In the complex landscape of healthcare management and personal finance, few topics are as emotionally charged or financially significant as end-of-life and chronic illness care. For families and individuals mapping out their long-term financial strategies, understanding the distinction between palliative and hospice care is not just a matter of medical preference; it is a critical fiscal decision. While both provide comfort and support for patients facing serious illnesses, they operate under vastly different billing structures, insurance reimbursement models, and eligibility requirements.

Navigating these differences requires a keen understanding of how the American healthcare system—specifically Medicare, Medicaid, and private insurance—allocates funds. From a financial perspective, the choice between palliative and hospice care can mean the difference between maintaining a steady household budget and facing catastrophic out-of-pocket expenses. This article delves into the economic realities of these two care paths, providing the insight necessary to make informed financial decisions during challenging times.

1. Understanding the Billing Models: Insurance, Medicare, and Out-of-Pocket Costs

The primary financial differentiator between palliative and hospice care lies in how the services are billed and who pays for them. To the uninitiated, these services might appear similar, but the backend financial machinery is remarkably different.

The Medicare Hospice Benefit: An All-Inclusive Model

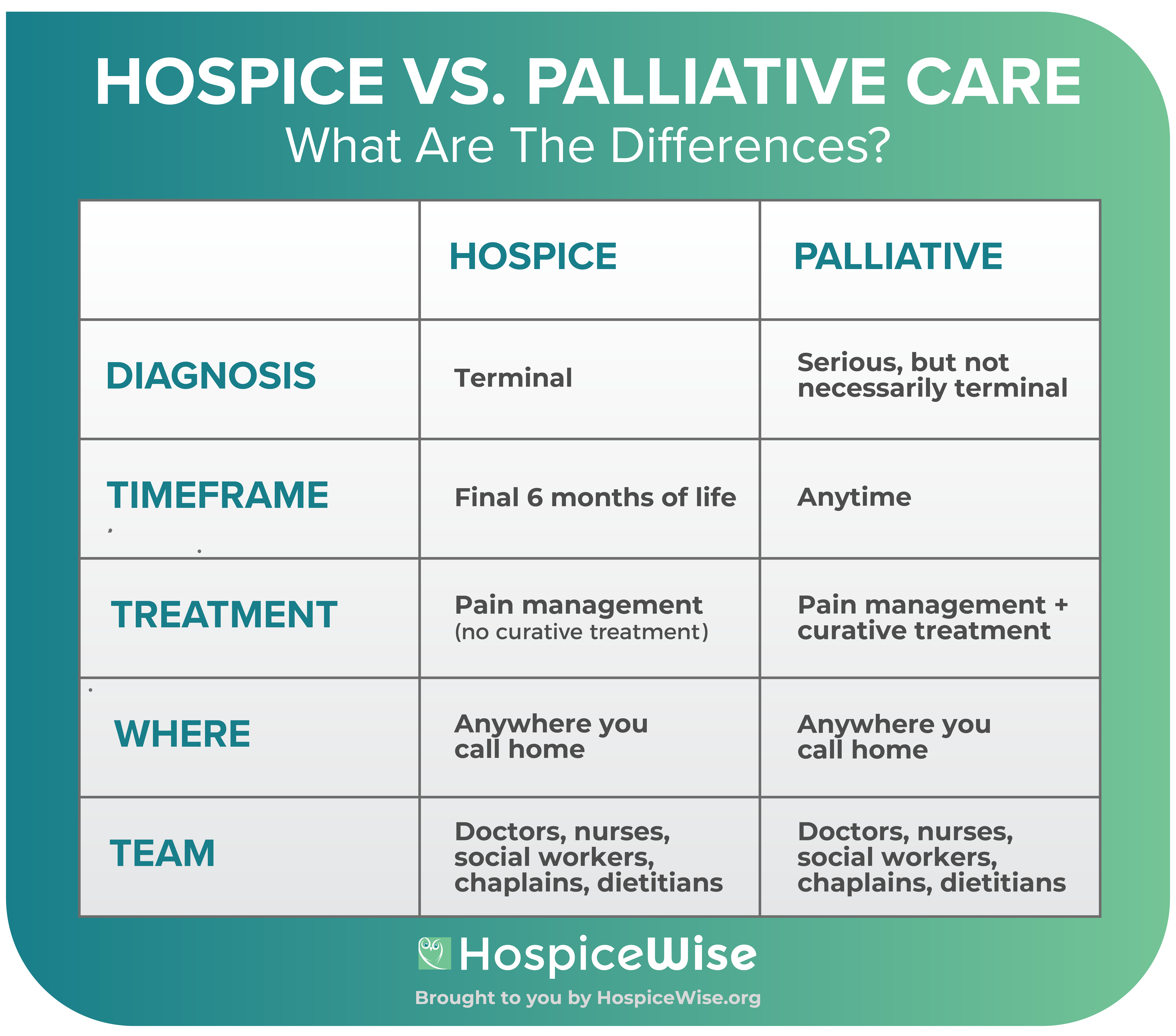

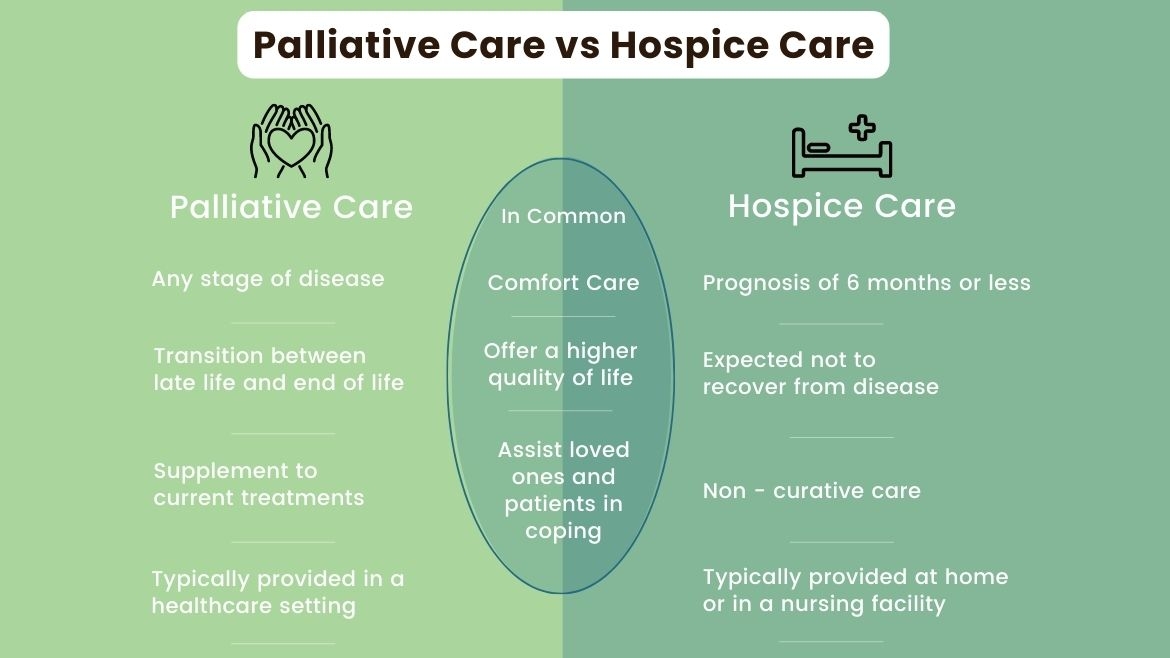

Hospice care is primarily funded through the Medicare Hospice Benefit. From a financial planning standpoint, hospice is one of the most comprehensive benefits offered by the federal government. When a patient elects the hospice benefit, they waive their right to traditional Medicare coverage for their terminal illness, opting instead for a per-diem payment system.

Under this model, Medicare pays the hospice provider a flat daily rate. This rate covers almost everything related to the terminal diagnosis: professional services (doctors, nurses, social workers), medications for symptom management, medical equipment (hospital beds, oxygen), and supplies. For the family, this often results in zero out-of-pocket costs for medications or equipment related to the illness, representing a significant financial relief during a period of high medical volatility.

Palliative Care: The Managed Care and Fee-for-Service Model

Unlike hospice, palliative care is not a consolidated benefit. Financially, it is treated like any other medical specialty, such as cardiology or oncology. Palliative care services are billed under Medicare Part B or private insurance as fee-for-service visits.

For a patient, this means that while the “consultation” with a palliative specialist might be covered, the associated costs—such as the medications they prescribe, the physical therapy they recommend, or the medical equipment they order—are subject to the patient’s standard insurance deductibles, co-pays, and coinsurance. For a family managing a chronic but not yet terminal illness, palliative care can be an expensive ongoing cost center rather than a packaged financial solution.

2. Financial Eligibility and Timelines: When Does the Money Flow?

The timing of care transition is a pivotal factor in financial forecasting. The “trigger” for when insurance shifts from standard curative coverage to end-of-life benefits is defined by specific clinical and financial milestones.

The Six-Month Rule and Financial Planning

To qualify for the financial protections of hospice, a physician must certify that the patient has a life expectancy of six months or less if the disease runs its normal course. This “six-month rule” acts as a gatekeeper for federal funding. From a wealth management perspective, entering hospice early (at the beginning of that six-month window) can preserve family assets by shifting the burden of expensive medication and equipment costs to the Medicare Hospice Benefit.

However, many families wait until the final days of life to engage hospice, meaning they have spent months or years paying high co-pays for palliative or curative treatments that could have been avoided had they transitioned sooner. Understanding the “break-even” point of when hospice becomes more financially advantageous than palliative care is a core component of medical financial advocacy.

Curative vs. Non-Curative Costs: Where Your Budget Goes

A major financial distinction involves “curative intent.” Palliative care allows for concurrent curative treatment. A patient can receive chemotherapy (a massive financial expense) while also seeing a palliative team to manage the side effects. The financial burden here remains high because the expensive curative treatments continue.

In hospice, the financial agreement is built on the cessation of curative treatments. Once a patient enters hospice, the insurance will no longer pay for expensive treatments aimed at “curing” the disease, such as aggressive radiation or experimental drugs. While this sounds like a medical choice, it is also a massive financial pivot. By forgoing curative treatments that have a low probability of success, families stop the “money pit” of high-cost interventions and move toward a fixed-cost, fully covered comfort model.

3. The Business Side of End-of-Life Care: Investment and Market Trends

The hospice and palliative care sectors have become significant players in the broader healthcare economy. For those looking at the “Money” niche, understanding the corporate structure of these services reveals why certain care paths are marketed more aggressively than others.

The Rise of For-Profit Hospice Chains

In the last two decades, the hospice industry has seen a massive influx of private equity and corporate investment. Once a predominantly non-profit sector, for-profit hospice providers now make up a significant portion of the market. These entities operate on a high-margin business model because the Medicare per-diem rate is fixed. If a provider can deliver care efficiently, the “spread” between the Medicare payment and the cost of care becomes profit.

This corporatization has financial implications for consumers. For-profit entities may be more aggressive in enrolling patients who are earlier in their six-month window to ensure a longer duration of per-diem payments. Investors see the hospice sector as a “recession-proof” asset class, driven by the aging Baby Boomer demographic.

How Consolidation Impacts Cost and Quality

The consolidation of palliative and hospice providers under large corporate umbrellas has led to standardized billing practices but also less flexibility for patients. When a large healthcare system owns both the hospital and the hospice agency, the “financial leak” is minimized—the patient stays within the system from diagnosis to death.

For the savvy consumer or financial planner, it is essential to realize that the “referral” from a doctor to a specific hospice might be driven by corporate alignment rather than the best financial or clinical outcome. Comparing the fee structures of independent palliative clinics versus hospital-based systems can often reveal hidden administrative fees or higher co-pay requirements.

4. Strategic Financial Planning for Families and Caregivers

The transition to palliative or hospice care should be viewed through the lens of asset protection and long-term financial viability for the surviving family members.

Asset Protection and Long-Term Care Insurance

Long-term care insurance (LTCI) policies often treat palliative and hospice care differently. Some older policies may only pay out if the patient is in a facility, whereas many palliative and hospice services are delivered at home.

Financial advisors recommend a thorough “audit” of insurance policies before a crisis hits. Does the policy cover “in-home palliative support”? Does it offer a “death benefit” or “accelerated benefit” that can be used to pay for the 24/7 caregiving that hospice does not cover? (It is a common financial misconception that hospice provides 24/7 bedside nursing; it generally does not, leaving the family to either provide the labor themselves or hire private-duty nurses at a significant hourly rate.)

Managing the Indirect Costs of Home Care

While hospice may cover the “medical” bills, the “living” bills often escalate. When a patient chooses home-based palliative or hospice care, the indirect costs—electricity for oxygen concentrators, specialized nutritional supplements not covered by Medicare, and the “lost wages” of family caregivers—can be staggering.

From a business finance perspective, caregiving is unpaid labor that has a massive “opportunity cost.” For a high-earning professional to leave their job to provide hospice care for a parent is a major financial hit to the family’s net worth. Strategic planning involves calculating whether it is more cost-effective to pay for private-duty nursing (tax-deductible in some cases as a medical expense) or for a family member to take a leave of absence under the Family and Medical Leave Act (FMLA), which is usually unpaid.

Conclusion: The Bottom Line of Care

The difference between palliative and hospice care is as much about the ledger as it is about the bedside. Palliative care is a flexible, albeit more expensive, “pay-as-you-go” model that allows for continued curative attempts. Hospice care is a “bundled” financial benefit designed to provide total coverage in exchange for a shift in medical goals.

By understanding these financial levers—reimbursement models, the six-month rule, and the corporate landscape of the care industry—individuals can protect their wealth while ensuring they or their loved ones receive the appropriate level of support. In the intersection of health and money, being informed is the best way to ensure that a medical journey doesn’t become a financial catastrophe.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.