In the world of finance, precision is not merely a preference; it is a requirement. Whether you are calculating the interest on a high-yield savings account, determining the dividend yield of a blue-chip stock, or evaluating the capitalization rate of a commercial real estate property, the ability to pivot between fractions and decimals is a fundamental skill. A common question that arises in both basic mathematics and complex financial modeling is the conversion of mixed numbers. Specifically, what is 5 3/5 as a decimal?

While the mathematical answer is a straightforward 5.6, the implications of that number within the context of personal finance and investing are profound. Understanding how to arrive at this figure and how it scales across large-scale portfolios is the difference between an amateur investor and a financially literate strategist.

The Fundamentals of Numerical Conversion in Personal Finance

Before diving into complex market analysis, one must master the basic arithmetic that governs money. Fractions are often used in legacy financial systems—such as the way stock prices were quoted in eighths and sixteenths on the New York Stock Exchange until the early 2000s. However, the modern era belongs to the decimal.

Breaking Down 5 3/5 into a Decimal Format

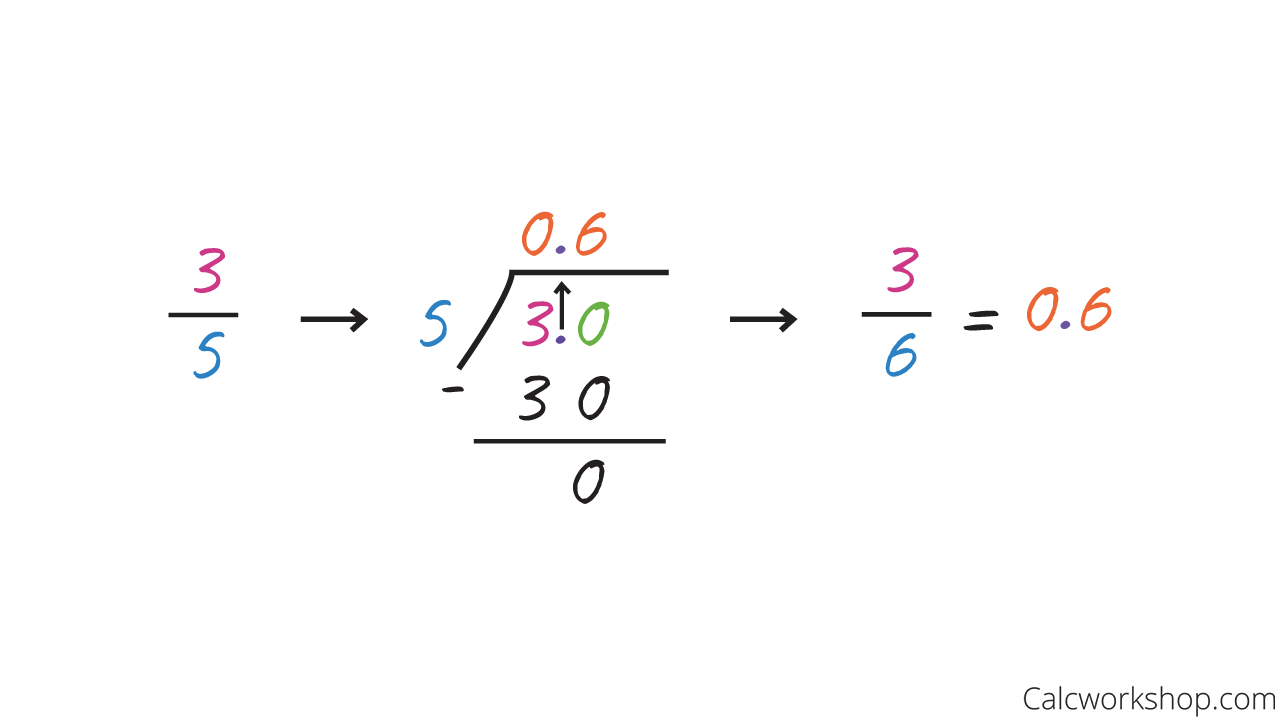

To convert the mixed number 5 3/5 into a decimal, we must separate the whole number from the fraction. The whole number remains 5. The fractional component, 3/5, represents three parts of a five-part whole. In decimal terms, we divide the numerator (3) by the denominator (5).

3 ÷ 5 = 0.6

When we combine the whole number with our new decimal, we get 5.6. In a financial context, this 5.6 could represent a 5.6% interest rate, a 5.6x price-to-earnings ratio, or a 5.6% increase in quarterly revenue. Without the ability to quickly convert 3/5 into 0.6, a financial analyst might struggle to input data into the digital tools that drive modern wealth creation.

Why Decimals are the Language of Modern Banking

The shift from fractions to decimals in the financial world—a process known as “decimalization”—was designed to make markets more transparent and accessible. When a bank offers a loan at 5 3/5%, they are legally obligated to represent that as 5.6% in most disclosure documents (the Annual Percentage Rate, or APR).

Decimals allow for much tighter “spreads” in trading. In the fractional era, the minimum price movement (tick size) might have been 1/8 of a dollar (12.5 cents). With decimals, we can track movements down to the penny or even the “pip” in foreign exchange markets. Converting 5 3/5 to 5.6 allows investors to compare that rate against a competitor’s 5.55% or 5.65% with immediate clarity.

Calculating Returns and Yields with Precision

In the realm of investing, small numbers lead to massive outcomes over time. The difference between 5% and 5.6% might seem negligible on a one-hundred-dollar investment, but when scaled to a retirement portfolio or a corporate balance sheet, that 0.6 (the 3/5) becomes a significant sum of money.

The Difference Between 5.6% and 5.625%: Why it Matters

In the bond market or when calculating mortgage-backed securities, precision often extends to three or four decimal places. While 5 3/5 is exactly 5.6, an investor might encounter a rate of 5 5/8, which is 5.625.

On a $1,000,000 commercial loan, the difference between 5.6% and 5.625% is $250 in interest per year. Over a 30-year amortization schedule, this small decimal variance results in thousands of dollars in extra costs. Financial literacy involves recognizing that the decimal 5.6 is a specific point on a continuum, and being able to calculate it accurately ensures that you are not overpaying for capital or underestimating your returns.

Compound Interest and the Power of Small Decimal Variations

The magic of compound interest relies entirely on the rate (r) in the formula $A = P(1 + r/n)^{nt}$. If your annual return is 5 3/5%, your “r” value is 0.056.

Consider an initial investment of $10,000 held for 20 years.

- At 5%, the ending balance is approximately $26,532.

- At 5.6% (5 3/5), the ending balance is approximately $29,735.

By understanding that 3/5 adds an extra 0.6 to your percentage, you realize that this “small” fraction resulted in an additional $3,203 in wealth. This illustrates why savvy investors obsess over decimal points in expense ratios and management fees.

Applying Fractional Knowledge to Investment Portfolios

Beyond simple interest rates, decimals are used to track ownership and asset value. As fintech platforms evolve, the lines between whole units and fractions continue to blur.

Dividend Yields and Fractional Shares

Modern brokerage apps now allow for “fractional share” investing. In the past, if a stock cost $1,000, you needed $1,000 to participate. Today, if you have $5,600, you can buy exactly 5.6 shares of that company.

Understanding that you own 5 3/5 shares is vital for calculating your dividend income. If the company pays a dividend of $2.00 per share, your calculation is 5.6 x 2 = $11.20. When your portfolio grows to include hundreds of different assets, your ability to think in decimals allows you to aggregate your projected cash flow more efficiently than using cumbersome fractions.

Real Estate Cap Rates: Moving Beyond Round Numbers

In real estate, the Capitalization Rate (Cap Rate) is the ratio of Net Operating Income (NOI) to the property asset value. A property might be listed with a Cap Rate of 5 3/5%. An investor looking at this would immediately convert this to 5.6% to compare it against the “risk-free rate” (usually the 10-year Treasury yield).

If the Treasury is yielding 4.2%, and the property is yielding 5.6%, the “risk premium” is 1.4%. This decimal-based comparison allows the investor to decide if the extra work of managing a property is worth the 1.4% spread. Without converting 5 3/5 into its decimal counterpart, the comparison is less intuitive and prone to error.

Digital Tools and Financial Calculators

While mental math is a valuable skill, professional financial management relies on software. However, software is only as good as the data entered into it.

Using Spreadsheets to Automate Fractional Conversions

In programs like Microsoft Excel or Google Sheets, entering “5 3/5” can sometimes lead to formatting errors where the software interprets the entry as a date (e.g., May 3rd). To build a robust financial model, an analyst must enter the decimal equivalent: 5.6.

Using the formula =5+(3/5) in a cell ensures that the spreadsheet recognizes the value as a number. This allows for the automation of “what-if” scenarios. For instance, if you are a business owner calculating the cost of goods sold (COGS) and your raw material price increases by 5 3/5%, your spreadsheet model needs that 5.6 factor to accurately predict your new profit margins.

Avoiding Costly Errors in Business Financial Modeling

In corporate finance, “rounding errors” can lead to significant discrepancies in year-end audits. If a business records a 5.6% growth rate but rounded it down from 5 3/5 to 5.5% for simplicity, they are under-reporting their performance. Conversely, rounding up to 6% could mislead stakeholders.

Accuracy in converting fractions like 3/5 to .6 ensures that the financial narrative of the company is honest and data-driven. It builds trust with investors, lenders, and regulatory bodies who require exact figures rather than approximations.

The Psychological Edge of Numerical Literacy

Finally, there is a psychological component to understanding numbers. In personal finance, the “math-anxious” are often the most vulnerable to predatory lending or poor investment choices.

Understanding Market Volatility through Decimals

When the stock market drops by 5 3/5%, seeing it as a 5.6% decline helps put it in perspective. It is more than a 5% “correction” but less than a 10% “bear market” move. Being able to quantify volatility with decimal precision allows an investor to remain calm. They can look at historical data and see that 5.6% fluctuations are a standard part of market cycles, helping them avoid “panic selling.”

Building a Data-Driven Wealth Mindset

Wealth is built through the accumulation of small wins. A 5 3/5% return on a side hustle, a 5.6% savings on tax through efficient planning, and a 5.6% reduction in household expenses all compound.

When you stop seeing “5 3/5” as a confusing school math problem and start seeing it as “5.6”—a modular, usable piece of financial data—you take control of your economic life. You move from being a passive consumer of financial products to an active manager of your capital.

In conclusion, while the question “what is 5 3/5 as a decimal?” has a simple answer—5.6—the application of that answer spans the entire spectrum of money management. From the micro-level of personal savings to the macro-level of global investment strategies, the transition from fractions to decimals represents the transition from guesswork to precision. In the pursuit of financial independence, every decimal point counts.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.