In an increasingly complex financial world, mastering your household finances is not merely a suggestion—it’s a critical component of family well-being and long-term security. A family budget serves as a foundational financial roadmap, guiding your spending, savings, and investment decisions, and ultimately empowering you to achieve your financial aspirations. Far from being a restrictive exercise, budgeting is a powerful tool for clarity, control, and peace of mind. It demystifies where your money goes, highlighting opportunities to optimize resources, reduce debt, and build a resilient financial future for every member of your household. This comprehensive guide will walk you through the essential steps to create a practical, effective, and sustainable family budget that genuinely reflects your family’s unique financial landscape and goals.

The Foundation: Understanding Your Financial Landscape

Before you can effectively allocate your money, you must first understand its journey. This initial phase involves a thorough examination of your current financial inflows and outflows, providing a realistic snapshot of your economic reality. Without this clear picture, any budgeting efforts would be akin to navigating unfamiliar territory without a map.

Tracking Income Sources

The first step in understanding your financial landscape is to meticulously identify and total all sources of income flowing into your household. This includes not only regular salaries or wages but also any supplemental income streams such as freelance work, rental income, child support, alimony, pension payments, or even benefits. It’s crucial to calculate your net income—the amount of money you actually receive after taxes, deductions, and contributions (like 401k or health insurance premiums) are removed. This figure represents the actual spendable income you have to work with each month. Consistency is key here; aim for an average monthly net income if your pay varies, or use the lowest expected income to be conservative.

Identifying Fixed vs. Variable Expenses

Once your income is clearly established, the next crucial step is to categorize your expenditures. Expenses generally fall into two broad categories: fixed and variable.

- Fixed expenses are those that typically remain the same amount each month and are often contractual. Examples include rent/mortgage payments, car payments, insurance premiums, loan repayments, and subscription services. These are usually easier to account for and often have less flexibility for immediate adjustment.

- Variable expenses, on the other hand, fluctuate month-to-month and represent areas where you often have more control. This includes groceries, utilities (which can vary seasonally), transportation costs (gas, public transport), dining out, entertainment, and personal care. Thoroughly tracking these variable expenses for at least a month or two will provide invaluable insights into your spending habits and reveal potential areas for savings.

Differentiating Needs from Wants

A fundamental principle of effective budgeting, especially for families, is the ability to distinguish between needs and wants.

- Needs are essential for survival and basic functioning: housing, utilities, food, essential transportation, healthcare, and basic clothing. These are non-negotiable expenses that must be prioritized.

- Wants are discretionary expenses that enhance your quality of life but are not strictly necessary: dining out, entertainment, vacations, designer clothes, premium streaming services, and expensive hobbies. While wants contribute to happiness, they are also the first place to look for cuts when trying to free up funds or address financial shortfalls. Having a frank discussion as a family about what constitutes a “need” versus a “want” can foster a shared understanding and commitment to financial goals. This distinction allows you to consciously allocate resources, ensuring essentials are covered before indulging in desires.

Building Your Budget: Practical Steps

With a clear understanding of your income and expenses, you’re ready to construct the framework of your family budget. This phase involves choosing a budgeting methodology and strategically allocating your funds to align with your financial objectives.

Choosing a Budgeting Method

There isn’t a one-size-fits-all approach to budgeting; the best method is the one you and your family will consistently use.

- The 50/30/20 Rule: A popular and straightforward method, this allocates 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. It offers a balanced approach that can be easily adapted.

- Zero-Based Budgeting: With this method, every dollar of your income is assigned a “job” until your income minus your expenses equals zero. This doesn’t mean you spend all your money; rather, it means every dollar is intentionally allocated to an expense, saving, or debt repayment. This method provides maximum control and awareness.

- The Envelope System: A classic, tactile method often used for variable expenses, where physical cash is divided into envelopes labeled for specific categories (e.g., “Groceries,” “Entertainment”). Once an envelope is empty, spending in that category stops until the next budgeting period. This is excellent for those who tend to overspend with credit cards.

- Paycheck-to-Paycheck Budgeting: If income arrives bi-weekly, this method focuses on budgeting each paycheck individually to cover expenses until the next one.

Evaluate your family’s spending habits, comfort with technology, and need for flexibility or strictness to select the method that resonates most.

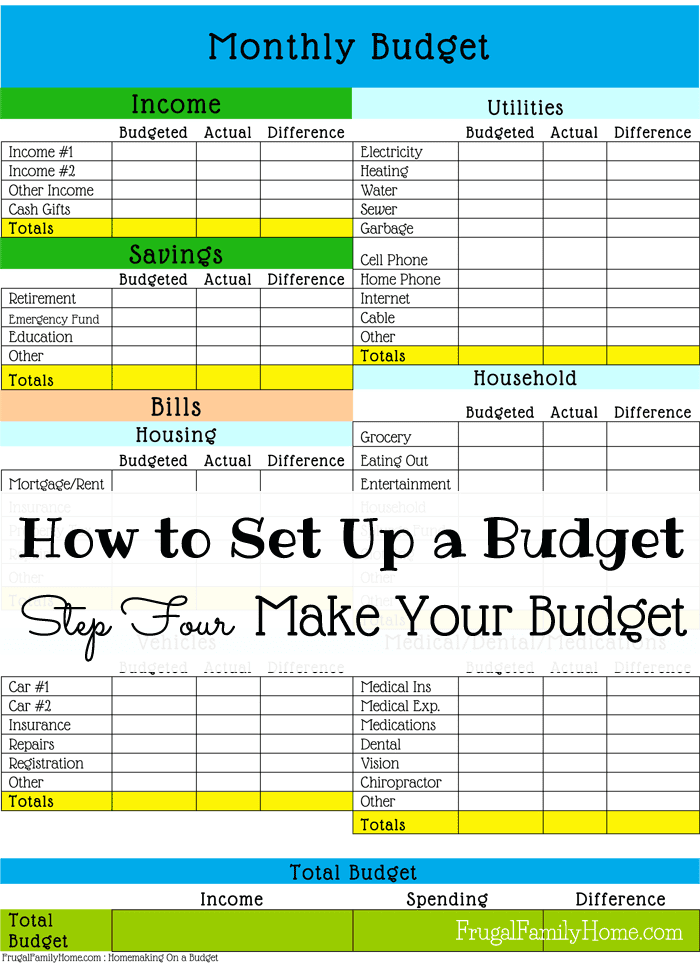

Allocating Funds to Categories

Once you’ve chosen a method, begin assigning specific dollar amounts to each expense category. Start with your fixed expenses, as these are usually non-negotiable. Then, move to your variable expenses, using your tracked spending data as a guide. It’s crucial to be realistic rather than overly optimistic in this initial allocation. Underestimating expenses can lead to budget failure.

For instance, if your tracking showed you spend an average of $800 on groceries, allocate that amount initially. If you aim to reduce it, set a slightly lower target, but be prepared to adjust if it proves unsustainable. Don’t forget to include categories for savings (emergency fund, retirement, college) and debt repayment beyond minimums. Each dollar should have a home, preventing “mystery spending” where money disappears without a clear purpose.

Setting Realistic Financial Goals

A budget is not just about tracking where your money goes; it’s about directing it towards where you want it to go. This means setting clear, measurable, and realistic financial goals as a family. These goals provide the motivation and direction for your budgeting efforts.

- Short-term goals (within one year): Building an emergency fund (3-6 months of living expenses), paying off a specific credit card, saving for a down payment on a car, or a family vacation.

- Mid-term goals (1-5 years): Saving for a larger down payment on a home, funding a child’s private school tuition, or major home renovations.

- Long-term goals (5+ years): Retirement planning, college savings, becoming debt-free, or significant wealth building.

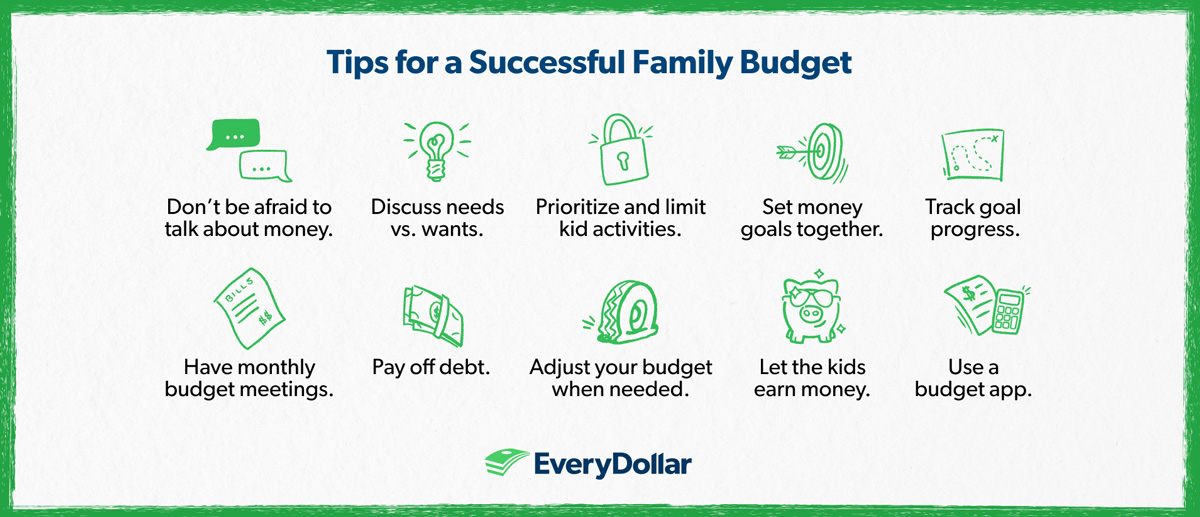

Discuss these goals openly with your family. Ensure they are specific (e.g., “Save $5,000 for an emergency fund by December 31st”), measurable, achievable, relevant, and time-bound (SMART). Aligning your budget allocations with these goals will make the process more meaningful and less burdensome, as every spending decision becomes a step towards a shared objective.

Implementing and Monitoring Your Budget

A budget is a living document, not a static one-time creation. Its effectiveness hinges on consistent implementation and regular monitoring. This ongoing engagement ensures your budget remains relevant and helps you adapt to life’s inevitable changes.

Tools and Resources for Budgeting

Modern personal finance offers a plethora of tools to simplify the budgeting process.

- Spreadsheets: For those comfortable with numbers, a simple spreadsheet (Excel, Google Sheets) offers complete customization and control. You can create columns for income, expenses, categories, and track actual versus budgeted amounts.

- Budgeting Apps/Software: Many digital tools (e.g., YNAB, Mint, Personal Capital, EveryDollar) can automate much of the tracking by linking directly to your bank accounts and credit cards. They categorize transactions, provide visual reports, and send alerts. While specific app recommendations aren’t our focus here, exploring these options can significantly streamline the monitoring process.

- Notebook and Pen: Don’t underestimate the power of a physical notebook. For some, the act of manually writing down every transaction enhances awareness and commitment, especially when paired with an envelope system.

Choose the tool that best suits your family’s preferences and tech comfort level. The key is finding a system that encourages regular engagement without feeling overly cumbersome.

Regular Review and Adjustment

Your family budget should be reviewed regularly—at least once a month, preferably weekly. This review isn’t about judgment; it’s about understanding and adapting.

- Compare Actual vs. Budgeted: See where you overspent or underspent. Were there unexpected expenses? Did you meet your savings goals?

- Identify Trends: Notice recurring overspending in certain categories or consistent underspending in others.

- Make Adjustments: Life changes. Income might increase or decrease, new expenses may arise (e.g., child care, medical bills), or old ones may disappear. Your budget needs to flex with these changes. Don’t be afraid to reallocate funds, revise category limits, or even completely overhaul your budgeting method if it’s not working. The goal is progress, not perfection. This iterative process is what makes budgeting truly effective over the long term.

Engaging the Whole Family

For a family budget to truly succeed, it needs to be a collaborative effort. Financial discussions often carry a stigma, but opening the lines of communication with your spouse and children (age-appropriately) can transform budgeting from a chore into a shared journey.

- Spousal Partnership: Both partners should be involved in setting goals, reviewing expenses, and making financial decisions. Shared ownership fosters accountability and reduces conflict.

- Teaching Children: Even young children can grasp basic financial concepts. Involve them in age-appropriate ways: explaining why you might choose to pack lunches instead of buying school lunches, or letting them allocate a small allowance towards their own wants. Older children can understand family financial goals and contribute ideas for saving. This early financial literacy is an invaluable life skill. When everyone understands the “why” behind the budget, there’s greater motivation to stick to it and achieve collective financial success.

Overcoming Budgeting Challenges and Staying Motivated

Budgeting is a marathon, not a sprint. You will encounter bumps along the road, but developing strategies to navigate these challenges is crucial for long-term success.

Dealing with Unexpected Expenses (Emergency Fund)

Life is unpredictable. Car repairs, medical emergencies, home repairs, or job loss can derail even the most carefully constructed budget. This is where an emergency fund becomes your financial safety net. Ideally, this fund should hold 3 to 6 months’ worth of essential living expenses, kept in a separate, easily accessible savings account. Building this fund should be one of your top financial goals. When an unexpected expense arises, you can draw from this fund without incurring debt or compromising your regular budget, providing a significant layer of financial security and peace of mind.

Avoiding Budget Burnout

Strict budgeting can sometimes feel restrictive, leading to burnout and eventual abandonment. To prevent this, build some flexibility into your budget.

- Allocate “Fun Money”: Include a small, guilt-free amount for discretionary spending that doesn’t need to be tracked rigorously. This allows for small indulgences without blowing the entire budget.

- Schedule Breaks: If you’re intensely tracking every penny, consider a slightly more relaxed approach during holidays or special occasions, provided you’ve budgeted for it.

- Focus on Progress, Not Perfection: Don’t let minor slip-ups derail your entire effort. If you overspend in one category, look for ways to trim in another or simply acknowledge it and get back on track next month. The goal is sustainable financial health, not absolute adherence to every single line item.

Celebrating Small Wins

Acknowledge and celebrate your family’s budgeting achievements, no matter how small. Did you stick to your grocery budget for the month? Did you hit a savings milestone? Did you pay off a small debt? Recognize these accomplishments. This positive reinforcement reinforces good financial habits and keeps the family motivated. It transforms budgeting from a punitive exercise into a rewarding journey towards shared goals. These small victories collectively build momentum and demonstrate the tangible benefits of your disciplined efforts.

The Long-Term Impact of Family Budgeting

Creating and maintaining a family budget extends far beyond simply managing monthly cash flow. It’s a strategic investment in your family’s future, laying the groundwork for enduring financial stability and prosperity.

Building Wealth and Financial Security

A consistently followed budget is the cornerstone of wealth creation. By consciously allocating funds for savings and investments, you transition from merely spending your income to actively growing it. Budgeting enables you to:

- Maximize Savings: Identify opportunities to save more efficiently for retirement, college funds, or large purchases.

- Reduce Debt: Prioritize debt repayment, freeing up future income for investments rather than interest payments.

- Invest Strategically: Free up capital to invest in stocks, bonds, real estate, or other assets that can compound over time, building significant long-term wealth.

This intentional management transforms your finances from a reactive response to income and expenses into a proactive strategy for building lasting financial security and potentially achieving financial independence.

Reducing Financial Stress

Financial stress is a pervasive issue that can impact mental health, relationships, and overall well-being. A family budget directly addresses this by providing clarity and control. When you know exactly where your money is going and what your financial situation is, much of the anxiety surrounding money dissipates.

- Eliminate Guesswork: No more wondering if you have enough for bills or emergencies.

- Proactive Planning: Anticipate large expenses and plan for them, rather than reacting to them in a crisis.

- Fewer Arguments: Shared financial goals and transparent budgeting can significantly reduce money-related conflicts within the family, fostering a more harmonious home environment.

The peace of mind that comes from knowing you are in control of your financial destiny is one of the most invaluable benefits of a well-executed family budget.

Teaching Financial Literacy to Children

Perhaps one of the most significant long-term impacts of family budgeting is the invaluable financial education it provides for your children. By openly discussing money, involving them in budgeting decisions, and demonstrating responsible financial habits, you are equipping them with essential life skills that will serve them well into adulthood.

- Value of Money: Children learn that money is a finite resource that requires careful management.

- Delayed Gratification: They understand the importance of saving for goals rather than immediate impulse spending.

- Decision-Making Skills: They witness how financial choices have consequences and learn to make informed decisions.

This practical exposure to personal finance within the family context cultivates a generation of financially responsible individuals, breaking cycles of financial struggle and fostering a legacy of economic empowerment.

Creating a family budget is an ongoing journey, not a destination. It requires dedication, flexibility, and open communication. However, the rewards—from immediate financial control and reduced stress to long-term wealth building and the priceless gift of financial literacy for your children—are immeasurable. Embrace this process as an empowering tool to shape a more secure, prosperous, and peaceful financial future for your entire family. Start today, and watch your financial landscape transform.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.