The question of “what are loan rates today” is more than a simple inquiry into a percentage point; it is a gateway to understanding the pulse of the global economy. For homeowners, entrepreneurs, and individual consumers, interest rates represent the cost of time and the price of opportunity. In a financial climate characterized by rapid shifts in monetary policy and fluctuating inflation, staying informed about current lending rates is essential for making sound financial decisions.

Today’s loan rates are shaped by a complex interplay of central bank policies, market demand, and individual risk profiles. Whether you are looking to purchase a new home, expand a business, or consolidate high-interest debt, understanding the current environment allows you to time your moves strategically and minimize the lifetime cost of your borrowing.

Understanding the Factors Influencing Today’s Loan Rates

To understand why loan rates sit at their current levels, one must look toward the macro-economic foundations that dictate the flow of capital. Interest rates do not exist in a vacuum; they are the result of deliberate policy and spontaneous market reactions.

The Role of the Federal Reserve and Central Banks

The single most influential factor in determining loan rates is the policy set by the Federal Reserve (or the equivalent central bank in other jurisdictions). By adjusting the federal funds rate—the rate at which commercial banks lend to one another overnight—the Fed sets a benchmark for all other consumer interest rates. When the Fed raises rates to combat inflation, the cost of borrowing for banks increases, which is then passed on to consumers in the form of higher mortgage, auto, and personal loan rates. Conversely, when the economy requires a boost, the Fed lowers rates to encourage spending and investment.

Inflation and Economic Indicators

Lenders are inherently cautious about inflation because it erodes the purchasing power of the money they will be paid back in the future. If inflation is high, lenders demand higher interest rates to compensate for the diminishing value of the dollar. Key indicators such as the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index are closely watched by market analysts. When these reports show rising prices, market expectations for future interest rates typically trend upward.

Market Sentiment and Global Events

Loan rates, particularly long-term rates like the 30-year mortgage, are also influenced by the bond market. The yield on the 10-year Treasury note is a primary benchmark. When investors are nervous about the economy, they often flock to the safety of government bonds, which can drive yields (and subsequently loan rates) down. However, in times of geopolitical instability or supply chain disruptions, the resulting economic uncertainty can lead to volatility, making it difficult for lenders to offer stable, low rates.

Breaking Down Current Rates Across Different Loan Types

While there is a general trend in “the market,” different types of loans react differently to economic shifts. Understanding the nuances between these products is vital for accurate financial planning.

Mortgage Rates: Fixed vs. Adjustable

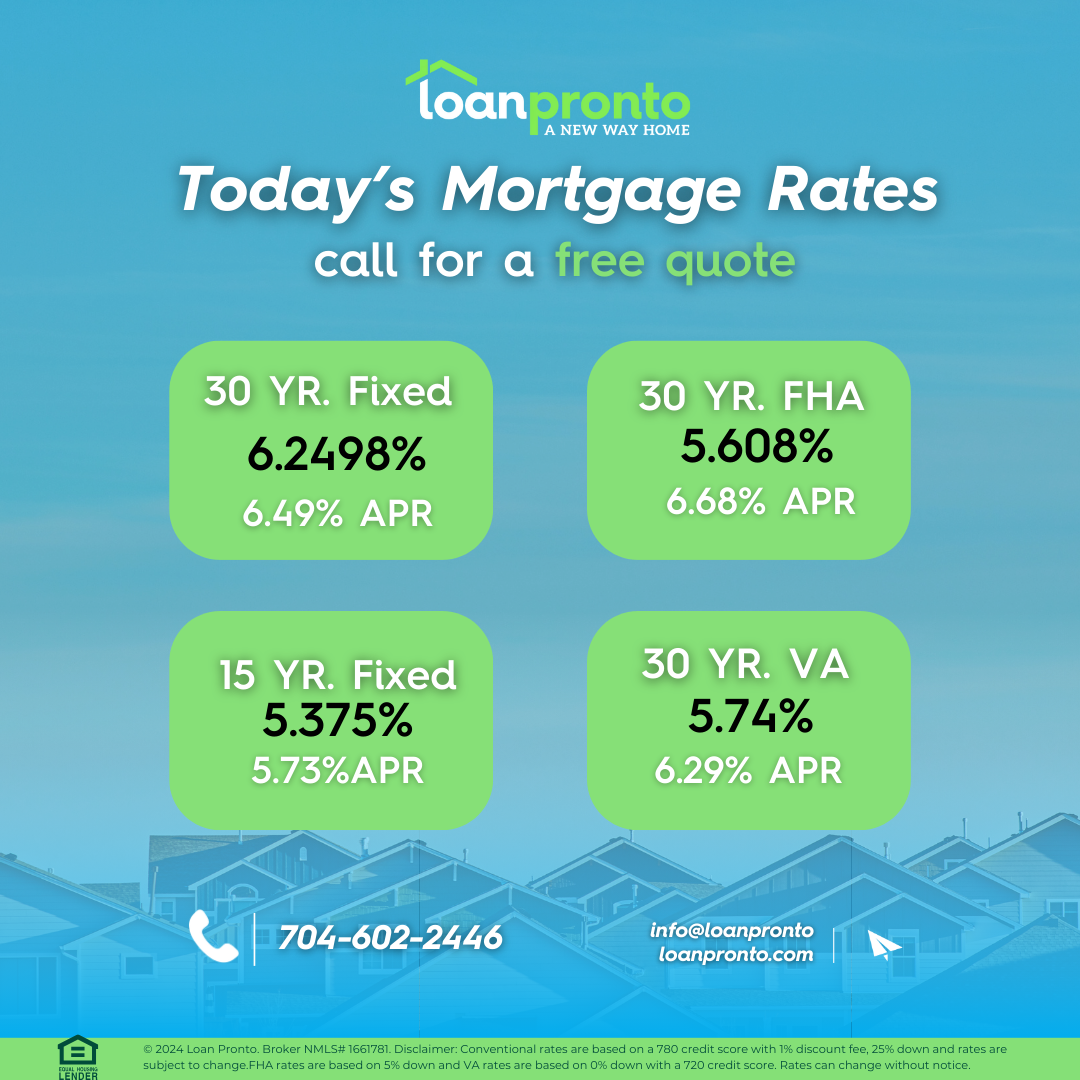

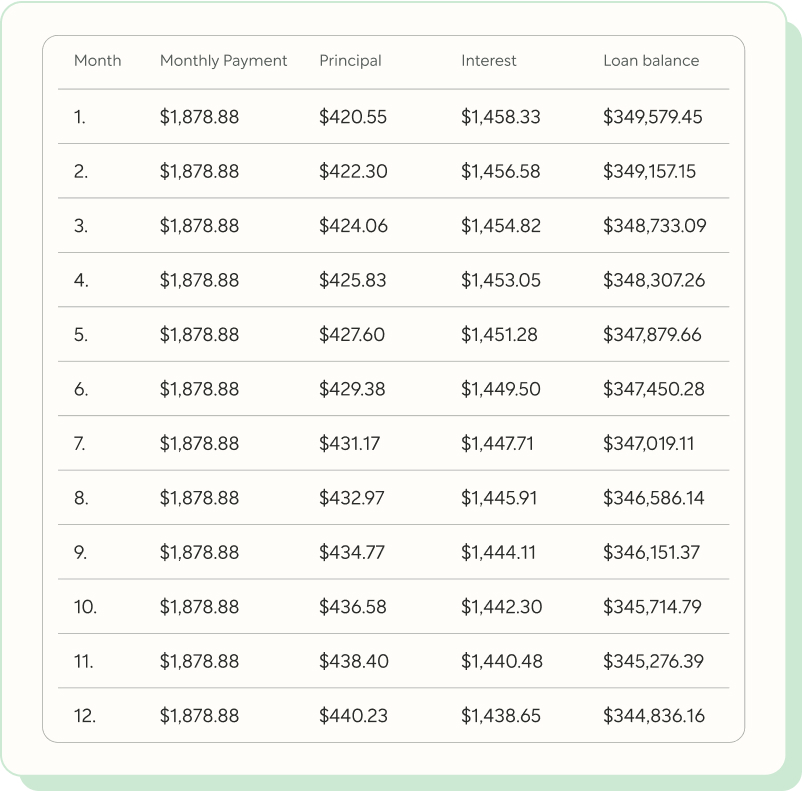

Mortgage rates are often the most discussed because of the sheer size of the debt. Today’s mortgage market is defined by a significant spread between 15-year and 30-year fixed-rate options. A 30-year fixed-rate mortgage offers stability but usually carries a higher interest rate than its 15-year counterpart. Furthermore, Adjustable-Rate Mortgages (ARMs) have regained some popularity in high-rate environments, offering a lower initial rate for a set period (such as five or seven years) before adjusting based on market conditions. Borrowers must weigh the immediate savings of an ARM against the long-term risk of rising rates.

Personal Loan Rates and Unsecured Debt

Personal loans are typically “unsecured,” meaning they aren’t backed by collateral like a house or a car. Because of this, personal loan rates are significantly higher than mortgage rates and are highly sensitive to the borrower’s creditworthiness. Today, personal loan rates can range anywhere from 6% for “excellent” credit borrowers to over 35% for those with “poor” credit. These loans are frequently used for debt consolidation, and their value lies in providing a fixed interest rate that is often lower than the variable rates found on credit cards.

Auto Loans and Student Loan Trends

The auto loan market has seen substantial tightening recently. With the rising cost of vehicles and higher interest rates, the average monthly car payment has reached historic highs. Lenders have become more stringent with their requirements, making it essential for buyers to shop around. Meanwhile, student loan rates—particularly federal ones—are set annually by Congress and remain fixed for the life of the loan, though private student loan rates continue to fluctuate in line with broader market benchmarks like the SOFR (Secured Overnight Financing Rate).

How Your Personal Profile Impacts the Rate You Receive

While the “headline” rate you see advertised online might look appealing, the actual rate you are offered depends heavily on your unique financial profile. Lenders use several metrics to determine the risk of lending to you.

The Importance of Credit Scores

Your credit score is the most significant factor in the interest rate equation. Lenders generally categorize borrowers into tiers: Excellent (740+), Good (670-739), Fair (580-669), and Poor (under 580). A borrower in the “excellent” tier might qualify for a mortgage rate that is a full percentage point lower than a borrower in the “fair” tier. Over the life of a 30-year loan, that single percentage point can translate into tens of thousands of dollars in interest savings.

Debt-to-Income Ratio (DTI)

Lenders don’t just want to know that you pay your bills; they want to know how much “room” you have in your budget. The Debt-to-Income ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Most lenders prefer a DTI below 36%, though some programs allow for higher ratios. A lower DTI suggests that you are less likely to default, which can sometimes help you secure more favorable terms or higher loan amounts.

Loan-to-Value (LTV) and Down Payments

In the world of secured lending—such as home and auto loans—the amount of equity you have matters. The Loan-to-Value (LTV) ratio compares the loan amount to the appraised value of the asset. A lower LTV (resulting from a larger down payment) reduces the lender’s risk. For example, in the mortgage world, reaching an LTV of 80% or lower not only helps secure a better interest rate but also allows the borrower to avoid Private Mortgage Insurance (PMI), further reducing the monthly cost.

Strategies to Secure the Best Possible Rate Right Now

In a high-rate or volatile environment, being proactive can save you a significant amount of money. You do not have to be a passive recipient of whatever rate a bank offers you.

Comparison Shopping and Pre-Qualification

One of the most common mistakes borrowers make is accepting the first loan offer they receive. Studies have shown that consumers who get at least three to five quotes can save thousands over the life of their loan. Digital lending platforms have made this easier than ever, allowing for “soft” credit pulls that provide pre-qualification rates without impacting your credit score. Comparing traditional banks, credit unions, and online-only lenders is the best way to find the most competitive “today” rate.

Rate Locks and Timing the Market

If you find a favorable rate during your search, you may want to consider a “rate lock.” Because loan rates can change multiple times in a single day, a rate lock guarantees your quoted interest rate for a specific period (usually 30 to 60 days) while your loan is being processed. This protects you from sudden market spikes. However, be aware of the “float-down” option, which allows you to take advantage of a lower rate if market rates drop during your lock period.

Improving Your Financial Health Before Applying

If you aren’t in a rush to borrow, taking six months to improve your financial profile can pay dividends. Paying down revolving credit card balances to lower your credit utilization, correcting errors on your credit report, and avoiding new credit inquiries can boost your score by 20 to 50 points. In the eyes of a lender, this movement can jump you into a higher credit tier, unlocking lower interest rates that were previously unavailable.

The Future Outlook: What to Expect in the Coming Quarters

Predicting the exact movement of loan rates is notoriously difficult, but financial analysts look at several key signals to forecast the coming months.

Predictive Models and Expert Forecasts

Currently, most economists are looking for a “plateau” or a gradual “pivot” in interest rate policy. If inflation continues to cool toward the central bank’s targets, there is a general expectation that the Federal Reserve may begin to lower the federal funds rate. This would lead to a gradual decline in consumer loan rates. However, if the labor market remains overheated or if energy prices spike due to global conflict, rates may remain “higher for longer.”

Navigating today’s loan rates requires a blend of macroeconomic awareness and personal financial discipline. By understanding the forces that drive the market and optimizing your own financial standing, you can secure the capital you need at the best possible price, ensuring that your financial future remains on a solid foundation. Whether the trend is up or down, the most informed borrower is always the one who comes out ahead.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.