In the landscape of global finance, few entities command as much attention, scrutiny, and awe as Apple Inc. When investors and analysts ask, “How much is Apple worth?” they are not merely asking for a sticker price on a corporate entity. They are inquiring about a financial phenomenon that has redefined the parameters of the modern stock market. Apple is not just a technology company; it is a cornerstone of the global economy, a massive engine of cash flow, and a benchmark for institutional and individual portfolios alike.

Understanding the valuation of Apple requires a deep dive into the mechanics of market capitalization, the intricacies of its balance sheet, and the strategic financial decisions that have propelled it to become the first company in history to hit milestones that were once considered impossible.

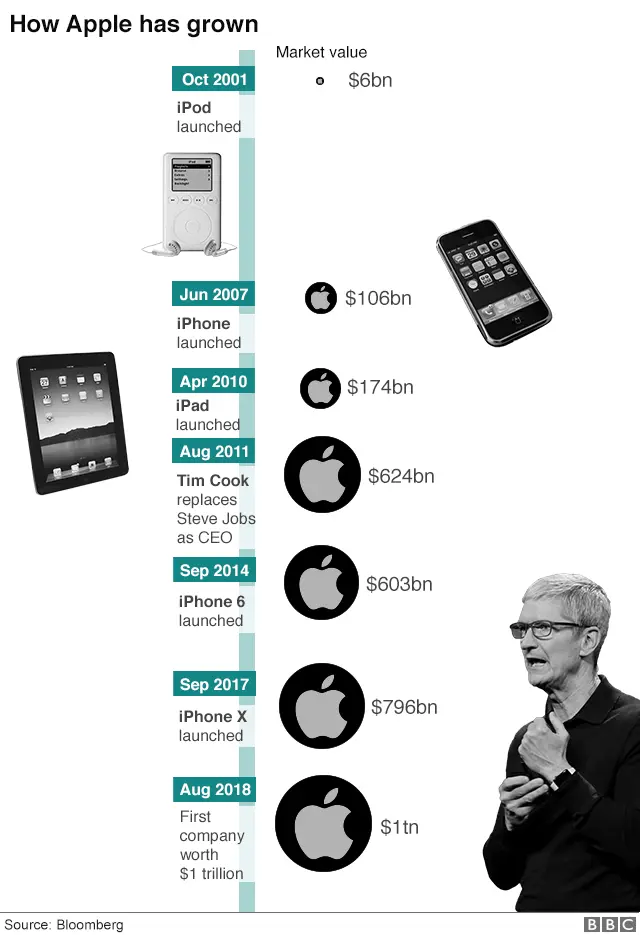

Decoding Market Capitalization: How Apple Reached the $3 Trillion Milestone

The most common way to measure what a company is “worth” is through its market capitalization. This figure is calculated by multiplying the total number of outstanding shares by the current market price of a single share. For Apple, this number has become a revolving door of record-breaking achievements.

The Mechanics of Stock Price and Outstanding Shares

Market capitalization is a dynamic figure, shifting with every tick of the stock market. However, Apple’s journey to the top has been characterized by a unique paradox: while its stock price has generally trended upward over the long term, the company has actively reduced its number of outstanding shares through aggressive buyback programs.

From a purely financial perspective, this increases the “worth” of each individual share because the company’s earnings are divided among fewer slices of the pie. When investors assess Apple’s value, they are looking at a combination of high demand for the stock and a shrinking supply of it, a formula that has consistently driven its market cap into the trillions.

Historical Context: From Near Bankruptcy to Market Leader

To appreciate Apple’s current multi-trillion dollar valuation, one must look back at its financial trajectory. In the late 1990s, Apple was weeks away from bankruptcy. Its valuation was a fraction of its peers. The “worth” of the company today is a testament to one of the most successful financial turnarounds in corporate history.

The transition from a niche computer manufacturer to a diversified consumer electronics and services powerhouse allowed it to cross the $1 trillion mark in 2018. The speed at which it moved from $1 trillion to $2 trillion, and eventually touching $3 trillion, signals a fundamental shift in how the market values big tech: no longer as cyclical hardware companies, but as essential infrastructure for modern life.

Beyond the Balance Sheet: The Financial Drivers of Apple’s Valuation

While the market cap provides a snapshot of value, the true “worth” of Apple is rooted in its ability to generate staggering amounts of profit. Analysts look beyond the headline numbers to see what is actually powering the engine.

Revenue Streams: Services vs. Hardware

For decades, Apple’s valuation was tied almost exclusively to the iPhone. While the iPhone remains a massive revenue driver, the financial community has re-rated Apple’s worth based on the growth of its Services division. This includes the App Store, iCloud, Apple Music, and Apple Pay.

From an investing standpoint, services are more valuable than hardware. Hardware sales are subject to upgrade cycles and supply chain disruptions. Services, however, provide recurring, high-margin revenue. The “worth” of a dollar earned from a subscription is generally viewed by Wall Street as more valuable than a dollar earned from a one-time device sale because of its predictability and lower cost of goods sold.

Profit Margins and the Luxury Tech Premium

Apple maintains profit margins that are the envy of the manufacturing world. By positioning its products as “premium” or “luxury” tech, Apple avoids the “race to the bottom” on pricing that plagues many of its competitors. This pricing power is a critical component of its valuation.

When a company can maintain 40%+ gross margins while operating at a scale of hundreds of billions of dollars in revenue, it creates a massive “moat.” This financial security allows Apple to trade at a premium valuation (a higher Price-to-Earnings ratio) compared to other hardware companies, as investors are willing to pay more for every dollar of Apple’s profit due to its perceived stability and quality.

The Investor’s Perspective: Why Wall Street Prizes Apple Stock

For the individual investor or the institutional fund manager, Apple is often viewed as a “safe haven” or a “proxy for the market.” Its valuation is buoyed by its status as a cornerstone of the S&P 500 and the Nasdaq-100.

Dividend Growth and Massive Share Buybacks

One of the most significant contributors to Apple’s perceived worth is its capital return program. Apple sits on one of the largest cash piles in corporate history. Instead of letting this cash sit idle, the company has returned hundreds of billions of dollars to shareholders.

Through dividends, Apple provides a steady income stream to investors. More importantly, its share buyback program is the largest in the world. By spending billions each quarter to buy its own stock, Apple creates a “floor” for its share price. For investors, this financial engineering is a sign of a mature, disciplined company that prioritizes shareholder value, further inflating what the market is willing to pay for the company.

Valuation Metrics: P/E Ratios and Cash Flow Analysis

To determine if Apple is “overvalued” or “undervalued” at any given price point, financiers use the Price-to-Earnings (P/E) ratio. Historically, Apple traded at a P/E of 10 to 15. As it proved the resilience of its ecosystem, that ratio expanded to 25, 30, or even higher.

Beyond earnings, the “worth” of Apple is found in its Free Cash Flow (FCF). Apple generates tens of billions in FCF every quarter. This is the actual cash left over after the company has paid all its expenses and reinvested in its business. This cash flow is the lifeblood of the company, providing it the “dry powder” to acquire startups, fund research and development, and weather economic downturns without ever needing to take on expensive debt.

Risk Factors and Future Growth: Can Apple Sustain Its Valuation?

No valuation is permanent, and Apple faces constant pressure to justify its multi-trillion dollar price tag. The “worth” of the company is intrinsically tied to its future growth prospects and its ability to mitigate global risks.

Global Economic Pressures and Supply Chain Realities

Apple’s valuation is sensitive to geopolitical tensions and global economic health. Because a significant portion of its manufacturing is concentrated in certain regions and a large percentage of its sales come from international markets, currency fluctuations and trade policies can impact its bottom line.

Inflation also plays a role. If consumer spending power decreases, the “luxury” status of Apple products could be tested. Investors constantly monitor Apple’s ability to navigate these headwinds; any sign of a permanent slowdown in iPhone demand or a contraction in margins could lead to a significant “de-rating” of the company’s valuation.

Emerging Markets and Future R&D Investments

To maintain and grow its worth, Apple must find the “next big thing.” This is why Wall Street watches Apple’s R&D spending so closely. Whether it is the foray into spatial computing with the Vision Pro, advancements in artificial intelligence, or the expansion of financial services, the company must prove it can continue to innovate.

Furthermore, Apple’s “worth” in the next decade will likely be determined by its success in emerging markets like India. As the middle class grows in these regions, the potential for millions of new users to enter the Apple ecosystem provides a long-term “growth tailwind.” If Apple can successfully replicate its Western ecosystem success in these high-growth regions, its market capitalization could see further unprecedented milestones.

Conclusion: The Perpetual Valuation of Excellence

How much is Apple worth? The answer is a moving target, currently hovering in the trillions, but the underlying factors remain constant. Apple’s value is built on a foundation of unparalleled brand loyalty, high-margin services, disciplined capital management, and a massive cash flow that provides a safety net few other companies possess.

For the student of finance or the casual investor, Apple serves as the ultimate case study in corporate valuation. It demonstrates that “worth” is not just about what you sell today, but about the ecosystem you build, the efficiency with which you manage your capital, and the trust you instill in the global financial markets. As long as Apple remains the center of the digital consumer’s universe, its financial valuation will likely continue to be the yardstick by which all other corporate successes are measured.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.