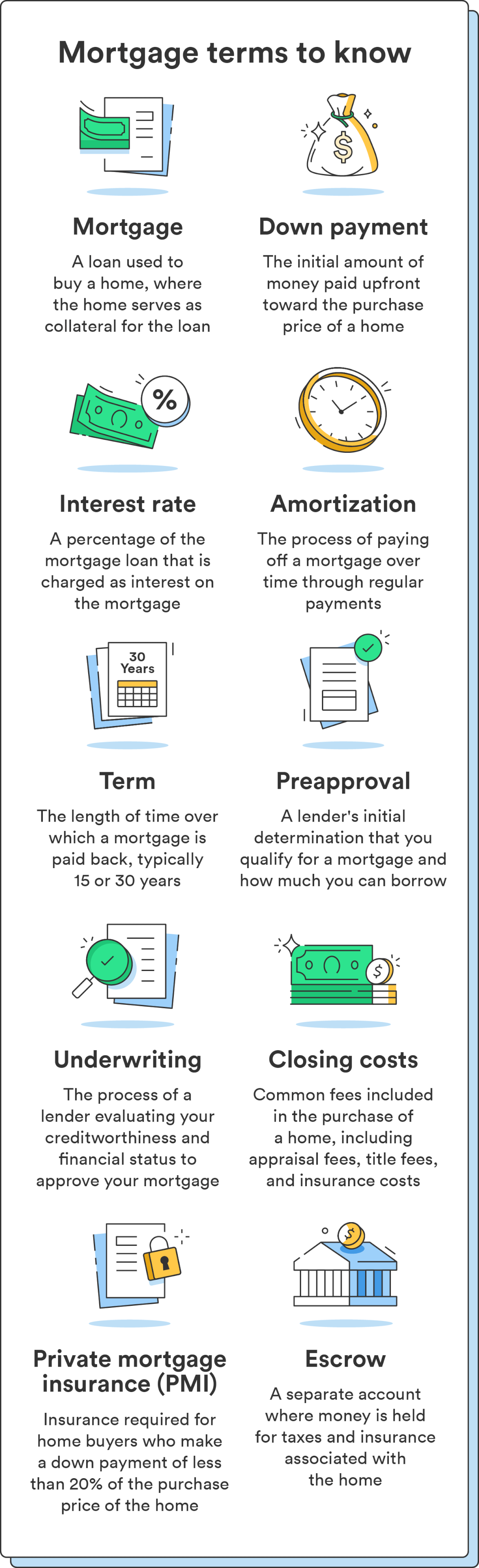

For most individuals, the purchase of a home represents the most significant financial transaction of their lives. It is more than just a lifestyle upgrade; it is a sophisticated maneuver in personal finance that involves long-term debt management, asset allocation, and wealth preservation. Securing a mortgage is the bridge between the dream of ownership and the reality of a deed. However, the path to obtaining a mortgage is paved with complex terminology, rigorous financial scrutiny, and a multi-step process that requires meticulous preparation.

To successfully navigate this landscape, one must understand that a mortgage is not merely a loan, but a financial partnership between a borrower and a lender. To qualify, you must demonstrate your reliability, financial stability, and capacity for long-term fiscal responsibility. This guide provides a deep dive into the “Money” niche of home financing, outlining exactly how you can position yourself to secure the best possible mortgage terms.

1. Strengthening Your Financial Foundation: Credit and Income

Before you ever step foot into a bank or contact a mortgage broker, you must evaluate your financial profile through the eyes of a lender. Lenders are risk-averse; they want to ensure that the probability of default is as close to zero as possible. They determine this risk by examining three primary pillars: your credit score, your debt-to-income ratio, and your history of steady income.

Improving Your Credit Score for Optimal Rates

Your credit score is perhaps the most influential factor in determining your mortgage interest rate. A difference of even 0.5% in an interest rate can result in tens of thousands of dollars saved or spent over a 30-year term. To get a mortgage, most conventional lenders look for a score of at least 620, though a score above 740 is typically required to unlock the most competitive “prime” rates.

To prepare, you should pull your credit reports from the three major bureaus—Equifax, Experian, and TransUnion. Look for errors, such as accounts you didn’t open or paid debts marked as outstanding, and dispute them immediately. Furthermore, reduce your credit utilization ratio by paying down revolving balances. Lenders prefer to see that you are using less than 30% of your available credit limits.

Understanding the Debt-to-Income (DTI) Ratio

Lenders use the Debt-to-Income (DTI) ratio to measure your ability to manage monthly payments. This is calculated by dividing your total monthly debt obligations (student loans, car payments, credit card minimums) by your gross monthly income.

Most mortgage programs require a DTI ratio of 43% or lower, although some government-backed programs allow for higher thresholds. If your DTI is too high, you have two levers to pull: increase your income or decrease your debt. For those looking to get a mortgage, it is often advisable to pause any new major purchases—such as a new car or high-end furniture on credit—until after the house closing, as these add to your DTI and can jeopardize your approval.

Establishing Proof of Stable Income

Consistency is key in the eyes of a mortgage underwriter. Lenders typically want to see a two-year history of stable employment within the same industry. If you are a W-2 employee, this process is straightforward, requiring pay stubs and tax returns.

However, for the self-employed or those with “gig economy” income, the scrutiny is more intense. You will likely need to provide at least two years of full federal tax returns (including Schedule C) to prove that your business is profitable and that your income is not overly volatile. In the world of personal finance, your “taxable income” is what matters; if you use too many deductions to lower your tax bill, you might accidentally lower the amount of mortgage you qualify for.

2. The Financial Preparation Phase: Capital and Liquidity

Once your credit and income are in order, the next step in getting a mortgage is amassing the necessary capital. A mortgage isn’t just about the monthly payment; it requires significant “skin in the game” upfront.

Saving for the Down Payment: The 20% Myth

A common misconception in personal finance is that a 20% down payment is mandatory. While 20% is ideal because it allows you to avoid Private Mortgage Insurance (PMI) and gives you immediate equity, many loan programs allow for much less. FHA loans require as little as 3.5% down, and some conventional loans for first-time buyers allow for 3%.

However, from a wealth-building perspective, the more you put down, the less interest you pay over time. You must balance the desire to own a home sooner with the long-term cost of a higher loan-to-value (LTV) ratio. If you choose a low-down-payment option, ensure you have a plan to eventually cancel your PMI once your equity reaches 20% to optimize your monthly cash flow.

Accounting for Closing Costs and Cash Reserves

Many prospective homeowners forget that the down payment is not the only upfront cost. Closing costs typically range from 2% to 5% of the home’s purchase price. These fees cover appraisals, title insurance, attorney fees, and taxes.

Furthermore, lenders often require “cash reserves.” This is liquid capital (savings, stocks, or money market funds) that remains in your account after the closing. Lenders want to see that you won’t be “house poor”—the state of having a beautiful home but no money left for maintenance or emergencies. Having 3 to 6 months of mortgage payments in reserve can significantly strengthen your application.

Sourcing Your Funds

Lenders are required by law to track the source of your funds to prevent money laundering. If you are receiving a “gift” from a family member to help with the down payment, this must be documented with a “gift letter” stating that the money is not a loan and does not need to be repaid. Large, unexplained deposits into your bank accounts in the months leading up to a mortgage application can trigger red flags, so it is best to keep your finances “seasoned” and transparent.

3. Selecting the Right Mortgage Product

Not all mortgages are created equal. Choosing the right one depends on your financial goals, how long you plan to stay in the home, and your risk tolerance.

Conventional vs. Government-Backed Loans

- Conventional Loans: These are not insured by the federal government and usually follow the guidelines set by Fannie Mae or Freddie Mac. They are best for those with good credit scores and stable finances.

- FHA Loans: Insured by the Federal Housing Administration, these are popular with first-time buyers or those with lower credit scores. They require lower down payments but come with mandatory mortgage insurance premiums.

- VA and USDA Loans: These are specialized products. VA loans are available to veterans and active-duty service members with zero down payment. USDA loans are designed for low-to-moderate-income buyers in specific rural areas.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The choice between a fixed-rate and an adjustable-rate mortgage (ARM) is a fundamental decision in financial planning. A 30-year fixed-rate mortgage offers stability; your interest rate never changes, making it easier to budget for the long term.

An ARM usually offers a lower “teaser” rate for an initial period (5, 7, or 10 years), after which the rate adjusts based on market indices. ARMs can be beneficial if you plan to sell the home or refinance before the adjustment period begins. However, they carry the risk of significantly higher payments in the future if interest rates rise.

4. The Application and Underwriting Journey

With your finances prepared and your loan type chosen, you enter the formal process of securing the loan. This is where the theoretical meets the practical.

The Power of Pre-Approval

Before you look at a single house, you should obtain a mortgage pre-approval letter. This is different from a “pre-qualification,” which is a surface-level estimate. A pre-approval involves a lender actually verifying your credit and documentation. In a competitive real estate market, a pre-approval letter is your “license to shop,” signaling to sellers that you are a serious and capable buyer.

Navigating Underwriting and the Appraisal

Once you find a home and your offer is accepted, you enter the underwriting phase. The underwriter is the “detective” of the mortgage world, double-checking every detail of your financial life. During this time, the lender will also order an appraisal of the property. The appraisal is a critical financial safeguard; the lender will not lend you more money than the home is actually worth. If a home is appraised for less than the purchase price, you may have to cover the “appraisal gap” in cash or renegotiate the price with the seller.

The “Clear to Close”

The final stage is receiving the “Clear to Close.” This means the lender has finished their review and is ready to fund the loan. At this stage, you will receive a Closing Disclosure (CD), a document that outlines your final loan terms, monthly payments, and the exact amount of “cash to close” you need to provide.

5. Strategic Management of Your Mortgage Debt

Getting the mortgage is just the beginning. From a personal finance perspective, a mortgage is a tool that must be managed.

Amortization and Extra Payments

Understand your amortization schedule. In the early years of a 30-year mortgage, the vast majority of your payment goes toward interest rather than the principal balance. By making just one extra principal-only payment per year, or by rounding up your monthly payments, you can shave years off your loan and save tens of thousands of dollars in interest.

Monitoring Refinance Opportunities

The financial market is dynamic. If interest rates drop significantly after you’ve secured your mortgage, or if your credit score improves drastically, you may want to consider a “rate-and-term” refinance. This allows you to replace your current mortgage with a new one at a lower rate, reducing your monthly overhead and increasing your long-term wealth.

Conclusion

Getting a mortgage is a rigorous financial marathon that requires discipline, transparency, and strategic planning. By focusing on your credit health, managing your debt-to-income ratio, and choosing the right mortgage product, you transform a complex hurdle into a structured financial victory. Remember that a mortgage is not just a debt—it is a leveraged investment in your future. Approaching it with the mindset of a financial professional ensures that your home remains a source of security and wealth for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.