Deciding when to claim Social Security benefits is one of the most critical financial decisions an individual will make in their lifetime. For many, the allure of age 62—the earliest possible age to claim retirement benefits—is strong. It represents the first opportunity to tap into a lifelong investment and transition away from the daily grind. However, the decision to claim early is not merely a matter of timing; it is a complex financial calculation that involves understanding permanent reductions, actuarial adjustments, and long-term cash flow strategies.

To answer the question “How much will I get?” one must look beyond a simple dollar figure and examine the mechanics of the Social Security Administration (SSA) formulas and how they interact with your personal financial profile.

The Mechanics of Your Benefit: How the SSA Calculates Your Payment

Before determining the specific amount you will receive at age 62, it is essential to understand the foundation upon which your benefit is built. The SSA does not simply look at your last few years of work; it looks at your entire career through a specific lens.

The Role of Average Indexed Monthly Earnings (AIME)

Your benefit is based on your “Average Indexed Monthly Earnings” (AIME). To calculate this, the SSA looks at your highest 35 years of earnings. These earnings are “indexed” to account for changes in average wages over time, ensuring that your prior earnings are viewed in today’s economic context. If you have fewer than 35 years of work history, the SSA enters a zero for each missing year, which can significantly drag down your average and, consequently, your monthly check.

The Primary Insurance Amount (PIA) and Bend Points

Once your AIME is established, the SSA applies a formula to determine your Primary Insurance Amount (PIA). This is the amount you would receive if you waited until your Full Retirement Age (FRA). The formula is progressive, meaning it replaces a higher percentage of lower earnings than higher earnings. It uses “bend points”—specific dollar thresholds that change annually—to determine the replacement rate. For the money-conscious retiree, understanding that Social Security is designed as a safety net rather than a full salary replacement is vital for proper retirement planning.

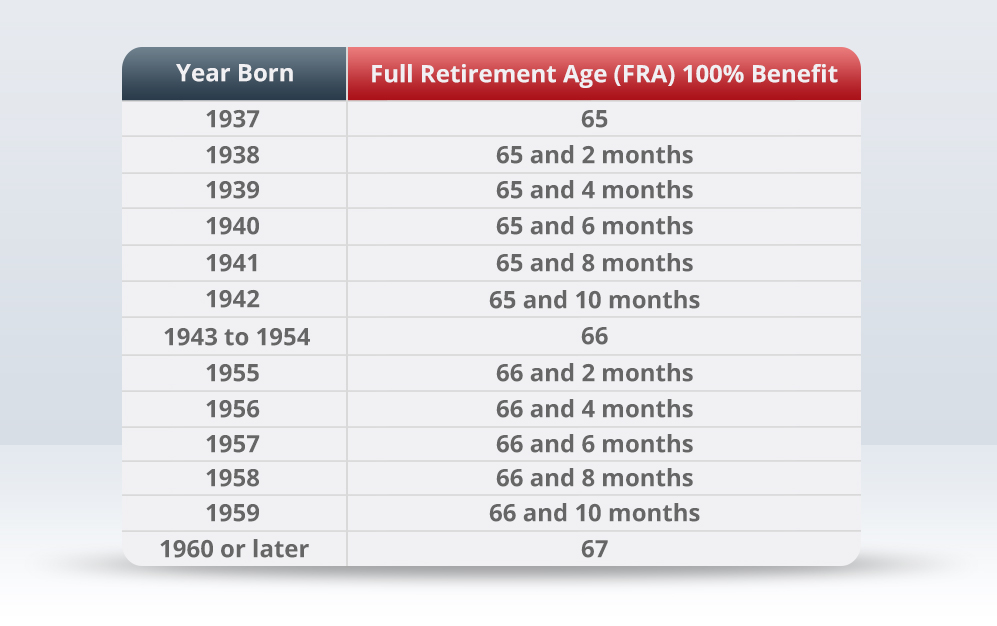

Defining Your Full Retirement Age (FRA)

Your FRA is the age at which you are entitled to 100% of your PIA. For anyone born in 1960 or later, the FRA is 67. If you claim at 62, you are claiming five years early. This “early” status triggers a permanent reduction in your monthly benefit to account for the fact that you will likely receive checks for a longer period of time.

The Financial Penalty of Claiming at Age 62

Claiming at 62 provides immediate liquidity, but it comes at a steep price. The reduction is not a temporary “early bird” fee; it is a permanent adjustment to your base benefit that lasts for the rest of your life.

The Permanent Percentage Reduction

If your Full Retirement Age is 67 and you choose to start benefits at 62, your monthly payment will be reduced by approximately 30%. This reduction is calculated month-by-month: benefits are reduced by 5/9 of 1% for each month before FRA, up to 36 months, and 5/12 of 1% for each additional month. On a $2,000 monthly PIA, claiming at 62 would result in a monthly check of only $1,400. Over a 20-year retirement, this represents a difference of over $140,000, not including the impact on future Cost-of-Living Adjustments (COLAs).

The Impact of the Retirement Earnings Test

A common mistake many retirees make is claiming at 62 while continuing to work a high-paying job or a lucrative side hustle. If you are under your FRA, the SSA applies an “earnings test.” For 2024, if you earn more than $22,320, the SSA will withhold $1 in benefits for every $2 you earn above that limit. While these withheld benefits are eventually added back to your check once you reach FRA, the immediate loss of liquidity can defeat the purpose of claiming early. For those focused on maximizing cash flow, working and claiming early is often the least efficient financial move.

Consequences for Spousal and Survivor Benefits

Your decision to claim at 62 doesn’t just affect you; it can affect your household’s total financial picture. If you are the higher earner, claiming early locks in a lower base for survivor benefits. If you pass away, your spouse is entitled to the higher of their own benefit or yours. By claiming at 62, you are effectively capping the maximum amount your surviving spouse can receive, which could create a financial shortfall in their later years.

Strategic Considerations: When Does 62 Make Sense?

Despite the heavy reductions, there are specific financial scenarios where claiming at 62 is the most logical component of a broader money management strategy.

Health Status and Life Expectancy

Social Security is essentially an insurance product designed to protect against the “risk” of living a long life. If you have significant health concerns or a family history of shorter lifespans, taking the money as early as possible may result in a higher cumulative lifetime benefit. From a strictly financial standpoint, if you do not expect to reach the “break-even point”—usually between ages 77 and 80—claiming at 62 ensures you receive as much from the system as possible.

Immediate Financial Need and Debt Management

For some, the decision is driven by necessity. If you have lost your primary source of income or are facing high-interest debt, the Social Security check at 62 can serve as a vital tool to prevent the depletion of other assets, such as a 401(k) or IRA. Using Social Security to avoid high-interest credit card debt or to prevent a foreclosure is often a more sound financial move than waiting for a higher benefit while your net worth is eroded by interest payments.

The Reinvestment Strategy

Sophisticated investors sometimes claim at 62 even if they don’t “need” the money. The logic here is “opportunity cost.” If you believe you can invest your Social Security checks into a brokerage account or a business venture and achieve a rate of return that outperforms the 8% annual increase you would get by delaying, claiming at 62 might be a tactical move. However, this is risky, as the “return” on waiting for Social Security is guaranteed and inflation-adjusted, whereas market returns are not.

Tools and Resources for Accurate Projections

To know exactly how much you will get, you should move beyond general estimates and look at your specific data provided by the government.

Utilizing the “my Social Security” Account

The most accurate way to determine your benefit is to create an account on the SSA.gov website. Your “Social Security Statement” provides personalized estimates based on your actual earnings history. It will show you your projected monthly amount at 62, at your FRA, and at age 70. This tool is the gold standard for financial planning, as it accounts for your specific years of high and low earnings.

Factoring in Inflation and COLAs

When looking at your projected amount at age 62, remember that this number is usually expressed in today’s dollars. Social Security benefits are adjusted annually via the Cost-of-Living Adjustment (COLA). While the percentage reduction for claiming at 62 is fixed, the dollar amount of your check will likely grow over time. When modeling your retirement income, it is important to include a conservative inflation estimate to see how your purchasing power might hold up over two or three decades.

Calculating Your Break-Even Point

A “break-even” analysis is a calculation used to determine the age at which the total value of higher monthly payments (from waiting) surpasses the total value of smaller monthly payments (from starting early). For most people, if they live past age 78, they would have been better off waiting until 67. If they live past 82, they would have been better off waiting until 70. Understanding your break-even point allows you to treat Social Security as an asset class within your portfolio, making a data-driven decision rather than an emotional one.

Conclusion: Balancing Today’s Needs with Tomorrow’s Security

The question of how much you will get at age 62 is only half of the equation. The other half is determining if that amount is sufficient to support your lifestyle and financial goals. A 30% permanent reduction is a significant trade-off for five years of early access.

For the disciplined financial planner, the decision should be part of a holistic review of all income sources, including pensions, retirement accounts, and personal investments. Whether you choose to claim early to enjoy your youth, reinvest the funds, or out of necessity, doing so with a clear understanding of the math ensures that your “golden years” are built on a stable financial foundation. Social Security is a powerful tool; ensure you are wielding it in a way that maximizes your long-term net worth and provides the security you’ve spent decades working to achieve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.