ACH direct deposit is a fundamental component of modern financial transactions, enabling individuals and businesses to transfer funds electronically without the need for physical checks. At its core, it’s an automated system for disbursing money directly into a bank account. This process is facilitated by the Automated Clearing House (ACH) network, a U.S. financial network used for electronic fund transfers. Understanding how ACH direct deposit works, its benefits, and its implications is crucial for anyone navigating personal finance, managing business operations, or seeking efficient ways to receive payments.

The ACH network operates as a centralized batch processing system, meaning transactions are grouped together and processed at specific intervals throughout the day. This contrasts with real-time gross settlement (RTGS) systems, which process each transaction individually and immediately. While this batch processing can sometimes mean a slight delay compared to instant transfers, it offers a highly cost-effective and reliable method for a vast number of transactions, making it the backbone of many payroll, tax refund, and government benefit disbursements.

The ubiquity of ACH direct deposit has revolutionized how we receive and make payments. From receiving your paycheck every two weeks to getting your tax refund from the government, ACH direct deposit has become the default method for many organizations. It’s not just about convenience; it also offers significant advantages in terms of speed, security, and cost-effectiveness compared to traditional paper-based methods.

The Mechanics of ACH Direct Deposit

To truly grasp what ACH direct deposit is, it’s essential to understand the underlying infrastructure and the players involved. The ACH network is managed by Nacha (formerly the National Automated Clearing House Association), a not-for-profit organization that sets the rules and standards for ACH transactions. These rules ensure the security, reliability, and efficiency of the network.

The Automated Clearing House (ACH) Network

The ACH network is a vast electronic network connecting virtually all financial institutions in the United States. It’s not a physical place, but rather a system of interconnected computers and communication protocols that allow financial institutions to exchange payment information securely and efficiently. Think of it as the digital highway for money movement between bank accounts.

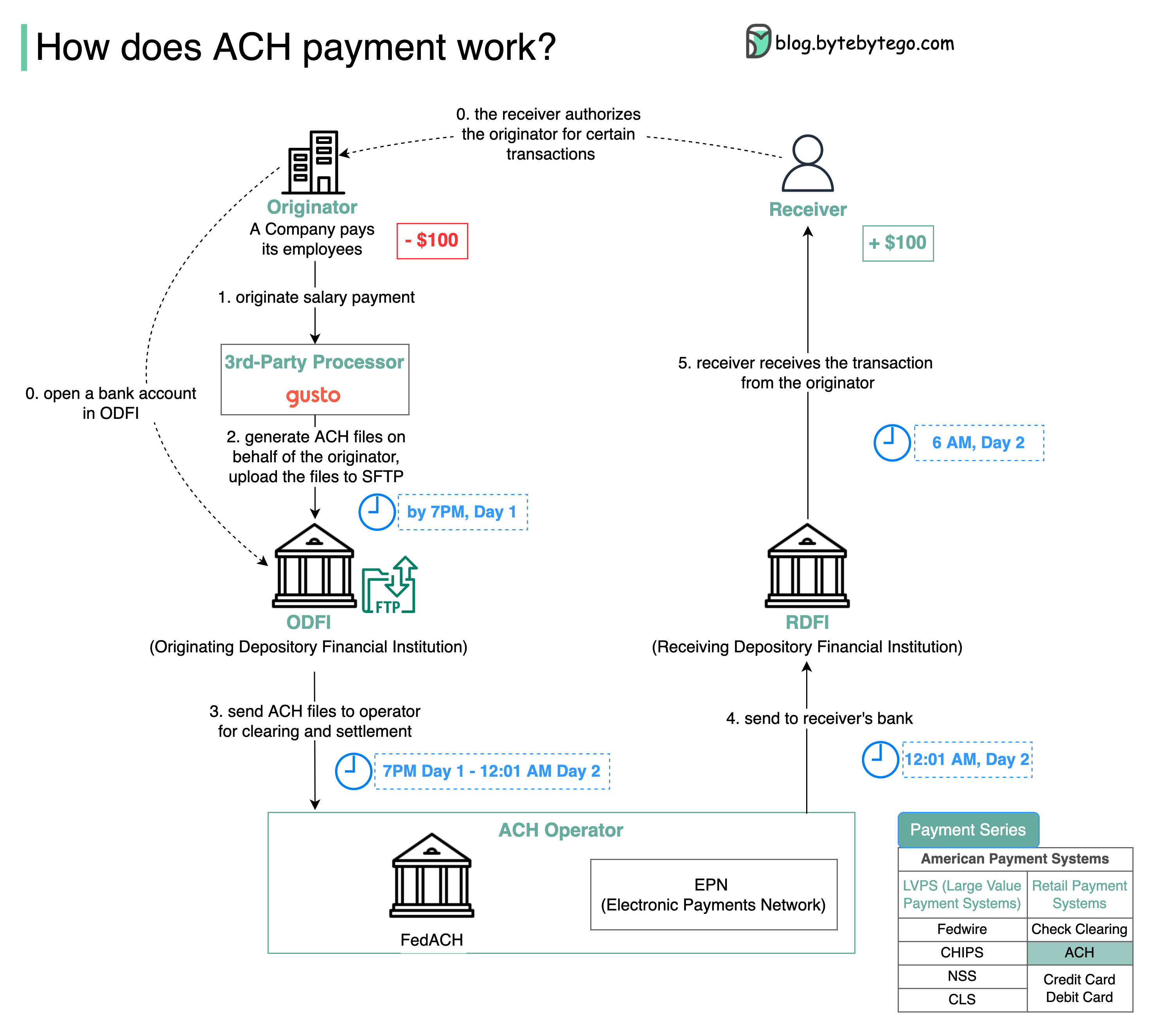

The network operates through two main types of transactions: ACH credits and ACH debits. ACH direct deposit falls under the category of ACH credits. In an ACH credit transaction, a company or government agency (the “originator”) instructs its bank to send funds to another person or company’s bank account (the “receiver”). This is in contrast to an ACH debit, where a company might pull funds from a customer’s account, such as for recurring bill payments.

Key Players in the ACH Direct Deposit Process

Several entities are involved in making an ACH direct deposit happen smoothly:

- Originator: This is the entity initiating the payment. For direct deposit, it’s typically an employer, a government agency (for tax refunds or benefits), or a company paying dividends.

- Originating Depository Financial Institution (ODFI): This is the bank of the originator. The ODFI receives the payment instructions and the funds from the originator and submits them to the ACH network for processing.

- ACH Operator: The ACH network is operated by two private-sector financial utilities: the Federal Reserve Banks and The Clearing House. These operators act as central clearinghouses, receiving batches of transactions from ODFIs and sorting them for delivery to the appropriate Receiving Depository Financial Institutions (RDFIs).

- Receiving Depository Financial Institution (RDFI): This is the bank of the receiver – the individual or entity getting paid. The RDFI receives the payment instructions and funds from the ACH operator and credits the receiver’s account.

- Receiver: This is the individual or entity whose bank account is being credited with the funds.

The process typically involves the originator providing their bank with a file containing the details of all individuals to be paid, including their bank routing number and account number. This file is then sent to the ODFI, which processes it and transmits it to the ACH operator. The ACH operator sorts the transactions and sends them to the respective RDFIs. Once received, the RDFI verifies the information and credits the receiver’s account.

Benefits of ACH Direct Deposit

The widespread adoption of ACH direct deposit is a testament to its numerous advantages for both individuals and businesses. It offers a compelling alternative to traditional payment methods, streamlining financial operations and enhancing convenience.

For Individuals: Convenience and Security

For individuals, ACH direct deposit offers unparalleled convenience. Gone are the days of waiting for a paper check to arrive in the mail, then having to physically deposit it at a bank or ATM.

- Timeliness: Funds are typically available in the recipient’s account on the payment date, meaning no waiting for checks to clear. This predictable access to funds is vital for managing personal budgets and meeting financial obligations.

- Reduced Risk of Loss or Theft: Paper checks can be lost, stolen, or misplaced during transit or while awaiting deposit. ACH direct deposit eliminates this risk, as the funds are electronically transferred directly into a secure bank account.

- No Need for Physical Bank Visits: Individuals don’t need to make special trips to the bank to deposit checks, saving time and effort. This is particularly beneficial for those with busy schedules or limited mobility.

- Automatic Savings and Payments: Direct deposit can be used not only for receiving income but also for setting up automatic transfers to savings accounts or for bill payments, promoting better financial management and discipline.

For Businesses: Efficiency and Cost Savings

Businesses also reap significant rewards from implementing ACH direct deposit for payroll and other disbursements. The efficiency gains and cost reductions can be substantial.

- Reduced Administrative Overhead: Processing and distributing paper checks involves significant labor costs, printing expenses, and postage. ACH direct deposit automates much of this process, freeing up administrative staff for other tasks.

- Lower Costs per Transaction: ACH transactions are generally much cheaper than processing paper checks. The cost savings multiply with the volume of transactions, making it a more economical choice for payroll and vendor payments.

- Improved Cash Flow Management: By automating payments, businesses can better predict and manage their outgoing cash flow. This also helps in ensuring that employees and vendors are paid on time, fostering positive relationships.

- Enhanced Security: ACH transactions are transmitted through secure, encrypted networks, reducing the risk of fraud associated with physical checks, such as counterfeiting or alteration.

- Environmental Benefits: Reducing the reliance on paper checks contributes to a more sustainable business practice by minimizing paper usage and transportation emissions.

![]()

Setting Up and Managing ACH Direct Deposit

Getting started with ACH direct deposit is typically a straightforward process, whether you are an individual receiving funds or a business initiating payments. The key lies in providing accurate banking information.

For Recipients: Providing Your Banking Details

If you are an individual expecting to receive payments via ACH direct deposit, such as your salary or government benefits, you will need to provide your banking information to the payer. This usually involves:

- Bank Routing Number: This nine-digit number identifies your specific financial institution. You can find it on the bottom of your checks, by logging into your online banking portal, or by contacting your bank directly.

- Account Number: This is your unique account identifier at your bank. You can also find this on your checks or through your online banking.

Many employers provide a direct deposit form that you will need to fill out with this information. It’s crucial to ensure that the routing and account numbers are accurate, as errors can lead to payment delays or misdirected funds. In some cases, you might need to provide a voided check to confirm the banking details.

For Payers: Initiating Direct Deposit Payments

For businesses or organizations that want to send payments via ACH direct deposit, the process involves setting up an account with a bank or a third-party payment processor that offers ACH origination services. This typically requires:

- Obtaining Authorization: You must have explicit authorization from the recipient to debit or credit their account. This is usually obtained through signed agreements or completed forms.

- Creating a Payment File: You will need to compile a payment file containing the necessary information for each recipient, including their bank details, payment amount, and any relevant transaction codes. This file is often generated using accounting or payroll software.

- Submitting the File to Your Bank: The payment file is then submitted to your bank (the ODFI). Your bank will validate the file and transmit it to the ACH operator for processing.

- Reconciliation: After the transactions have been processed, you will receive reports from your bank that allow you to reconcile the payments made and ensure that all transactions were successful.

Security and Verification

The ACH network employs robust security measures to protect transactions. However, it is still important for both recipients and payers to remain vigilant.

- For Recipients: Always verify that the direct deposit payments you receive match the expected amounts and dates. If you notice any discrepancies, contact your employer or the paying entity immediately. Also, be cautious about sharing your banking information; only provide it to trusted sources.

- For Payers: Implement internal controls to ensure the accuracy of the data submitted for ACH transactions. Regularly review transaction reports and audit your direct deposit processes. Be aware of phishing scams that might attempt to solicit your banking information or credentials.

Common Uses and Future Trends of ACH Direct Deposit

ACH direct deposit has become an indispensable tool in the financial ecosystem, facilitating a vast array of transactions beyond just payroll. Its adaptability and efficiency suggest a continued and evolving role in the future of payments.

Beyond Payroll: Diverse Applications

While payroll is perhaps the most recognized application of ACH direct deposit, its utility extends far beyond employee compensation:

- Government Disbursements: Tax refunds, social security benefits, and other government payments are frequently disbursed via ACH direct deposit, providing timely financial support to millions of citizens.

- Consumer Payments: Many companies utilize ACH debits for recurring bill payments, such as utility bills, mortgage payments, and subscription services. This offers convenience for consumers and predictable revenue for businesses.

- Business-to-Business (B2B) Payments: ACH direct deposit is increasingly used for business payments, such as vendor payments and supplier invoices. This offers a cost-effective alternative to wire transfers or checks for large value transactions.

- Investment Payouts: Dividends, interest payments, and other investment-related payouts can be automatically deposited directly into investors’ bank accounts.

- Insurance Claims and Reimbursements: Many insurance companies now use ACH direct deposit to send out claim payouts and reimbursements to policyholders, expediting the process.

The Evolution of ACH and Future Outlook

The ACH network, while established, is not static. It continuously evolves to meet the changing demands of the digital economy.

- Faster Payments Initiatives: While traditional ACH operates on a batch system, there’s a growing push towards faster payment capabilities. Initiatives like the Real-Time Payments (RTP®) network, operated by The Clearing House, and the upcoming FedNow® Service from the Federal Reserve, aim to provide near-instantaneous fund availability, complementing the existing ACH infrastructure.

- Enhanced Security Features: As digital transactions become more prevalent, the focus on security intensifies. Nacha and financial institutions are constantly working on implementing advanced security protocols and fraud detection mechanisms to protect against evolving cyber threats.

- Integration with Digital Wallets and Fintech: ACH capabilities are being integrated into various digital wallets and fintech platforms, offering users more seamless ways to manage and move their money.

- Increased Adoption in E-commerce: While credit and debit cards dominate online payments, ACH is gaining traction for its lower processing fees, especially for higher-value transactions, and its ability to directly link to bank accounts.

In conclusion, ACH direct deposit is more than just a method for receiving paychecks; it’s a foundational element of the modern financial system that offers significant benefits in terms of efficiency, security, and convenience. Its continued evolution ensures its relevance and importance in the years to come, adapting to new technologies and consumer expectations while maintaining its core role as a reliable and cost-effective means of electronic fund transfer.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.