions are made. For an individual with a traditional salaried job, this is the figure stated on your offer letter or employment contract. It’s the total revenue generated from your primary source of employment. For business owners, gross income, often referred to as gross revenue or gross sales, is the total income generated from the sale of goods or services before any costs of goods sold or operating expenses are subtracted. This figure is a snapshot of your earning potential at its highest level. It’s important to know this number as it reflects your overall productivity and market value. However, it is rarely the amount you have available to spend or save.

Net Income: The Take-Home Reality

Net income, often called take-home pay or disposable income, is what remains after all deductions have been subtracted from your gross income. These deductions can vary significantly depending on whether you are an individual or a business. For individuals, common deductions include:

- Taxes: Federal, state, and local income taxes are typically withheld from your paycheck.

- Social Security and Medicare Contributions: These mandatory contributions fund retirement and healthcare programs.

- Health Insurance Premiums: If you receive health insurance through your employer, your portion of the premium is usually deducted.

- Retirement Contributions: Contributions to 401(k) or other employer-sponsored retirement plans are often pre-tax deductions.

- Other Deductions: This can include union dues, life insurance premiums, or wage garnishments.

For businesses, net income (also known as profit) is calculated after subtracting all expenses from gross revenue. These expenses include:

- Cost of Goods Sold (COGS): The direct costs attributable to the production or purchase of the goods sold by a company.

- Operating Expenses: Rent, utilities, salaries, marketing costs, insurance, etc.

- Interest Expenses: Costs incurred from borrowing money.

- Taxes: Corporate income taxes.

Net income is the more practical figure for budgeting and everyday financial decision-making, as it represents the actual amount of money you have available to spend, save, or invest.

Identifying All Income Sources

Beyond your primary employment or business revenue, individuals and businesses often have multiple sources of income. Accurately computing your total monthly income requires identifying and quantifying all of these.

For Individuals: Beyond the Paycheck

Many individuals supplement their primary income with various other streams. These can include:

- Freelance Work and Side Hustles: Income earned from offering services or selling products outside of your main job. This can be highly variable.

- Rental Income: Revenue generated from properties you own and rent out.

- Investment Income: Dividends from stocks, interest from bonds or savings accounts, and capital gains from selling assets.

- Royalties: Payments received for the use of your intellectual property (e.g., books, music, patents).

- Government Benefits: Social Security, unemployment benefits, disability payments, etc.

- Alimony or Child Support: Regular payments received from a former spouse or partner.

It’s crucial to track these sources consistently, especially if they are variable, to get a realistic monthly average.

For Businesses: Diversifying Revenue Streams

Businesses can also generate income from various avenues:

- Sales of Goods/Services: The primary revenue driver.

- Interest Income: Earned on business savings accounts or short-term investments.

- Rental Income: If the business owns property and rents out portions of it.

- Licensing Fees: For intellectual property owned by the business.

- Government Grants or Subsidies: Financial assistance received from public sources.

A comprehensive understanding of all revenue streams is essential for a complete financial picture.

Methods for Computing Monthly Income

The method for computing your monthly income will depend on your employment status and the nature of your income. For those with stable, predictable incomes, the process is straightforward. For those with variable income, it requires a more nuanced approach.

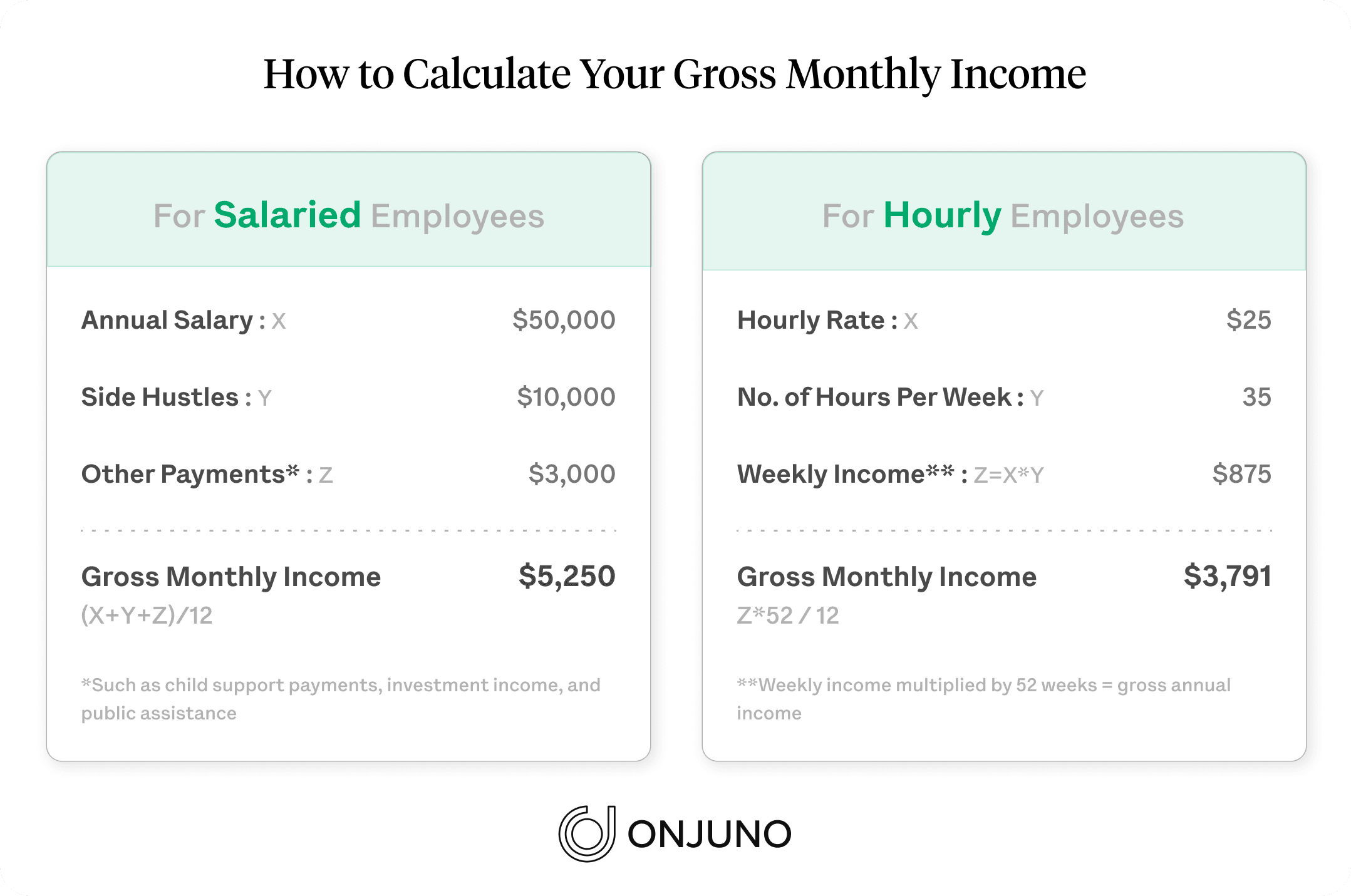

For Salaried Employees: The Straightforward Calculation

If you are a salaried employee, computing your monthly net income is relatively simple. Your gross monthly income is typically your annual salary divided by 12. To find your net monthly income, you will refer to your pay stubs.

Analyzing Your Pay Stub

Your pay stub is a detailed record of your earnings and deductions for a specific pay period. It will clearly show your gross pay for that period and a breakdown of all deductions. By summing up the net pay from each pay stub within a month, you can determine your total monthly net income. Most salaried employees are paid bi-weekly or semi-monthly.

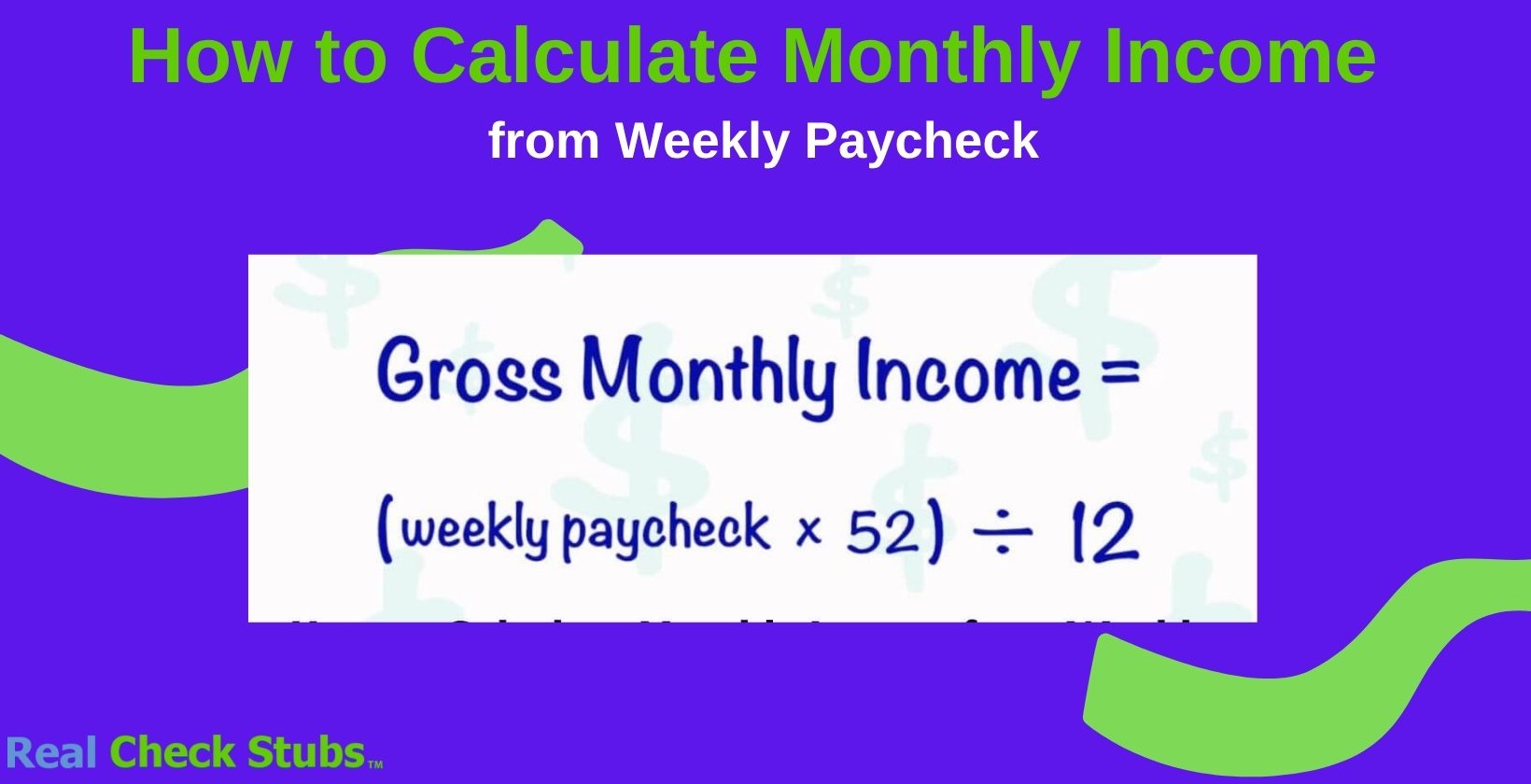

- Bi-weekly Pay: If you are paid every two weeks, you will receive 26 paychecks per year. This means that in some months, you will receive three paychecks instead of two. This can lead to a slightly higher monthly income in those months.

- Semi-monthly Pay: If you are paid twice a month (e.g., on the 15th and the last day), you will receive 24 paychecks per year, resulting in a more consistent monthly income.

To compute your average monthly net income, you can:

- Sum your net pay for all pay periods within a given month.

- Alternatively, for a more stable budgeting figure, calculate your annual net income (total net pay for the year) and divide it by 12. This will give you a consistent monthly average, smoothing out the fluctuations caused by having three paychecks in some months.

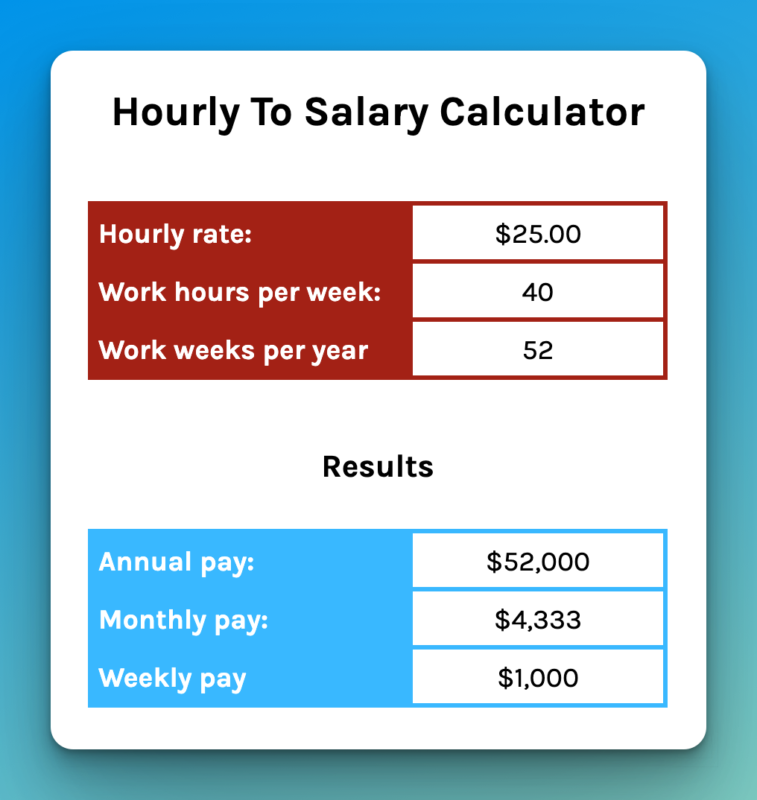

For Hourly Employees: Tracking Your Hours

Hourly employees’ income fluctuates based on the number of hours worked and their hourly rate. Computing monthly income requires diligent tracking.

Calculating Gross and Net Hourly Pay

First, determine your gross hourly rate. Then, multiply this by the number of hours you expect to work in a month. Be sure to account for potential overtime, which is often paid at a higher rate (e.g., 1.5 times the regular rate).

Your net hourly pay is your gross hourly pay minus the deductions per hour. However, it’s often more practical to calculate your total gross pay for the month and then deduct taxes and other mandatory contributions.

Consistent Time Tracking and Forecasting

- Time Sheets: Maintain accurate and consistent time sheets. Use official company systems or reliable apps to log your hours.

- Forecasting: Estimate your monthly income by multiplying your expected hours (including any planned overtime) by your hourly rate.

- Pay Stub Review: After each pay period, review your pay stub to ensure accuracy and to understand the net amount received. Summing these net amounts for the month will give you your actual monthly take-home pay.

For budgeting purposes, it’s advisable to be conservative with your income projections, especially if your work hours can fluctuate significantly.

For Freelancers and Gig Workers: Navigating Variable Income

Freelancers and gig economy workers face the challenge of irregular and unpredictable income. Computing their monthly income requires a different strategy that focuses on averages and projections.

Averaging Income Over Time

The most effective method for freelancers is to calculate an average monthly income based on past earnings.

- Track All Income: Diligently record every payment received from all clients and platforms.

- Calculate Total Annual Income: Sum up all income earned over the past 12 months.

- Divide by 12: Divide your total annual income by 12 to arrive at your average monthly income.

This average provides a more stable figure for budgeting and financial planning than relying on the income from a single month, which could be unusually high or low.

Projecting Future Income and Managing Cash Flow

Beyond averaging, freelancers need to project future income.

- Client Contracts: Review current and upcoming client contracts to estimate expected earnings.

- Pipeline: Keep track of potential leads and projects in your pipeline.

- Seasonal Trends: Be aware of any seasonal fluctuations in your industry.

Given the variability, it’s also crucial to manage cash flow carefully. It’s often wise to maintain a buffer of savings to cover expenses during leaner months. Setting aside a percentage of each payment for taxes is also non-negotiable for freelancers.

For Business Owners: Tracking Revenue and Profitability

For business owners, computing monthly income is synonymous with tracking revenue and profitability. This involves looking beyond just sales figures to understand the true financial health of the enterprise.

Differentiating Revenue and Profit

As discussed earlier, revenue is the total income from sales. Profit is what’s left after all expenses are paid. For business owners, the most critical monthly income figure to compute is often net profit.

Utilizing Accounting Software and Tools

Modern accounting software is indispensable for businesses of all sizes.

- Software Solutions: Platforms like QuickBooks, Xero, or Wave can automate much of the income and expense tracking process. They allow you to categorize transactions, generate financial reports, and provide a clear view of your financial performance.

- Chart of Accounts: A well-structured chart of accounts is essential for categorizing revenue and expenses accurately.

- Regular Financial Reviews: Schedule regular (at least monthly) reviews of your profit and loss statements (also known as income statements) and cash flow statements.

The income statement will detail your gross revenue, cost of goods sold, operating expenses, and ultimately, your net profit for the month. Understanding these components is vital for identifying areas of strength and weakness in your business operations.

Strategies for Accurate Income Computation and Management

Beyond the calculation itself, adopting effective strategies can significantly enhance the accuracy and usefulness of your monthly income computations, leading to better financial control.

Maintaining Detailed Records

Regardless of your income source, meticulous record-keeping is the cornerstone of accurate financial computation.

Digital vs. Manual Record Keeping

- Digital Tools: Leverage spreadsheets (Excel, Google Sheets), accounting software, or dedicated budgeting apps. These tools offer automation, error reduction, and easier analysis.

- Manual Records: For some, physical ledgers or notebooks may suffice, but they require discipline to avoid errors and are less efficient for complex financial situations.

The key is consistency. Whichever method you choose, ensure you are diligent in recording every income transaction promptly.

The Importance of Documentation

Keep supporting documents for all income transactions. This includes:

- Pay Stubs: For salaried and hourly employees.

- Invoices and Receipts: For freelancers and business owners.

- Bank Statements: To verify deposits and transactions.

- Tax Documents: For freelance and investment income.

These documents serve as proof and are invaluable for tax purposes, audits, or resolving any discrepancies.

Forecasting and Budgeting Based on Income

Once you have a clear understanding of your monthly income, the next logical step is to integrate this knowledge into your financial planning through forecasting and budgeting.

Creating a Realistic Budget

A budget is a plan for how you will spend and save your income. It should be directly informed by your computed monthly income.

- Allocate Funds: Assign specific amounts for essential expenses (housing, utilities, food, transportation), discretionary spending (entertainment, dining out), savings, and debt repayment.

- Prioritize Needs: Ensure that all essential expenses are covered before allocating funds to discretionary items.

- Budgeting Methods: Explore different budgeting methods like the 50/30/20 rule, zero-based budgeting, or envelope budgeting to find what works best for you.

A well-structured budget acts as a roadmap, guiding your spending and helping you stay on track toward your financial goals.

Income Forecasting for Stability

For those with variable income, forecasting is not just about prediction; it’s about proactive management.

- Scenario Planning: Develop best-case, worst-case, and most-likely scenarios for your monthly income. This helps you prepare for fluctuations.

- Cash Flow Management: Understand your typical income cycle and your expenditure cycle. Try to align them to avoid shortfalls. For instance, if you know a particular month is likely to be low-income, plan to reduce expenses or draw from savings in advance.

- Setting Financial Goals: Use your forecasted income to set realistic short-term and long-term financial goals, such as saving for a down payment, investing, or building an emergency fund.

By proactively forecasting and budgeting, you transform your computed monthly income from a mere number into a powerful tool for achieving financial security and success.

Leveraging Financial Tools and Technology

In today’s digital age, a plethora of financial tools and technologies can simplify and enhance the process of computing and managing your monthly income.

Personal Finance Apps and Software

For individuals, personal finance apps offer an integrated approach to tracking income and expenses.

Features and Benefits

- Automated Tracking: Many apps link directly to your bank accounts and credit cards, automatically importing transactions.

- Categorization: They can automatically categorize income and expenses, providing insights into spending habits.

- Budgeting Tools: Built-in budgeting features allow you to set spending limits and track your progress.

- Goal Setting: You can set financial goals (e.g., saving for a down payment) and monitor your progress.

- Reporting: Generate reports on income, expenses, net worth, and cash flow.

Popular examples include Mint, YNAB (You Need A Budget), Personal Capital, and PocketGuard. These tools democratize financial management, making it accessible and manageable for a wide audience.

Accounting Software for Businesses

For businesses, robust accounting software is not just helpful; it’s essential for accurate financial reporting and compliance.

Key Features for Income Tracking

- Invoicing: Create and send professional invoices to clients, tracking payment statuses.

- Expense Management: Record and categorize all business expenses.

- Bank Reconciliation: Match your accounting records with your bank statements to ensure accuracy.

- Financial Reporting: Generate key reports such as Profit & Loss statements, Balance Sheets, and Cash Flow statements.

- Tax Preparation Support: Many software solutions can help generate reports needed for tax filing.

For small businesses, platforms like QuickBooks Online, Xero, or Wave offer scalable solutions. Larger enterprises may utilize more comprehensive ERP (Enterprise Resource Planning) systems.

Online Banking and Payment Platforms

Modern banking and payment platforms provide real-time visibility into your financial activities, aiding in income computation.

Real-time Transaction Monitoring

- Online Banking Portals: Most banks offer online portals and mobile apps that allow you to view your account balances and transaction history in real-time. This immediate access is crucial for tracking income as it arrives.

- Payment Processors: Platforms like PayPal, Stripe, and Square are commonly used by freelancers and small businesses. They provide detailed dashboards and reports of payments received, making it easier to aggregate income.

By regularly reviewing these platforms, you can stay on top of your incoming funds and ensure your records align with actual deposits.

Conclusion: Empowering Financial Decisions Through Accurate Income Computation

Accurately computing your monthly income is not a one-time task but an ongoing process that forms the bedrock of sound financial health, whether for personal or business purposes. It provides the clarity needed to navigate complex financial landscapes, make informed decisions, and achieve your financial aspirations. By understanding the distinctions between gross and net income, identifying all revenue streams, and employing appropriate calculation methods for your specific circumstances, you gain a powerful tool for financial control.

The strategies outlined – meticulous record-keeping, proactive forecasting, and diligent budgeting – transform raw data into actionable insights. Furthermore, leveraging the vast array of financial tools and technologies available today simplifies this process, offering automation, improved accuracy, and deeper financial understanding. Whether you are an individual seeking to manage your personal finances, a freelancer striving for stability, or a business owner focused on profitability, a firm grasp of your monthly income is the essential first step. Embrace these practices, utilize the available resources, and empower yourself to make confident, strategic financial decisions that pave the way for a secure and prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.