For veterans, active-duty service members, and eligible surviving spouses, the question “what is the VA mortgage rate today?” is more than just a search query; it is a critical starting point for one of the most significant financial decisions of their lives. In the current economic landscape, where interest rates fluctuate based on global market pressures, inflation data, and Federal Reserve policies, understanding the mechanics of VA loan pricing is essential for long-term wealth management.

The VA home loan remains one of the most powerful financial tools available in the United States. Because these loans are backed by the Department of Veterans Affairs, lenders are able to offer terms that are significantly more favorable than conventional or FHA counterparts. However, the “today” in that question is key—mortgage rates change daily, often hourly, influenced by a complex web of financial indicators.

Understanding the Factors Influencing Today’s VA Mortgage Rates

To understand today’s VA mortgage rates, one must look beyond the surface-level numbers. While the VA provides the guarantee, they do not set the interest rates. Private lenders—banks, credit unions, and mortgage companies—determine the rates based on several macroeconomic and individual factors.

The Role of the Federal Reserve and Inflation

While the Federal Reserve does not directly set mortgage rates, its influence is profound. The Fed’s management of the federal funds rate acts as a benchmark for the cost of borrowing across the economy. When inflation is high, the Fed typically raises rates to cool the economy, which leads to an upward trend in mortgage rates. Conversely, when inflation is under control or the economy needs a boost, rates tend to stabilize or fall. For a veteran monitoring the market today, keeping an eye on the Consumer Price Index (CPI) and Fed meeting minutes is a vital part of financial literacy.

Secondary Market Demand and MBS

Mortgage-backed securities (MBS) are the primary engine behind daily rate movements. VA loans are often packaged into Ginnie Mae securities. When investors have a high appetite for these bonds, prices go up and yields (rates) go down. In times of economic uncertainty, investors often flock to the safety of government-backed securities, which can paradoxically lead to lower VA rates even when the broader stock market is volatile.

Individual Financial Profiles

Even if the “market rate” is quoted at a specific percentage, your personal financial health dictates the final offer. Lenders look at credit scores, debt-to-income (DTI) ratios, and the loan-to-value (LTV) ratio. While VA loans are famously flexible—often allowing for lower credit scores than conventional loans—those with “prime” credit scores (usually 740 and above) will still secure the most competitive rates available on any given day.

The Financial Advantages of VA Loans Compared to Conventional Options

When analyzing today’s rates, it is crucial to compare the “total cost of capital” between VA loans and other products. The VA loan consistently outperforms other mortgage types in several key financial metrics, making it a cornerstone of personal finance for those who qualify.

No Down Payment Requirements

One of the most significant barriers to entry in real estate is the down payment. Conventional loans often require 3% to 20% down to secure a competitive rate. A VA loan allows for 100% financing. From a wealth-building perspective, this allows a veteran to keep their liquid capital invested in higher-yielding assets—such as diversified stock portfolios or retirement accounts—rather than tying up significant cash in home equity that doesn’t provide a monthly dividend.

Absence of Private Mortgage Insurance (PMI)

On a conventional loan, if you put down less than 20%, you are typically required to pay Private Mortgage Insurance. This is a monthly fee that protects the lender, not you. VA loans do not require PMI, regardless of the down payment amount. When you calculate the effective interest rate of a conventional loan including PMI, the VA rate becomes even more attractive. This monthly saving can represent hundreds of dollars that can be redirected toward debt reduction or investment.

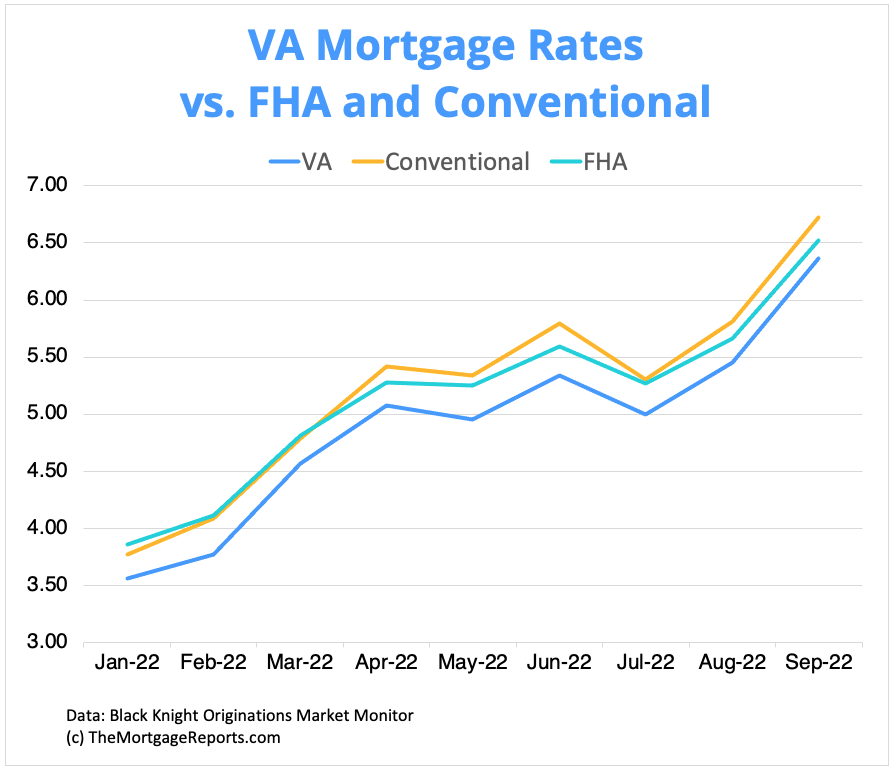

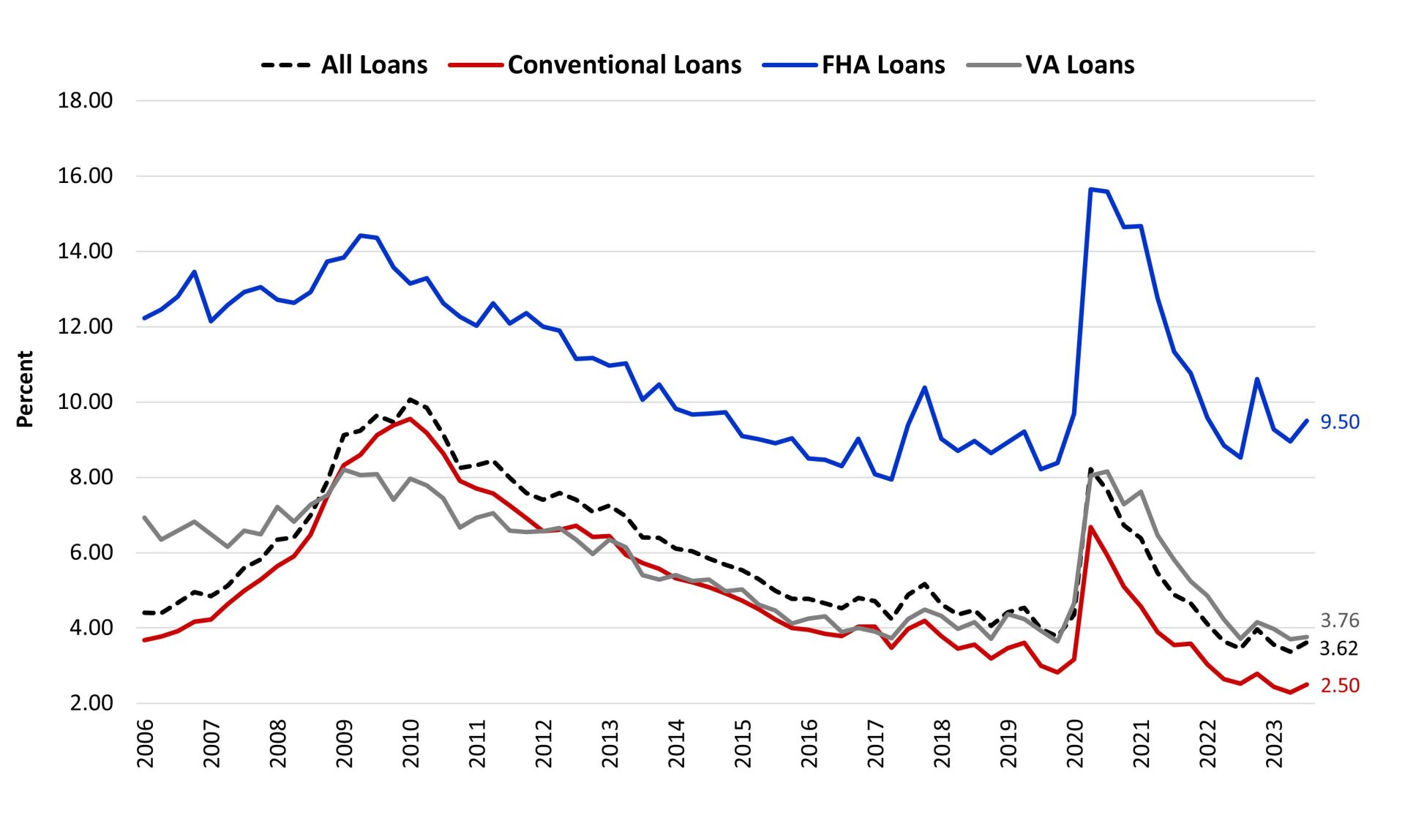

Lower Base Interest Rates

Historically, VA mortgage rates are approximately 0.25% to 0.50% lower than conventional mortgage rates. This is because the government guarantee reduces the risk for the lender. Over a 30-year amortization schedule, a half-percent difference on a $400,000 loan can save a borrower tens of thousands of dollars in interest payments. This makes the VA loan not just a “benefit,” but a superior financial instrument for long-term savings.

Navigating VA Loan Costs and Fees

While the interest rate is the headline figure, the true cost of a mortgage is reflected in the Annual Percentage Rate (APR), which includes fees. For veterans, understanding these costs is essential for accurate budgeting and financial planning.

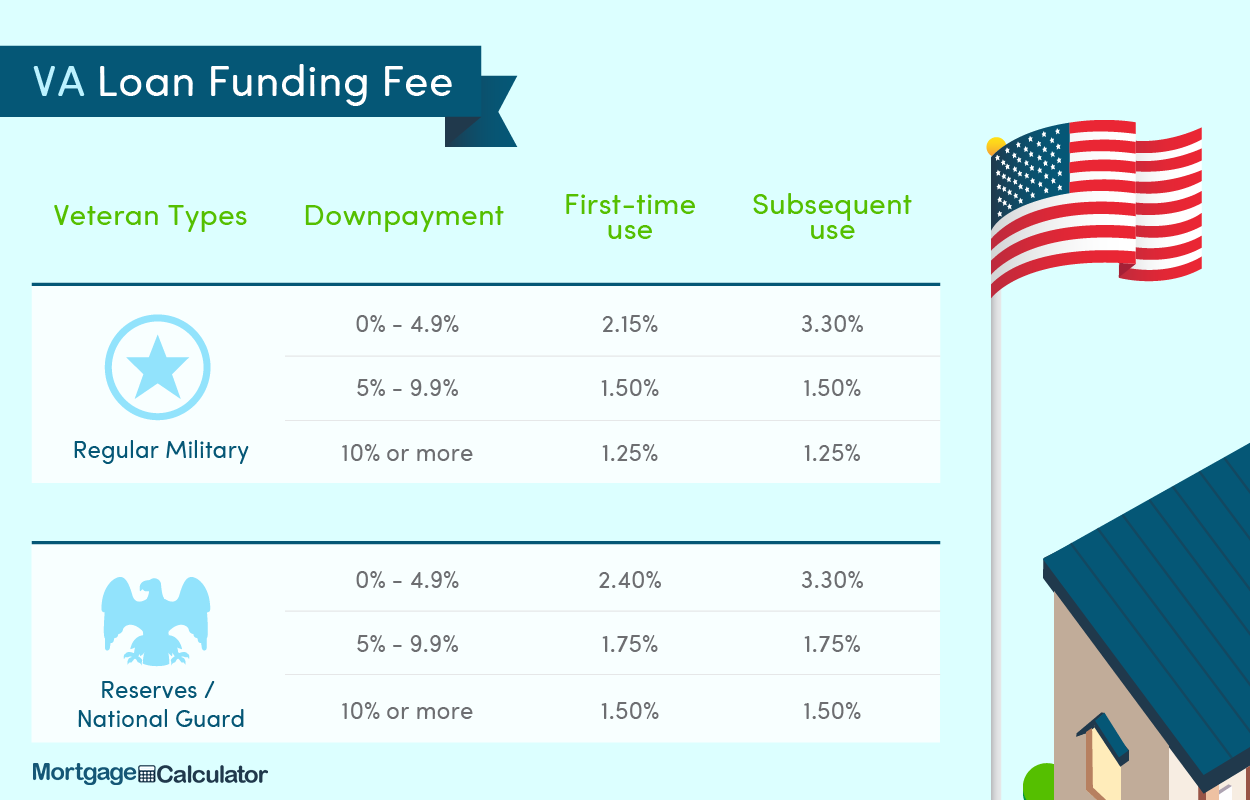

Understanding the VA Funding Fee

Instead of PMI, the VA charges a “Funding Fee.” This is a one-time payment that helps sustain the program for future generations. The fee varies depending on the down payment amount and whether it is the borrower’s first time using the benefit. For many, this fee can be rolled into the loan amount, meaning no out-of-pocket cost at closing. It is also important to note that veterans with service-connected disabilities are often exempt from this fee entirely, which significantly lowers the overall cost of the loan.

Closing Costs and Seller Concessions

The VA has strict rules about what closing costs a veteran is allowed to pay. These “non-allowable” costs must be covered by another party, often the lender or the seller. Furthermore, the VA allows sellers to contribute up to 4% of the sale price toward the buyer’s closing costs and even debt payoff. In a competitive financial strategy, a savvy veteran can use these concessions to “buy down” their interest rate using discount points, effectively lowering their monthly payment for the life of the loan.

The Long-term Impact of the IRRRL

The Interest Rate Reduction Refinance Loan (IRRRL), also known as a VA Streamline Refinance, is a powerful tool for when rates drop in the future. If you close on a home today and rates drop six months from now, the IRRRL allows you to refinance with minimal paperwork, no new appraisal (in most cases), and very low costs. This built-in “financial insurance” allows veterans to enter the market today without the fear of being “locked in” to a high rate if the market improves.

Strategic Financial Planning: When to Lock in Your VA Rate

Deciding when to “lock” a rate is one of the most stressful parts of the home-buying process. Because rates change daily, timing the market requires a mix of economic insight and personal financial readiness.

Market Volatility and the “Rate Lock” Strategy

A rate lock guarantees a specific interest rate for a set period, typically 30 to 60 days. In a volatile “upward” market, locking early is a defensive move to protect your purchasing power. If you are shopping for a home and today’s rate fits your budget, the “Money” niche perspective suggests locking in. Trying to squeeze an extra 0.125% out of the market is often a gamble that results in missing out on a favorable window.

The Impact of Loan Term: 15-Year vs. 30-Year

When looking at today’s rates, you will notice a significant difference between the 15-year and 30-year options. A 15-year VA loan typically offers a much lower interest rate, but the monthly payment is higher because the principal is amortized over a shorter period. For a veteran focused on aggressive wealth building and interest avoidance, the 15-year term is a powerhouse. However, for those prioritizing cash flow and liquidity, the 30-year term provides more flexibility, allowing for extra principal payments when the budget permits.

Assessing Opportunity Cost in a Changing Market

The final consideration in today’s VA rate environment is the opportunity cost of waiting. Many prospective buyers stay on the sidelines hoping for rates to return to historic lows. However, if home prices continue to appreciate while you wait for a 1% drop in rates, you may end up paying more for the asset than you saved on the financing. Real estate is a long-term play; the “best” rate is often the one that allows you to stop paying rent and start building equity in an appreciating asset.

Conclusion: Leveraging the VA Loan for Long-Term Wealth

Answering “what is the VA mortgage rate today” is only the beginning of a sophisticated financial journey. While the numerical value of the rate is important, the true value of the VA loan lies in its unique structure—the lack of a down payment, the absence of PMI, and the federal guarantee. These features create a low-friction entry into real estate that is unmatched in the private sector.

By understanding the macroeconomic forces at play, minimizing fees through exemptions or concessions, and utilizing tools like the IRRRL, veterans can turn a simple home loan into a robust vehicle for financial security. In the world of personal finance, the VA loan isn’t just a way to buy a house; it’s a way to leverage your service into a lasting financial legacy. Keep a close eye on the daily shifts in the bond market, consult with VA-specialist lenders, and remember that in the realm of compounding interest, the best time to start building equity was yesterday—the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.