The question of what percentage of Americans live below the poverty line is not merely a statistical query; it’s a window into the economic health, social equity, and financial resilience of a nation. Poverty, in its simplest definition, represents a state where individuals or households lack the financial resources to afford a minimum standard of living. However, delving deeper reveals a complex tapestry woven from economic indicators, social safety nets, systemic challenges, and individual financial realities. Understanding this percentage, its fluctuations, and the demographics it affects is crucial for policymakers, economists, and every citizen striving for a more equitable society.

Annually, the U.S. Census Bureau releases comprehensive data on poverty, providing the official figures that shape public discourse and policy. While the numbers offer a critical snapshot, they also spark ongoing debates about the adequacy of the official poverty measure itself. This article will explore the current landscape of poverty in America, delve into the methodologies used to measure it, examine the underlying causes and profound impacts, and discuss pathways toward greater financial stability for all.

Defining Poverty: More Than Just a Number

To grasp the reality of poverty in America, one must first understand how it is defined and measured. The official poverty line is a threshold set by the U.S. government, intended to delineate who is considered poor. However, this definition is far from universally accepted as a comprehensive gauge of financial hardship.

The Official Poverty Measure (OPM)

The Official Poverty Measure (OPM) was developed in the 1960s based on a formula derived by Mollie Orshansky of the Social Security Administration. Her methodology calculated the cost of a minimum adequate diet and multiplied it by three, based on the observation that food then constituted approximately one-third of a family’s budget. This initial threshold is adjusted annually for inflation using the Consumer Price Index (CPI). The poverty thresholds vary by family size and composition but are not adjusted for geographic differences in the cost of living. For instance, in 2022, the poverty threshold for a single individual under 65 was $14,580, while for a family of four with two children, it was $29,690. A household is considered to be in poverty if its pre-tax cash income falls below the applicable threshold.

Limitations and Criticisms of the OPM

While the OPM provides a consistent historical series, it faces significant criticism for its outdated methodology. Critics argue that multiplying a food budget by three is no longer reflective of modern household spending patterns, where housing, healthcare, transportation, and childcare often consume a much larger portion of income. Furthermore, the OPM only considers pre-tax cash income and does not account for non-cash benefits (like SNAP, housing subsidies, or Medicaid) or necessary expenses such as taxes, work expenses, or out-of-pocket medical spending. Its failure to adjust for variations in the cost of living across different regions of the country is another major flaw, meaning that an income considered adequate in a low-cost rural area might be entirely insufficient in a high-cost urban center.

Alternative Measures: Supplemental Poverty Measure (SPM)

Recognizing the limitations of the OPM, the U.S. Census Bureau developed the Supplemental Poverty Measure (SPM) in 2011. The SPM offers a more nuanced picture by taking into account a broader range of resources and expenses. It includes cash income, non-cash benefits (like food stamps, housing subsidies, and tax credits), and subtracts necessary expenses such as taxes, work expenses (including childcare), out-of-pocket medical expenses, and child support paid. Crucially, the SPM also adjusts for geographic differences in housing costs. The SPM thresholds are based on a percentage of spending on food, clothing, shelter, and utilities (FCSU) rather than just food, plus a small amount for other necessary expenses. While the OPM remains the official statistic for historical comparisons, the SPM is increasingly viewed as a more accurate reflection of contemporary economic hardship, often yielding different poverty rates and demographic distributions.

The Current Landscape: Snapshot of Poverty in America

Understanding the precise percentage of Americans below the poverty line requires examining the latest data and trends, acknowledging that these figures can fluctuate due to economic cycles, policy changes, and global events.

Recent Poverty Statistics and Trends

According to the U.S. Census Bureau’s most recent data (typically released in September for the prior calendar year), the official poverty rate in the United States often hovers around 10-12%. For instance, the 2022 data indicated an official poverty rate of 11.5%, which represented 37.9 million people. This figure was not statistically different from the 11.6% rate in 2021. However, the Supplemental Poverty Measure (SPM) tells a different story. The SPM rate increased significantly from 7.8% in 2021 to 12.4% in 2022, primarily due to the expiration of temporary pandemic-era government assistance programs, such as the expanded Child Tax Credit. This sharp increase highlights the profound impact of social safety nets on alleviating poverty. While the OPM showed little change, the SPM reflected a significant rise in hardship once these critical supports were removed. This disparity underscores why both measures are essential for a comprehensive understanding.

Demographic Disparities in Poverty

Poverty is not evenly distributed across the American population; certain demographic groups experience significantly higher rates.

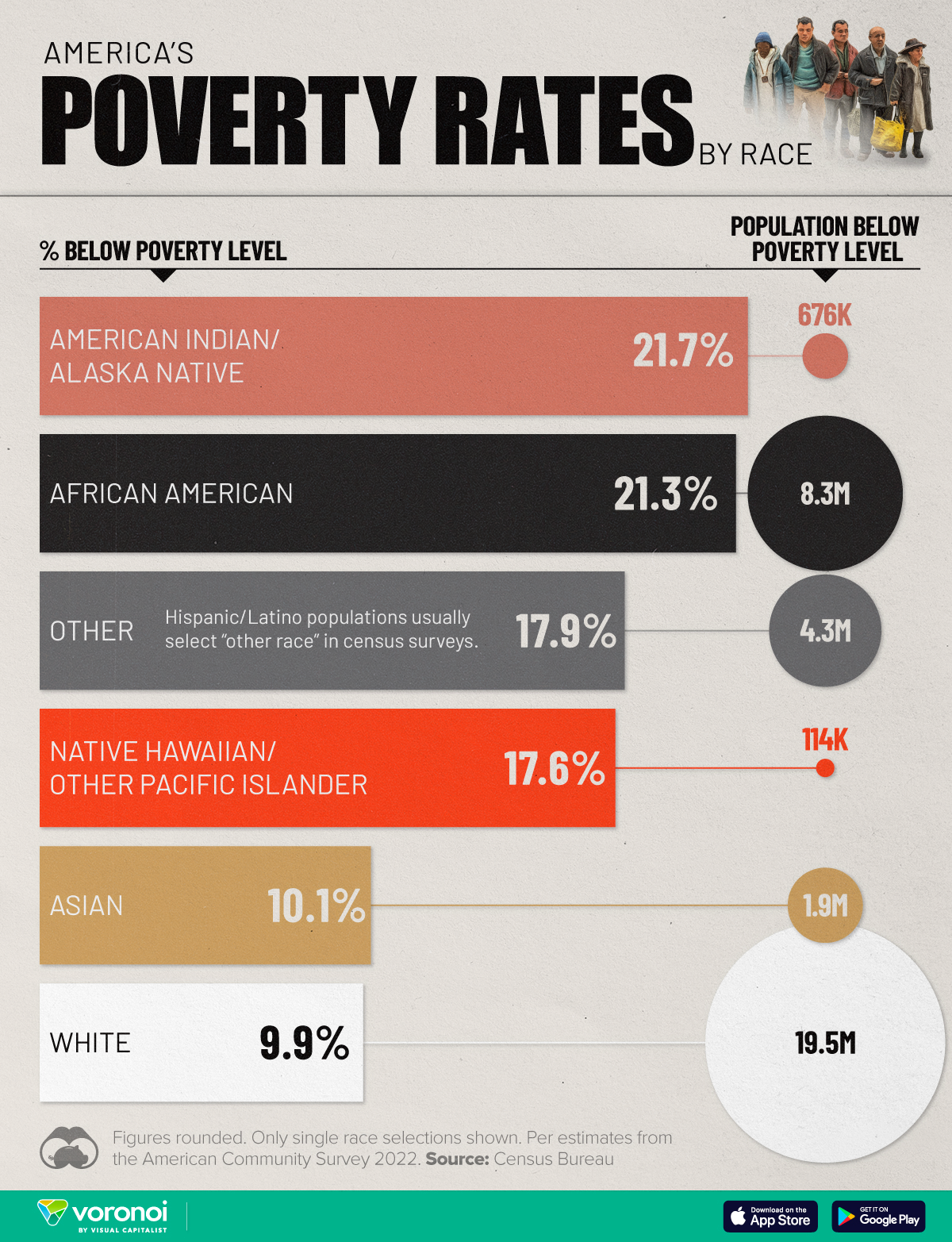

- Race and Ethnicity: Black individuals and Hispanic individuals consistently face higher poverty rates than White, non-Hispanic individuals and Asian individuals. In 2022, the official poverty rate was 17.1% for Black individuals and 17.0% for Hispanic individuals, compared to 7.3% for White, non-Hispanic individuals and 7.2% for Asian individuals. These disparities often reflect historical inequities, systemic barriers, and ongoing challenges in access to education, employment, and wealth-building opportunities.

- Age: Children disproportionately experience poverty. In 2022, the official poverty rate for individuals under 18 was 15.0%, higher than for working-age adults (10.5%) or seniors (10.9%). The SPM often shows a larger effect for children due to the impact of government programs like the Child Tax Credit.

- Family Structure: Families headed by single mothers face the highest poverty rates, significantly higher than married-couple families. This reflects the challenges of balancing work and childcare with a single income.

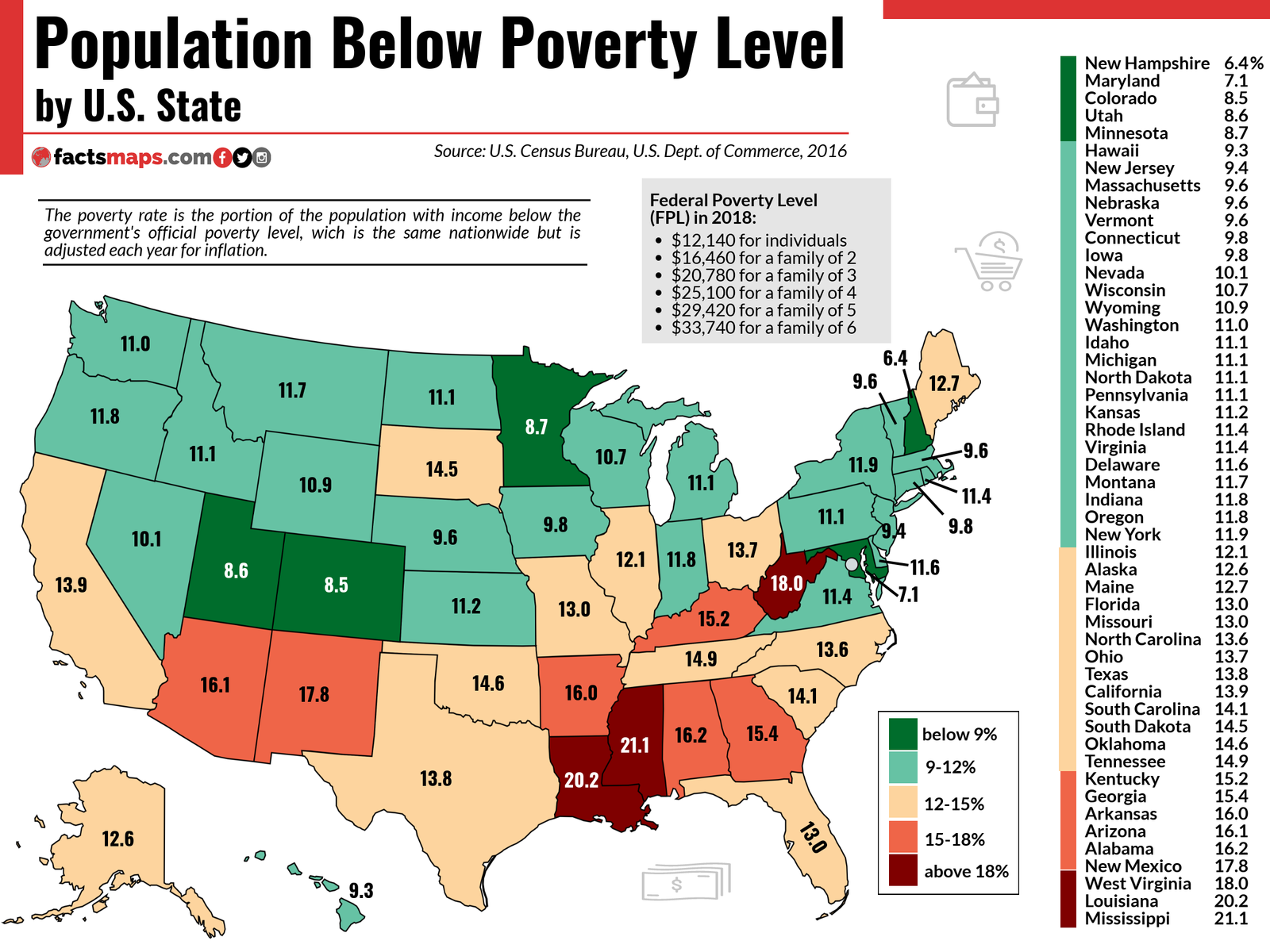

- Geography: Poverty rates vary by region, with higher concentrations often found in the South and in rural areas. Urban cores also exhibit pockets of deep poverty, often correlating with limited opportunities and disinvestment.

The “Working Poor” Phenomenon

A critical aspect of the poverty landscape is the “working poor”—individuals who are employed, sometimes even full-time, but whose incomes still fall below the poverty line. This phenomenon highlights that simply having a job is not always a guaranteed pathway out of poverty. Factors contributing to the working poor include low wages (especially minimum wage jobs that do not keep pace with the cost of living), part-time employment, unstable work schedules, and lack of benefits like health insurance or paid leave. These individuals often struggle to cover basic necessities, leading to chronic financial stress and limited opportunities for upward mobility, despite their efforts in the workforce.

Beyond the Statistics: The Multifaceted Causes of Poverty

Understanding the percentage of Americans below the poverty line requires looking beyond the numbers to the underlying causes. Poverty is rarely the result of a single factor; rather, it is a complex interplay of economic, systemic, and individual circumstances that can trap individuals and families in a cycle of financial hardship.

Economic Factors: Wages, Unemployment, Inflation

- Low Wages: A primary driver of poverty, especially for the working poor, is insufficient wages. The federal minimum wage, unchanged for many years, often falls far short of a living wage in many parts of the country. This means that even full-time employment at minimum wage can leave individuals below the poverty line, particularly for households with dependents.

- Unemployment and Underemployment: Lack of consistent employment is a direct path to poverty. Economic downturns, technological displacement, and lack of job skills can lead to unemployment. Underemployment—working fewer hours than desired or in a job that doesn’t utilize one’s skills—also contributes to financial instability.

- Inflation: Rising costs of living, particularly for essential goods and services like housing, food, and energy, can push families into poverty even if their incomes remain constant. When inflation outpaces wage growth, purchasing power erodes, making it harder for low-income households to afford basic necessities.

Systemic Issues: Education, Healthcare, Housing Affordability

- Unequal Access to Quality Education: A lack of access to quality education from early childhood through higher learning limits future earning potential. Disparities in school funding, teacher quality, and educational resources often perpetuate intergenerational poverty, as individuals from disadvantaged backgrounds struggle to acquire the skills needed for well-paying jobs.

- Healthcare Costs: The high cost of healthcare in the U.S. is a significant burden, especially for low-income families. Medical emergencies, chronic illnesses, and lack of adequate health insurance can lead to catastrophic medical debt, pushing families below the poverty line or preventing them from escaping it. Even with insurance, co-pays, deductibles, and prescription costs can be prohibitive.

- Housing Affordability Crisis: Rents and home prices have soared in many parts of the country, far outstripping wage growth. The lack of affordable housing forces many low-income families to spend a disproportionate amount of their income on shelter, leaving little for food, healthcare, transportation, or savings. This housing burden is a critical factor in the supplemental poverty measure and a major contributor to financial precarity.

Individual Circumstances: Health Shocks, Family Structure Changes

- Health Shocks and Disabilities: Unexpected illness, injury, or the onset of aability can severely impact an individual’s ability to work, leading to lost income and mounting medical bills. For those without adequate savings or insurance, a single health crisis can be financially devastating.

- Family Structure Changes: Events such as divorce, the death of a primary earner, or becoming a single parent can drastically alter a household’s financial stability. Single-parent households, particularly those headed by women, face unique challenges in balancing work and childcare responsibilities, often leading to reduced income and increased expenses.

- Lack of Financial Literacy and Savings: While not a root cause, a lack of financial literacy can exacerbate poverty by making it difficult for individuals to manage their money effectively, save for emergencies, or invest for the future. Without an emergency fund, unexpected expenses can quickly lead to debt and financial crises.

The Ripple Effect: How Poverty Impacts Individuals and the Economy

The presence of a significant portion of the population below the poverty line has far-reaching consequences that extend beyond individual financial hardship. It creates a ripple effect, impacting health, education, social mobility, and the broader economy, perpetuating cycles of disadvantage.

Personal Financial Strain and Debt

For individuals and families living in poverty, daily life is a constant struggle for financial survival. Every decision is weighed against its immediate cost, often sacrificing long-term well-being for short-term necessities.

- Chronic Stress and Mental Health: The relentless pressure of financial insecurity, worrying about affording food, rent, or medical bills, leads to chronic stress, anxiety, and depression. This constant fight-or-flight mode impairs decision-making and problem-solving abilities, making it even harder to escape poverty.

- Debt Cycle: To cover essential expenses or unexpected emergencies, many impoverished individuals resort to high-interest loans (e.g., payday loans, title loans) or credit card debt. This debt can quickly spiral out of control, consuming a significant portion of their limited income and making financial recovery exceedingly difficult.

- Limited Access to Banking Services: Many low-income individuals are “unbanked” or “underbanked,” meaning they lack access to traditional banking services. This forces them to rely on costly alternatives like check-cashing services, further eroding their already meager resources and making it harder to save or build credit.

Health, Education, and Social Mobility Barriers

Poverty creates significant barriers to accessing fundamental resources that are critical for well-being and upward mobility.

- Health Disparities: Individuals in poverty often experience poorer health outcomes. They may lack access to nutritious food, live in environments with higher pollution or fewer safe spaces for exercise, and face barriers to accessing quality healthcare, including preventative care. Chronic illnesses are more prevalent and often go untreated, leading to reduced productivity and quality of life.

- Educational Attainment: Children growing up in poverty often attend underfunded schools, have fewer educational resources at home, and experience instability that impacts their ability to learn. They may face challenges with nutrition, housing, and healthcare that affect their concentration and attendance, ultimately hindering academic achievement and future career prospects. This perpetuates a cycle where lower educational attainment correlates with lower earning potential.

- Reduced Social Mobility: Poverty significantly limits opportunities for upward social and economic mobility. Without access to education, job training, social networks, and capital, individuals find it challenging to climb the economic ladder. This creates a stratified society where one’s birth circumstances largely dictate future potential, undermining the ideal of equal opportunity.

Broader Economic Implications

The societal costs of poverty are substantial, extending beyond the individuals directly affected to impact the national economy as a whole.

- Decreased Productivity: A population burdened by poverty, poor health, and limited education is less productive. This translates to a less skilled workforce, lower innovation rates, and reduced overall economic output.

- Increased Healthcare and Social Welfare Costs: Poverty places a greater demand on public services, including emergency healthcare, social safety nets (such as unemployment benefits, food assistance, and housing aid), and criminal justice systems. These costs represent a significant drain on public budgets that could otherwise be invested in growth-generating sectors.

- Stifled Consumer Demand: A large segment of the population struggling financially has less disposable income, which dampens consumer demand. This can hinder economic growth, as consumer spending is a major driver of the U.S. economy.

- Social Instability: High levels of poverty and economic inequality can lead to social unrest, increased crime rates, and erosion of social cohesion. Addressing poverty is therefore not just a moral imperative but also a pragmatic necessity for maintaining a stable and prosperous society.

Pathways to Progress: Addressing Poverty and Fostering Financial Resilience

Reducing the percentage of Americans below the poverty line requires a multi-pronged approach that combines robust public policy, accessible financial tools, and community-led initiatives. It’s about building a robust safety net while simultaneously creating ladders of opportunity.

Policy Interventions and Social Safety Nets

Effective government policies play a crucial role in preventing individuals from falling into poverty and helping others climb out.

- Strengthening Social Safety Nets: Programs like the Supplemental Nutrition Assistance Program (SNAP), Medicaid, housing assistance, and unemployment insurance are vital. Expanding eligibility, increasing benefit levels, and ensuring easy access to these programs can significantly reduce the depth and prevalence of poverty, as evidenced by the SPM’s response to pandemic-era relief.

- Living Wage and Minimum Wage Reforms: Advocating for and implementing a living wage that reflects the actual cost of living in different regions can lift many working individuals out of poverty. Regular adjustments to the minimum wage, tied to inflation or regional costs, are essential to prevent the “working poor” phenomenon.

- Accessible Healthcare and Education: Policies that ensure affordable healthcare for all, such as universal healthcare systems or robust subsidies, can eliminate a major cause of medical debt and poverty. Similarly, investing in high-quality, equitable education from early childhood to post-secondary levels, including job training and vocational programs, can equip individuals with the skills needed for better-paying jobs.

- Expanded Tax Credits: Programs like the Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC) provide direct financial support to low- and moderate-income families, reducing child poverty and boosting household incomes. Making these credits fully refundable and expanding their reach can have a profound impact.

Personal Financial Literacy and Empowerment

While systemic changes are critical, empowering individuals with financial knowledge and tools is also essential for building long-term resilience.

- Financial Education Programs: Integrating practical financial literacy into school curricula and offering accessible workshops for adults can equip individuals with skills in budgeting, saving, debt management, and investing. Understanding how to manage money, even small amounts, can make a significant difference.

- Emergency Savings Initiatives: Promoting and facilitating access to emergency savings accounts, potentially through employer-matched programs or innovative financial products, can provide a buffer against unexpected expenses that often push families into debt or poverty.

- Access to Affordable Financial Services: Encouraging the growth of community development financial institutions (CDFIs) and credit unions can provide low-income individuals with fair and affordable banking services, including small loans, checking accounts, and financial counseling, as alternatives to predatory lenders.

Community-Based Solutions and Economic Development

Local initiatives and broader economic strategies are fundamental to creating environments where poverty can be overcome.

- Local Economic Development: Investing in local businesses, job creation programs, and infrastructure in disadvantaged communities can bring jobs and opportunities directly to those who need them most. This includes supporting small businesses, offering job training tailored to local labor market needs, and attracting employers who pay living wages.

- Affordable Housing Solutions: Implementing policies that encourage the development of affordable housing, such as zoning reforms, subsidies for affordable housing projects, and rent control measures, can alleviate the significant housing burden on low-income families.

- Community Support Networks: Strengthening local food banks, shelters, childcare services, and community centers provides immediate relief and crucial support structures for families in crisis. Collaborative efforts between non-profits, local governments, and businesses can build resilient communities.

The percentage of Americans below the poverty line is a dynamic statistic, reflecting both the challenges and the opportunities within the nation’s economic and social fabric. While the official numbers provide a baseline, a deeper understanding requires acknowledging the limitations of these measures, recognizing the disproportionate impact on certain demographics, and addressing the multifaceted causes ranging from low wages to systemic inequities. By fostering a comprehensive approach that combines robust policy interventions, enhanced financial literacy, and strong community support, the United States can work towards reducing poverty, building greater financial resilience, and ensuring a more prosperous and equitable future for all its citizens.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.