In the realm of real estate, the term “assessment” carries significant weight and often triggers a cascade of related financial and legal implications. Far from being a simple valuation, a real estate assessment is a formal, often government-mandated process that determines the value of a property for the purpose of taxation. This value, known as the assessed value, is then used by local authorities – typically municipalities, counties, or school districts – to calculate property taxes. Understanding the nuances of real estate assessments is crucial for homeowners, prospective buyers, and investors alike, as it directly impacts the cost of property ownership and can influence investment decisions.

The fundamental purpose of a real estate assessment is to create a fair and equitable system for funding public services. Property taxes are a primary revenue stream for local governments, financing everything from schools and public safety to infrastructure maintenance and parks. By assessing properties, tax authorities establish a baseline for distributing this tax burden. The higher a property’s assessed value, the greater its contribution to the local tax base. This system aims to ensure that those who benefit most from public services, often those with the most valuable properties, contribute proportionally more. However, the process itself can be complex, subject to various methodologies, and prone to disputes, making a thorough understanding essential for navigating the property ownership landscape.

The Purpose and Significance of Property Assessments

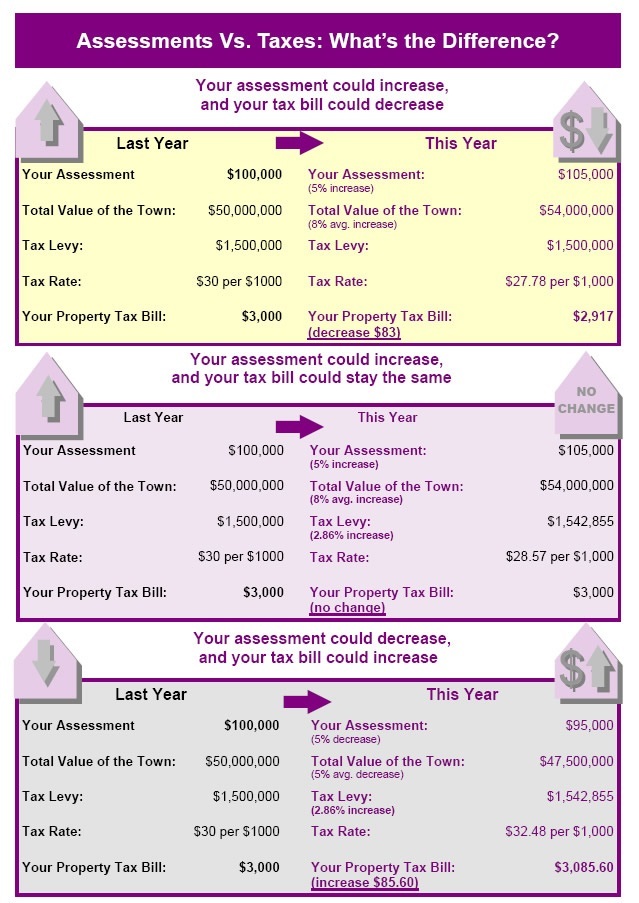

The core function of a property assessment is to establish a taxable value for real estate. This value is not necessarily the same as market value – the price a willing buyer would pay for the property on the open market. Instead, it’s a value determined by specific local regulations and appraisal methods. The assessed value serves as the foundation upon which property tax bills are calculated, making it a cornerstone of local government finance and a critical factor in the ongoing cost of owning real estate.

Funding Local Government Services

Property taxes are a vital source of revenue for local governments, underpinning the provision of essential public services that enhance the quality of life for residents. These services include:

- Education: Funding for public schools, from elementary to high school, is heavily reliant on property tax revenue. This includes teacher salaries, school supplies, facility maintenance, and extracurricular programs.

- Public Safety: Law enforcement, fire departments, and emergency medical services are often funded through property taxes, ensuring the safety and well-being of the community.

- Infrastructure: The maintenance and development of local infrastructure, such as roads, bridges, water systems, and sewage treatment plants, depend significantly on property tax contributions.

- Parks and Recreation: Public parks, community centers, libraries, and recreational facilities that enrich community life are often financed, in part or in whole, by property taxes.

- Other Municipal Services: Various other services, including waste management, street lighting, and administrative functions of local government, are also supported by property tax revenue.

The assessed value of properties within a jurisdiction directly dictates the potential revenue that can be generated. Therefore, accurate and fair assessments are paramount to ensuring that these services are adequately funded without placing an undue burden on any single group of taxpayers.

Establishing Taxable Value vs. Market Value

It is crucial to differentiate between a property’s assessed value and its market value.

- Market Value: This represents the price that a property would likely fetch in a competitive and open real estate market. It is influenced by factors such as location, size, condition, amenities, comparable sales, and overall economic conditions. Market value is dynamic and fluctuates with the ebb and flow of the housing market.

- Assessed Value: This is the value determined by the local tax assessor for the specific purpose of levying property taxes. The methods used to arrive at an assessed value vary by jurisdiction but often involve a standardized appraisal process. In many areas, the assessed value is a percentage of the property’s estimated market value, or it may be capped or adjusted by state-level legislation.

While market value provides a general idea of a property’s worth, the assessed value is the figure that directly impacts tax liabilities. A property might have a high market value but a lower assessed value, or vice versa, depending on the assessment methodologies employed and any legislative limitations. This distinction is vital when evaluating the affordability of a property, as property taxes are a recurring expense that must be factored into the total cost of ownership.

How Property Assessments are Determined

The process of determining a property’s assessed value involves a systematic appraisal by a local tax assessor. These assessors utilize various methodologies and data sources to arrive at a valuation that is intended to be fair and consistent across all properties within their jurisdiction. The specific approach can vary significantly, but generally falls into a few key categories.

Common Appraisal Methodologies

Tax assessors typically employ one or a combination of the following appraisal approaches:

- Sales Comparison Approach (Market Approach): This is the most common method for residential properties. It involves comparing the subject property to similar properties that have recently sold in the same area. Adjustments are made for differences in features, size, condition, and location to arrive at an estimated market value, which then informs the assessed value. Data for this approach relies heavily on recent sales records.

- Cost Approach: This method estimates the cost to replace the property’s structures with new ones of similar utility, minus any depreciation. It is often used for newer or unique properties where comparable sales are scarce, or for specialized structures like industrial buildings. Depreciation accounts for the physical wear and tear, functional obsolescence (outdated design), and economic obsolescence (external factors negatively impacting value).

- Income Approach: This method is primarily used for income-generating properties such as apartment buildings, commercial spaces, and rental homes. It estimates the property’s value based on its potential to generate income. This involves analyzing rental income, operating expenses, and vacancy rates to calculate net operating income, which is then capitalized at an appropriate rate to determine the property’s value.

The chosen methodology, or combination thereof, aims to reflect the property’s value at a specific point in time, as determined by local tax laws.

The Role of the Tax Assessor and Data Collection

The tax assessor’s office is the administrative body responsible for identifying taxable properties, maintaining property records, and conducting property appraisals to determine assessed values. Their work involves:

- Property Identification: Maintaining an up-to-date inventory of all taxable real estate within the jurisdiction.

- Data Collection: Gathering information on each property, which can include property characteristics (size, number of rooms, amenities), physical condition, zoning, and recent sales data for comparable properties. This data is often sourced from property deeds, building permits, site inspections, and public records.

- Appraisal and Valuation: Applying the appropriate appraisal methodologies to determine the assessed value. This is typically done on a cyclical basis, with properties being reassessed every few years, or more frequently if there are significant changes to the property or the local market.

- Notification: Informing property owners of their property’s assessed value, usually through an annual or periodic assessment notice.

The accuracy and fairness of the assessment process are heavily reliant on the quality and comprehensiveness of the data collected and the expertise of the tax assessors.

Understanding and Challenging Property Assessments

While the assessment process aims for fairness, errors can occur, and property owners often have the right to challenge their assessed value if they believe it is inaccurate or inequitable. This process typically involves several steps, from informal review to formal appeals.

The Assessment Notice and Informal Review

After a property has been assessed, the owner typically receives an official assessment notice detailing the determined value. This notice is a critical document, as it serves as the initial notification of the property’s taxable worth.

- Reviewing the Notice: The first step for a property owner is to carefully review the assessment notice. They should verify that all the property characteristics listed are accurate and that the assessed value appears reasonable in comparison to similar properties in the area.

- Informal Contact: If inaccuracies or concerns are identified, the next step is often to contact the local tax assessor’s office directly. This informal review period is designed to allow for the correction of simple errors, such as incorrect square footage or misplaced features, without the need for a formal appeal. Property owners can present evidence to support their claims, such as recent appraisals or sales data for comparable properties.

This initial stage provides an opportunity for a swift resolution of most discrepancies.

Formal Appeal Procedures

If an informal review does not resolve the issue, or if the property owner believes the assessed value is fundamentally unfair, they can initiate a formal appeal. The specifics of the appeal process vary significantly by jurisdiction, but generally involve presenting a case to an independent board or tribunal.

- Filing an Appeal: This typically involves submitting a formal appeal application within a specified timeframe. The application usually requires a clear statement of the grounds for appeal and supporting evidence.

- Evidence Presentation: During a formal appeal hearing, property owners will have the opportunity to present their case, often supported by an independent appraisal, sales data for comparable properties (often referred to as “comps”), or other documentation that demonstrates the property’s true market value or highlights errors in the assessor’s valuation.

- Appellate Bodies: The appeal may be heard by a local board of equalization, a county appeals board, or a state-level tax court, depending on the jurisdiction. These bodies are responsible for reviewing the evidence presented by both the property owner and the tax assessor and making a determination on the correct assessed value.

Successfully challenging an assessment can lead to a reduction in property taxes, making the appeal process a potentially significant financial benefit for property owners. It requires preparation, understanding of local assessment laws, and compelling evidence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.