Deciding to close a credit card account is a significant financial move that requires more than just a pair of scissors and a plastic shredder. Whether you are looking to simplify your financial life, eliminate an annual fee that no longer provides value, or move toward a debt-free lifestyle, canceling a Capital One credit card involves a strategic process.

In the realm of personal finance, your credit cards are more than just payment methods; they are integral components of your credit profile. Closing an account affects your credit utilization, the average age of your accounts, and your overall relationship with one of the largest banking institutions in the United States. This guide provides a professional, step-by-step roadmap to canceling your Capital One card while protecting your financial health and ensuring you don’t leave money on the table.

The Essential Pre-Cancellation Checklist

Before you pick up the phone or log into your portal, you must conduct a thorough audit of your account. Closing a card prematurely can result in the loss of earned rewards or missed payments on recurring subscriptions.

Redeeming Your Earned Rewards

Capital One is known for its “Miles” and “Cashback” ecosystems, found in popular products like the Venture and Savor series. One of the most common mistakes consumers make is canceling a card before exhausting their rewards balance. Generally, once a credit card account is closed, any unredeemed rewards are forfeited.

If you have a cashback card, ensure you have redeemed the balance as a statement credit or a check. For Venture miles, consider transferring them to travel partners or using them to cover recent travel purchases. If you have another Capital One card that earns the same type of rewards, you may be able to move your rewards to that active account, but you must confirm this with a representative before initiating the closure.

Clearing the Outstanding Balance

You cannot fully close a Capital One account if it carries a balance. Even if you stop using the card, interest may continue to accrue on any remaining principal. The most efficient way to handle this is to pay the balance in full and wait for the transaction to post.

Furthermore, keep an eye out for “trailing interest.” This is interest that accumulates between the time your last statement was issued and the time your payment was received. It is often best to overpay slightly or call Capital One to get a “payoff quote” to ensure the balance hits exactly zero.

Managing Automated Subscriptions

In our modern subscription economy, many of us have “set it and forget it” payments tied to our credit cards. Audit your last three months of statements to identify recurring charges such as gym memberships, streaming services, insurance premiums, or utility bills. Transition these payments to a new card or bank account at least one billing cycle before you cancel the Capital One card to avoid service interruptions or late fees.

Navigating the Cancellation Process

Once your house is in order, you are ready to proceed with the cancellation. Capital One offers several avenues for this, but each requires a different level of interaction and documentation.

The Direct Method: Phone Cancellation

The most common way to cancel a Capital One card is by calling their customer service department. For most cards, the number is 1-800-227-4825. When you call, navigate the automated menu to reach a representative.

Be prepared for a “retention offer.” Banks spend a significant amount of money acquiring customers, and they are often loath to lose them. The representative may offer to waive your annual fee for a year or provide a bonus point incentive to keep the account open. If your goal is strictly to close the account for financial simplification, be firm but polite. State clearly: “I would like to close this account, and I am not interested in any retention offers at this time.”

The Written Method: Cancellation by Mail

For those who prefer a paper trail—which is highly recommended for significant financial moves—you can cancel your account via mail. This provides you with physical evidence of your request. Send a formal letter to:

Capital One

Attn: General Correspondence

P.O. Box 30285

Salt Lake City, UT 84130-0285

In your letter, include your name, address, and the last four digits of your account number. Explicitly state that you are closing the account and request a written confirmation that the account has been closed with a $0 balance.

Handling the Retention Department

If you are canceling because of a high annual fee, you might find yourself speaking with the retention department. This is a specialized team authorized to give you “deals” to stay. While this guide focuses on cancellation, it is worth noting that if they offer to “downgrade” your card to a no-fee version (like moving from a Venture X to a VentureOne), it might be better for your credit score than a full cancellation. This keeps the credit line open without the cost.

Understanding the Impact on Your Credit Score

From a personal finance perspective, the biggest concern regarding account closure is the impact on your FICO or VantageScore. Closing a credit card is rarely “credit neutral”; it usually causes a temporary dip in your score.

Credit Utilization Ratio

Your credit utilization ratio—the amount of credit you are using compared to your total available credit—accounts for 30% of your FICO score. When you close a Capital One card, you are effectively reducing your total available credit limit.

For example, if you have two cards with $5,000 limits ($10,000 total) and you carry a $2,000 balance on one, your utilization is 20%. If you cancel the empty card, your total limit drops to $5,000, and your utilization suddenly jumps to 40%. This spike can lower your credit score significantly. Ensure your other cards have low balances before closing an account to mitigate this effect.

Average Age of Accounts

The “Length of Credit History” accounts for 15% of your score. Closing an old account can eventually lower the average age of your accounts. While closed accounts in good standing stay on your credit report for up to 10 years, once they fall off, the age of your credit profile could shrink. If your Capital One card is your oldest account, you should think twice before closing it, as it acts as an “anchor” for your credit age.

The Impact on Credit Mix

Lenders like to see that you can manage different types of credit (revolving credit like cards and installment credit like loans). If the Capital One card is your only credit card, closing it will negatively impact your “credit mix.” However, for most people with multiple cards, this impact is negligible.

Strategic Alternatives to Closing the Account

Sometimes, the desire to cancel is driven by a specific pain point that can be resolved without actually closing the account. Exploring these alternatives can save your credit score while still achieving your financial goals.

The “Product Change” or Downgrade

If the primary reason for cancellation is a $95 or $395 annual fee, ask for a “Product Change.” Capital One frequently allows users to move from a fee-bearing card to a “no-annual-fee” version within the same family. For instance, moving from the Savor card to the SavorOne. This allows you to keep the account age and the credit limit (helping your utilization) without paying for the privilege of keeping the card in your wallet.

Locking the Card

If you are canceling because you are afraid of overspending, Capital One offers a “Lock” feature in their mobile app. Locking the card prevents any new purchases while keeping the account open. This is a great way to “retire” a card from your daily rotation without the negative credit implications of a formal closure.

Consolidating Credit Lines

In some cases, you may be able to ask Capital One to move the credit limit from the card you wish to close to another Capital One card you intend to keep. While Capital One’s policies on this change frequently, it is always worth asking. If you have a $10,000 limit on a card you’re closing, moving that limit to your primary card prevents your total available credit from shrinking, thereby protecting your utilization ratio.

Conclusion: Finalizing Your Financial Move

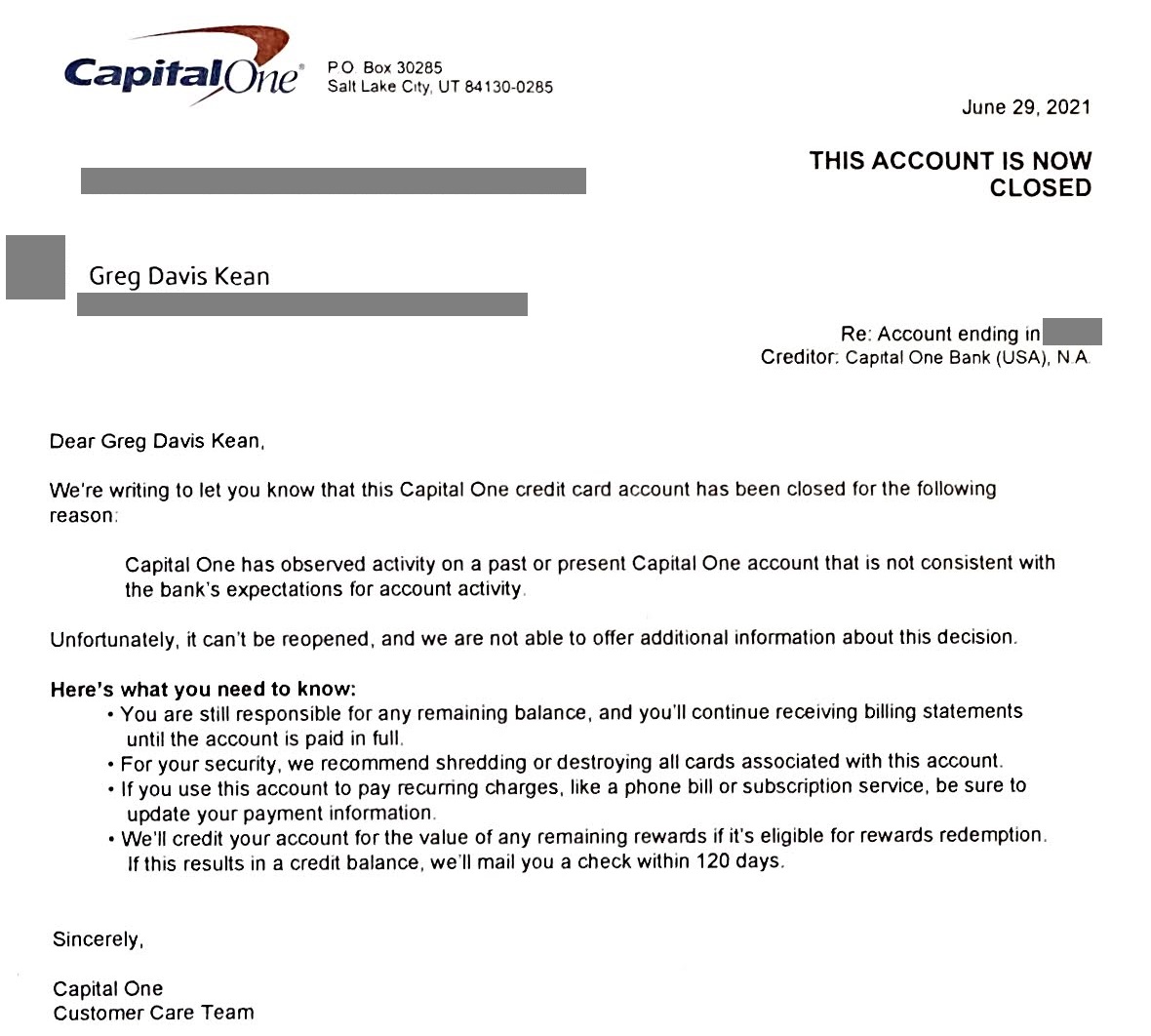

Once the representative confirms the closure, or you receive your letter in the mail, your work is almost done. After 30 to 60 days, pull a copy of your credit report from AnnualCreditReport.com to ensure the account is reported as “Closed by Consumer.” This distinction is important; it looks better to future lenders than “Closed by Grantor,” which implies the bank terminated the relationship due to poor management.

Finally, destroy the physical card. Modern Capital One cards often contain metal, so a standard home shredder may not suffice. You can usually return metal cards to Capital One via a prepaid envelope for secure destruction, or use heavy-duty shears to dispose of the chip and magnetic strip.

Canceling a credit card is a powerful assertion of financial control. By following this structured approach, you ensure that your transition away from Capital One is handled with the professional diligence your financial future deserves.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.