In the modern economy, the concept of mobility is shifting from a model of ownership to a model of utility. Whether you are a digital nomad, a professional on a temporary assignment, or someone waiting for a new vehicle delivery, hiring a car for a month is no longer just a travel convenience—it is a significant financial decision. Understanding “how much” it costs to hire a car for thirty days requires looking beyond the sticker price and diving into the nuances of personal finance, cash flow management, and cost-benefit analysis.

This guide explores the financial landscape of long-term car rentals, helping you navigate the costs, identify hidden expenses, and determine if this expenditure aligns with your broader financial goals.

Decoding the Cost Structure of Long-Term Car Rentals

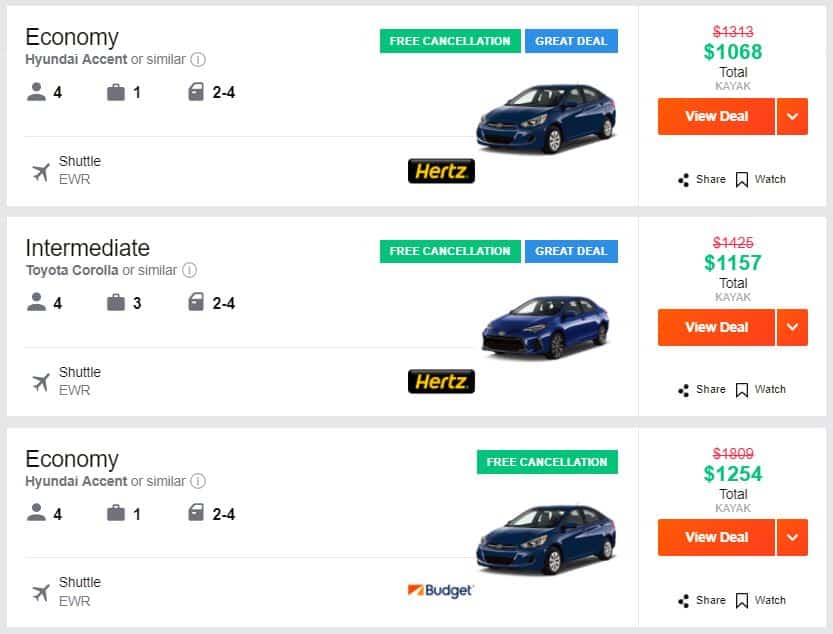

When you look at a daily rental rate, you might see $50 or $80 per day. If you multiply that by thirty, the figure seems astronomical. However, the car rental industry operates on a sliding scale. The longer the commitment, the lower the daily rate becomes.

The Power of the Monthly Discount

Most major rental agencies and peer-to-peer platforms offer significant “long-term” discounts. While a standard mid-size sedan might cost $60 a day for a weekend trip, that same vehicle often drops to $20 or $30 a day when booked for a full month. Financially, this is known as volume pricing. On average, a monthly rental in the current market can range anywhere from $700 to $1,500, depending on the vehicle class, location, and season.

Geographic and Seasonal Volatility

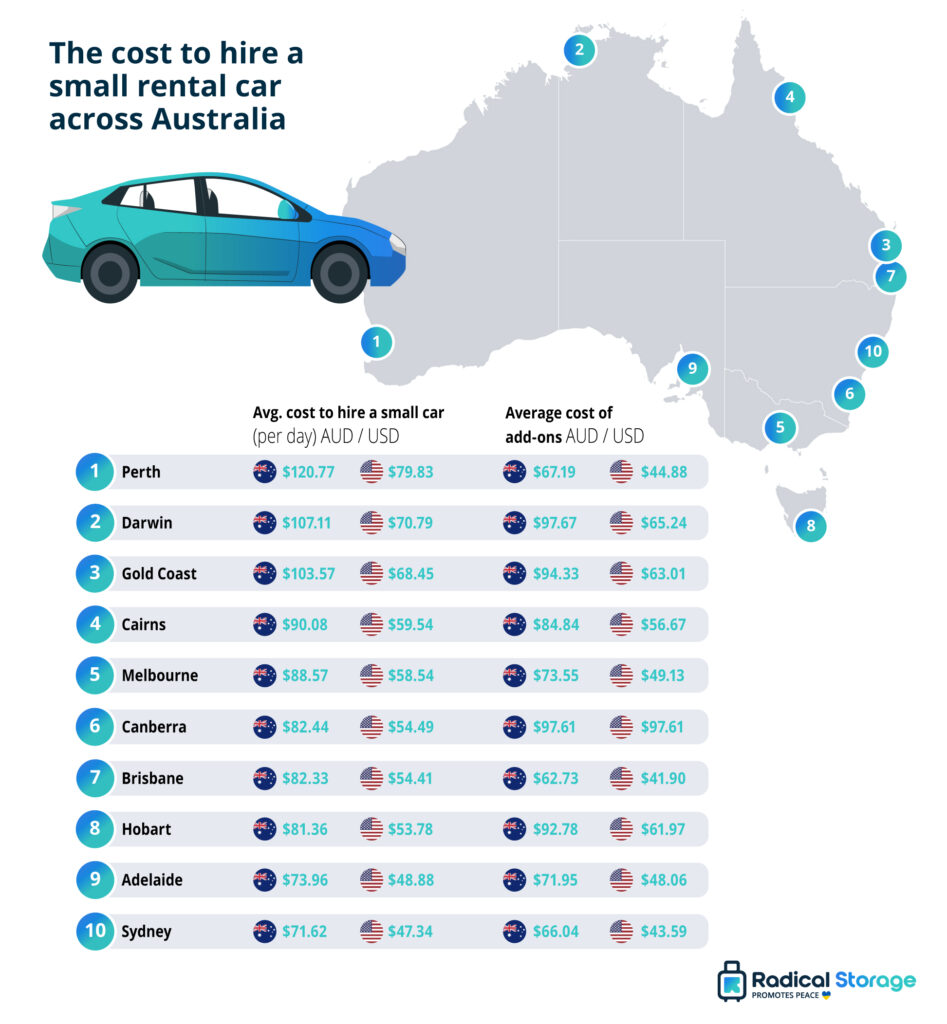

From a personal finance perspective, location is the most significant variable. Hiring a car in a high-demand urban center like New York or London will carry a premium compared to a suburban depot. Furthermore, “surge pricing” applies to months. If your thirty-day rental overlaps with peak holiday seasons or major local events, your costs could rise by 30% to 50%. Planning your rental period to start during “shoulder seasons” is a primary strategy for protecting your monthly budget.

Vehicle Class and Total Cost of Ownership

The “type” of car you choose is a direct lever on your monthly overhead. While an SUV offers comfort, the financial footprint includes not just the higher rental fee but also increased fuel consumption. When calculating your monthly budget, you must categorize the car as a “utility expense.” Choosing an economy or hybrid model can save you hundreds of dollars in fuel costs over a 30-day period, effectively lowering the “true cost” of the rental.

The Economic Comparison: Renting vs. Buying vs. Leasing

To determine if a monthly rental is a sound financial move, one must conduct a comparative analysis against traditional ownership and long-term leasing.

Liquidity and Opportunity Cost

Buying a car requires a significant down payment or a high-interest loan. This ties up your capital in a depreciating asset. Hiring a car for a month, conversely, preserves your liquidity. From an investment standpoint, the $5,000 you save by not making a down payment could be deployed into a high-yield savings account or the stock market. For many, the “convenience premium” of a rental is offset by the interest earned on preserved capital.

Depreciation: The Silent Wealth Killer

New cars can lose 20% of their value in the first year alone. When you hire a car for a month, the rental company bears the brunt of depreciation. You are essentially paying for the “use” of the vehicle without the long-term equity loss. For professionals who only need a vehicle for specific projects, renting is a hedge against the falling value of the automotive market.

Maintenance and Wear-and-Tear

Ownership comes with unpredictable costs: oil changes, new tires, brake pads, and unexpected repairs. A monthly rental fee is inclusive of these maintenance costs. If the engine fails or the transmission slips, it is the rental company’s financial liability, not yours. This predictability is a cornerstone of effective personal budgeting, as it eliminates “emergency” automotive expenses from your monthly ledger.

Identifying and Mitigating Hidden Fees

The quoted “base rate” for a month-long rental is rarely the final number that appears on your credit card statement. To manage your money effectively, you must account for the secondary costs that “leak” from your budget.

The Insurance Trap

Rental companies make a significant portion of their profit from Loss Damage Waivers (LDW) and liability insurance, which can cost $20 to $40 per day. Over a month, this can double your total cost. However, many high-end credit cards offer primary or secondary rental car insurance as a perk. By leveraging your existing financial tools, you can decline the rental company’s insurance and save upwards of $600 a month. Always verify your coverage limits before making this decision.

Mileage Caps and Overages

While many rentals offer “unlimited mileage,” some long-term contracts include a cap (e.g., 3,000 miles per month). Exceeding this limit can result in charges of $0.25 to $0.50 per mile. If you are planning a cross-country trek, these fees can decimate your budget. Mathematically, it is often cheaper to pay a slightly higher base rate for a truly unlimited plan than to risk overage fees.

Taxes, Surcharges, and Concession Fees

If you pick up your car at an airport, you will likely pay a “Concession Recovery Fee” and various tourism taxes. These can add 15% to 25% to your bill. A savvy financial move is to take a short rideshare to an off-airport rental location. The savings on a 30-day contract often far outweigh the $30 spent on a taxi to reach a suburban rental office.

Tax Strategies and Business Finance Considerations

For entrepreneurs, freelancers, and corporate employees, the cost of a monthly car rental isn’t just an expense—it’s a potential tax advantage.

Deductibility for Business Use

If you are hiring a car for business purposes, the entire cost of the rental—including fuel and tolls—may be tax-deductible. Unlike a personal vehicle where you might choose between the standard mileage rate and actual expenses, a rental car used 100% for business allows for a direct deduction of the rental invoice. This can significantly lower your taxable income at the end of the fiscal year.

Section 179 vs. Operational Expense

While purchasing a heavy SUV for a business might allow for a Section 179 “bonus depreciation” deduction, renting is treated as an operational expense (OpEx). For startups or small businesses looking to keep their balance sheets lean, OpEx is often preferable to CapEx (Capital Expenditure) because it doesn’t involve long-term debt or asset management. It provides the flexibility to scale your fleet up or down month-by-month based on revenue.

The Gig Economy and ROI

Many individuals hire cars for a month to participate in ride-sharing or delivery services. In this scenario, the rental cost must be viewed through the lens of Return on Investment (ROI). If the rental costs $1,000 a month and you generate $4,000 in revenue, your gross margin is $3,000. It is vital to track every mile and every dollar to ensure the rental isn’t “eating” your profits. Specialized “Rent-to-Drive” programs often exist for these niches, providing better insurance structures for commercial use.

Strategic Ways to Maximize Your Monthly Rental ROI

To get the most value out of your money, you must treat car hiring like any other major financial transaction: with research and strategy.

Leveraging Loyalty Programs and Credit Card Points

Most major rental brands (Hertz, Enterprise, Avis) have loyalty programs that offer free rental days after a certain number of points are earned. A one-month rental can often earn you enough points for several free weekend rentals in the future. Furthermore, booking through a travel portal (like Chase Ultimate Rewards or Amex Travel) can allow you to use points to cover the cost, preserving your cash for other investments.

The “Subscription” Alternative

In recent years, “Car Subscriptions” have emerged as a middle ground between renting and leasing. Companies like Sixt+ or Finn offer monthly subscriptions that include insurance, maintenance, and roadside assistance in one flat fee. From a financial management perspective, these are often more transparent and easier to budget for than traditional rentals, though they may require a “start-up fee.”

Negotiating Directly with Local Branches

While online booking engines provide a baseline, calling a local rental branch directly can sometimes yield a better “manager’s rate” for a 30-day commitment. Rental managers are often incentivized to keep their fleet utilized. A car sitting on the lot earns zero revenue; a car rented for a month at a discounted rate provides guaranteed cash flow for the branch. Don’t be afraid to ask for a “long-term corporate rate,” even if you are an individual.

Final Summary: Is it Worth It?

Determining how much to hire a car for a month is a calculation that involves more than just a daily rate. It is an assessment of liquidity, risk mitigation, and tax efficiency.

For the average consumer, a monthly rental will likely cost between $800 and $1,200 all-in. While this may seem higher than a monthly car loan payment, it frees you from the burdens of long-term debt, interest payments, maintenance costs, and the inevitable sting of depreciation.

If you value financial flexibility and want to avoid the “sunk cost” of vehicle ownership, hiring a car for a month can be a brilliant move for your personal balance sheet. By utilizing credit card insurance, avoiding airport locations, and choosing fuel-efficient models, you can turn a major expense into a controlled, predictable, and strategically sound financial decision.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.