In the realm of personal and business finance, numbers are the language of progress. However, raw numbers rarely tell the full story. To truly understand the health of an investment, the efficiency of a budget, or the growth of a business, one must master the concept of the percentage. Whether you are calculating the interest on a high-yield savings account, determining the tax implications of a stock sale, or analyzing a corporate balance sheet, knowing how to calculate the percentage is the foundational skill that separates passive observers from informed wealth builders.

This guide provides a comprehensive deep dive into the application of percentages within the financial sector, moving beyond basic arithmetic into strategic financial analysis.

1. The Fundamental Mathematics of Personal Finance

At its core, a percentage is a way to express a number as a fraction of 100. In finance, this allows us to compare disparate figures on an equal playing field. Understanding the basic mechanics of these calculations is the first step toward effective money management.

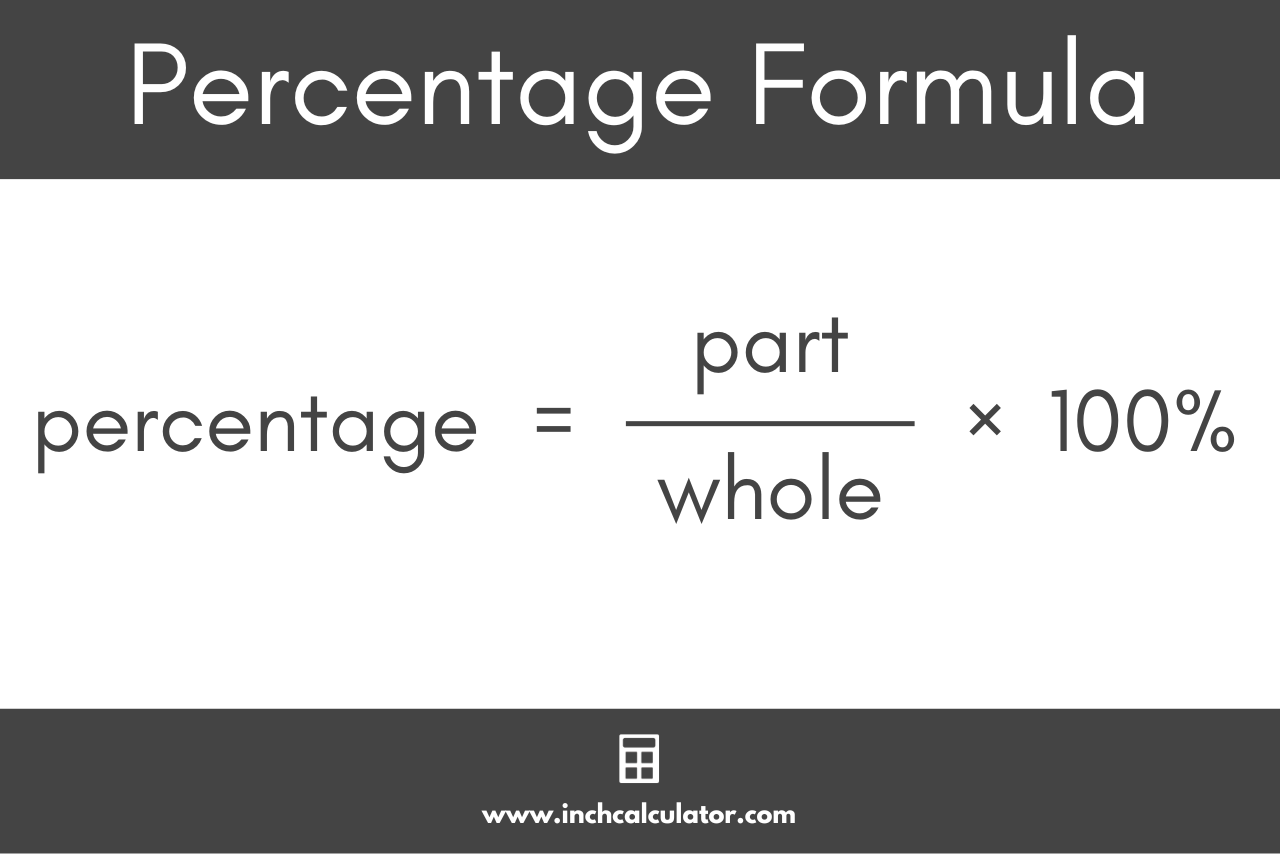

The Standard Percentage Formula

The basic formula for finding a percentage is:

** (Part / Whole) × 100 = Percentage **

In a financial context, this is most commonly used in budgeting. For instance, if your total monthly take-home pay is $5,000 and your rent is $1,500, calculating the percentage of your income spent on housing is vital for fiscal health.

($1,500 / $5,000) × 100 = 30%.

By identifying that 30% of your income goes to rent, you can align your spending with popular financial frameworks like the 50/30/20 rule (50% for needs, 30% for wants, and 20% for savings).

Calculating Percentage Increases for Salary and Savings

Negotiating a raise or tracking the growth of a retirement fund requires an understanding of percentage change. The formula for percentage increase is:

** [(New Value – Old Value) / Old Value] × 100 **

If you received a salary bump from $70,000 to $77,000, your percentage increase is 10%. Understanding this figure is crucial when comparing your income growth against the annual inflation rate. If inflation is at 4% and your raise is 10%, your “real” purchasing power has increased by 6%. Without this calculation, the raw dollar amount may mask the fact that you are barely keeping pace with the rising cost of living.

Discounts and Sales Tax Calculations

For the everyday consumer, calculating percentages is most frequent during transactions. To find the final price of a discounted item, you multiply the original price by the “decimal” version of the percentage (e.g., 20% becomes 0.20).

- Discount: Original Price × Discount Rate = Savings.

- Tax: Original Price × Tax Rate = Tax Amount.

Mastering these quick mental calculations prevents “sticker shock” at the register and allows for more accurate cash flow forecasting.

2. Strategic Percentages in Investing and Wealth Building

In the world of investing, percentages are the primary metric for success. Investors rarely ask “How many dollars did you make?” but rather “What was your percentage return?” This allows for a standardized comparison across different asset classes, such as real estate, stocks, and bonds.

Determining Return on Investment (ROI)

ROI is the ultimate litmus test for any financial endeavor. It measures the efficiency of an investment or compares the efficiencies of several different investments.

** ROI = [(Current Value of Investment – Cost of Investment) / Cost of Investment] × 100 **

Suppose you invested $10,000 in a mutual fund, and a year later, the balance is $11,200. Your ROI is 12%. This percentage allows you to see if your capital is working harder for you in the market than it would be in a standard savings account. High-net-worth individuals use this calculation to decide where to allocate their next dollar of capital.

The Rule of 72 and Compounding Percentages

While simple percentages measure a single point in time, compound interest involves percentages calculated on top of previous percentages. To understand how long it will take for your money to double at a specific percentage rate, professionals use the “Rule of 72.”

** 72 / Annual Interest Rate = Years to Double **

If your portfolio returns an average of 8% annually, your money will double every 9 years (72 / 8 = 9). Understanding this percentage-based shortcut is essential for long-term retirement planning and setting realistic financial expectations.

Portfolio Allocation Percentages

Diversification is the only “free lunch” in finance, and it is managed entirely through percentages. A balanced portfolio might consist of 60% equities, 30% fixed income, and 10% alternative assets. As market values shift, these percentages will drift. “Rebalancing” a portfolio is the process of selling assets that now represent a higher percentage than intended and buying those that have dipped, ensuring your risk profile remains consistent with your financial goals.

3. Navigating Debt and Credit via Percentage Analysis

Debt is often the biggest hurdle to wealth accumulation. Most debt instruments are priced as a percentage, known as interest. Failure to understand how these percentages interact with your principal balance can lead to a cycle of perpetual payments.

Understanding Annual Percentage Rates (APR)

When you borrow money—whether via a credit card, mortgage, or auto loan—the cost of that capital is expressed as the APR. However, the APR is often calculated daily or monthly. To find your monthly interest charge on a credit card balance, you divide the APR by 12.

If you carry a $2,000 balance on a card with a 24% APR:

- Monthly Interest Rate: 2% (24% / 12)

- Monthly Interest Charge: $40 ($2,000 × 0.02)

By calculating this percentage, consumers can see exactly how much of their “minimum payment” is going toward the bank’s profit versus reducing their own debt.

The Impact of Credit Utilization Ratios

In the realm of credit scoring, the “Credit Utilization Ratio” is a vital percentage. It is calculated by dividing your total used credit by your total available credit limits.

** (Total Credit Used / Total Credit Limit) × 100 = Utilization % **

FICO and other scoring models generally reward individuals who keep this percentage below 30%. Monitoring this specific percentage is often more effective for increasing a credit score than simply paying off small chunks of debt randomly.

Debt-to-Income (DTI) Ratio

For those looking to secure a mortgage, the DTI ratio is the gatekeeper. Lenders calculate this by taking your total monthly debt obligations and dividing them by your gross monthly income. Most lenders look for a DTI percentage of 36% or lower. Knowing how to calculate this percentage allows a prospective homeowner to determine exactly how much house they can afford before they ever step foot in a bank.

4. Business Finance: Percentages as Performance Indicators

For entrepreneurs and corporate professionals, percentages are the vital signs of a business. They provide context to the “Top Line” (Revenue) and the “Bottom Line” (Net Income).

Profit Margin Calculations (Gross vs. Net)

A business can have millions in revenue and still be failing if its margins are too slim.

- Gross Profit Margin: [(Revenue – Cost of Goods Sold) / Revenue] × 100. This shows the efficiency of production.

- Net Profit Margin: (Net Income / Revenue) × 100. This shows the overall profitability after all expenses, taxes, and interest.

By tracking these percentages, a business owner can identify if they need to raise prices (low gross margin) or cut administrative overhead (low net margin).

Calculating Year-over-Year (YoY) Growth

Investors and stakeholders use YoY growth percentages to gauge a company’s trajectory. Comparing the current quarter’s earnings to the same quarter in the previous year provides a clearer picture of growth than comparing consecutive months, which may be skewed by seasonality (e.g., holiday retail surges).

** YoY Growth = [(Current Period Value – Prior Period Value) / Prior Period Value] × 100 **

Consistent double-digit YoY growth is often what drives stock prices higher and attracts venture capital.

Break-Even Analysis

Before launching a new product or service, a business must calculate the break-even point. This often involves determining the “contribution margin” as a percentage. This percentage tells the business owner how much of every dollar in sales is available to cover fixed costs. Mastering this allows for strategic scaling and risk mitigation.

5. Harnessing Financial Tools for Precise Analysis

While mental math is a valuable skill, professional financial management requires precision. Modern tools have simplified the way we calculate and visualize percentages.

Leveraging Spreadsheet Software

Programs like Microsoft Excel and Google Sheets are built on the logic of percentages. Using the “Percent” cell format automatically multiplies your decimal results by 100 and adds the “%” symbol. Advanced users utilize the PMT function to calculate loan payments, which relies heavily on percentage-based interest inputs.

Financial Calculators and Apps

For complex scenarios like mortgage amortization or compound interest projections, specialized financial calculators are indispensable. These tools allow you to input annual percentage rates, compounding frequencies, and inflation adjustments to see the long-term impact of your financial decisions.

The Insightful Conclusion

Calculating percentages is more than just a mathematical exercise; it is a fundamental pillar of financial intelligence. From the micro-level of daily spending to the macro-level of global investment strategies, percentages provide the clarity needed to make informed decisions. By mastering these calculations, you empower yourself to evaluate opportunities, minimize costs, and maximize the growth of your net worth. In the world of money, those who understand the percentage are the ones who ultimately control the decimal point.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.