In the digital age, peer-to-peer payment apps like Venmo have revolutionized how we split bills, pay friends, and manage small transactions. It offers unparalleled convenience, allowing instant money transfers between users with just a few taps on a smartphone. However, while receiving money on Venmo is often quick and easy, the ultimate goal for many users is to integrate these funds into their broader financial ecosystem – specifically, by moving them into a traditional bank account where they can be saved, invested, or spent via conventional banking methods. Understanding the nuances of this transfer process is crucial for effective personal finance management, ensuring your money is where you need it, when you need it, without unnecessary delays or costs. This guide delves into the practical steps and strategic considerations for efficiently cashing out your Venmo balance, placing these actions within the context of sound financial planning.

Understanding Venmo Balances and Transfer Options

Before you can effectively move money from Venmo, it’s essential to grasp how Venmo holds your funds and the different pathways available for transfer. This foundational understanding is key to making informed decisions that align with your financial needs and timeline.

The Venmo Balance: More Than Just a Digital Wallet

When you receive money on Venmo, it resides within your Venmo balance, which functions much like a digital wallet. Unlike a traditional bank account, your Venmo balance does not typically earn interest, nor does it possess the same regulatory protections as funds held in FDIC-insured banks. While it’s incredibly convenient for immediate peer-to-peer transactions, treating your Venmo balance as a long-term holding place for significant funds isn’t advisable from a financial management perspective. Its primary purpose is to facilitate quick payments, not serve as a savings or primary checking account. Proactively transferring funds out ensures they can be leveraged more effectively elsewhere.

Standard vs. Instant Transfers: Speed and Cost Considerations

Venmo offers two primary methods for transferring money to your linked bank account: standard transfers and instant transfers. The choice between these depends largely on your urgency and willingness to incur a small fee. A standard transfer typically takes 1-3 business days to process and deposit into your bank account. This option is free of charge, making it the most cost-effective choice for non-urgent situations. Conversely, an instant transfer lives up to its name, usually completing within minutes, often less than 30 minutes. However, this expedited service comes with a fee, typically 1.75% of the transferred amount (with a minimum of $0.25 and a maximum of $25.00), which is deducted directly from the transfer sum. Understanding this trade-off between speed and cost is vital for optimal financial decision-making.

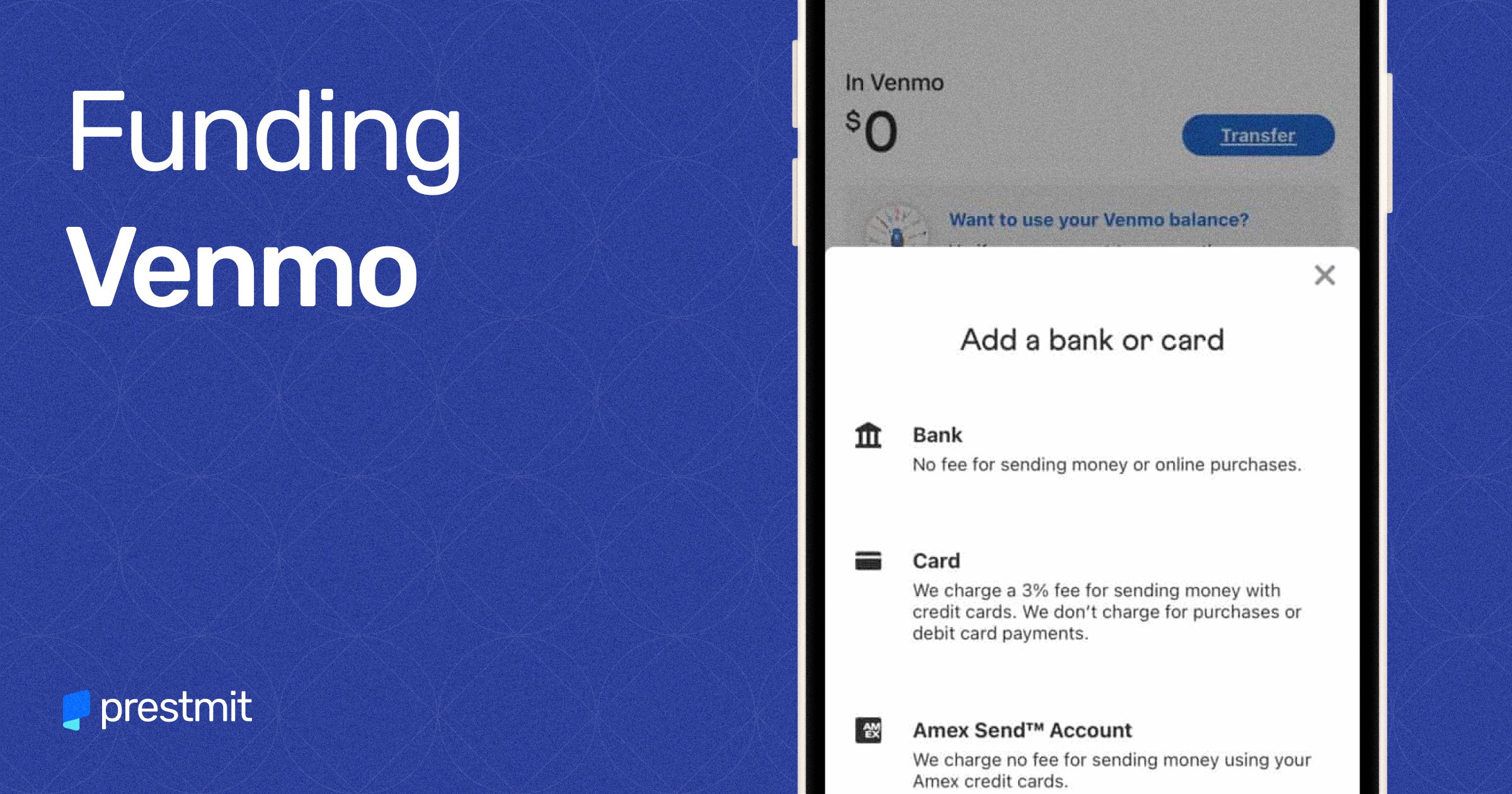

Linking Your Bank Account or Debit Card for Seamless Transfers

To transfer money from Venmo, you must have a valid U.S. bank account or a Mastercard, Visa, American Express, or Discover debit card linked and verified within your Venmo profile. Linking a bank account usually involves Venmo making two small test deposits (e.g., $0.03 and $0.15) to your account, which you then verify in the Venmo app. This process confirms you are the legitimate owner of the bank account. For instant transfers, a linked debit card is often preferred as it facilitates the immediate movement of funds more reliably than some bank account connections. Ensuring your linked financial instruments are current and correctly verified is a prerequisite for any successful transfer, preventing delays and potential frustrations.

Step-by-Step Guide to Cashing Out Your Venmo Balance

Once you understand the basics, executing a transfer from Venmo to your bank account is a straightforward process. Following these steps carefully will help ensure a smooth and successful transaction, regardless of whether you choose the standard or instant option.

Initiating a Standard Bank Transfer

To perform a standard transfer, open your Venmo app and navigate to the “Me” tab, typically represented by your profile picture or initials. Tap the “Transfer Money” button, which should clearly display your current Venmo balance. On the subsequent screen, you’ll be presented with options. Select “Standard Transfer” (usually displayed as 1-3 business days and free). Next, enter the exact amount you wish to transfer. Double-check this figure to avoid errors. Then, select your linked bank account as the destination. Confirm all the details one last time before finalizing the transfer. You’ll receive a confirmation in the app, and the funds should appear in your bank account within the specified business days. Always initiate transfers well in advance if you have a deadline, accounting for weekends and public holidays.

Utilizing Instant Transfers for Urgent Needs

For those times when you need immediate access to your Venmo funds, the instant transfer option is invaluable. Similar to a standard transfer, begin by going to the “Me” tab and tapping “Transfer Money.” This time, select “Instant Transfer” (usually accompanied by information about the fee). Enter the desired transfer amount. Venmo will then display the exact fee and the net amount that will be deposited into your bank account or linked debit card. Carefully review these figures. Select your preferred linked debit card or bank account for the instant deposit. Confirm the transaction, acknowledging the fee. The funds should reflect in your chosen account within minutes. Remember, while convenient, the fee for instant transfers can add up, so reserve this option for genuine emergencies or time-sensitive financial obligations.

Troubleshooting Common Transfer Issues

While Venmo transfers are generally reliable, occasional issues can arise. If a standard transfer seems delayed beyond 3 business days, first check for bank holidays or weekends, as these do not count as business days. Verify that your linked bank account details are correct and that the account is still active and verified. Daily and weekly transfer limits imposed by Venmo can also restrict larger transfers; if you hit a limit, you may need to transfer funds in smaller increments or wait for the limit to reset. If an instant transfer fails, it might be due to an issue with your linked debit card or bank account, or perhaps Venmo’s internal processing. In any case of persistent issues, or if you suspect an error or unauthorized activity, immediately contact Venmo Support through the app or their website for assistance.

Strategic Financial Management with Your Venmo Funds

Integrating Venmo into your broader financial strategy requires more than just knowing how to transfer money. It involves understanding where Venmo fits in your overall financial picture and adopting habits that promote responsible money management.

Integrating Venmo into Your Budgeting Strategy

For many, Venmo is a convenient tool for splitting casual expenses, contributing to group gifts, or receiving reimbursements. However, money sitting in your Venmo balance should be considered “allocated” but not “accessed” funds within your personal budget. To maintain an accurate view of your financial standing, make it a habit to regularly transfer your Venmo balance to your primary checking or savings account. This ensures that all your liquid funds are consolidated in one place, allowing for more precise budgeting, expense tracking, and savings goal management. Don’t let a growing Venmo balance give a false sense of security; integrate it into your regular cash flow management processes.

The Opportunity Cost of Stagnant Venmo Balances

Leaving funds in your Venmo balance for extended periods carries an often-overlooked financial cost: opportunity cost. Money held in Venmo does not accrue interest, meaning it’s not working for you. In contrast, funds in a high-yield savings account or invested, even conservatively, have the potential to grow over time. Moreover, inflation slowly erodes the purchasing power of idle cash. By promptly transferring your Venmo balance to an interest-bearing account, you ensure your money has the chance to earn returns, combat inflation, or be directed towards high-priority financial goals like debt repayment or investment. Proactive transfers turn idle digital money into active financial capital.

Understanding Venmo’s Role in Your Overall Financial Health

Venmo is a powerful peer-to-peer payment tool, but it’s crucial to understand its limitations within your overall financial health strategy. It is not a bank, and as such, it lacks many of the features and protections offered by traditional financial institutions. For instance, Venmo transactions for goods and services often have limited buyer/seller protection compared to credit card purchases. For significant transactions, large transfers, or ongoing business income, relying solely on Venmo is generally not advisable. Use Venmo for its strengths – quick, casual, trusted-party payments – while leveraging banks and other financial tools for savings, investments, large purchases, and comprehensive financial security. This balanced approach ensures you harness Venmo’s convenience without compromising your broader financial well-being.

Maximizing Security and Preventing Financial Mishaps

While convenient, digital payment platforms like Venmo are attractive targets for fraudsters. Protecting your Venmo account and understanding how to act in case of a mishap is a critical component of responsible financial management.

Best Practices for Account Security

Maintaining robust security for your Venmo account is paramount. Start by using a strong, unique password that combines letters, numbers, and symbols, and avoid reusing passwords from other online services. Enable two-factor authentication (2FA), which adds an extra layer of security by requiring a code from your phone in addition to your password when logging in from a new device. Be wary of phishing attempts – unsolicited emails or messages asking for your Venmo login credentials or personal information. Venmo will never ask for your password via email or text. Regularly review your transaction history within the app to quickly spot any unauthorized activity and address it promptly.

Verifying Recipients and Transaction Details

A common source of Venmo-related financial mishaps stems from sending money to the wrong person or for the wrong amount. Venmo transactions between friends are typically final and irreversible, making careful verification essential. Always double-check the recipient’s username, phone number, or email address before hitting “Send.” If possible, confirm the amount verbally or through a separate communication channel, especially for larger sums. Scammers often create similar-looking usernames, hoping you’ll make a mistake. Exercise extreme caution, especially when paying strangers or for items purchased online, as Venmo’s design for casual P2P payments offers minimal recourse for fraud in these contexts.

What to Do If You Suspect Fraud or Errors

Despite best efforts, financial mishaps can occur. If you suspect your Venmo account has been compromised, or if you notice unauthorized transactions, act immediately. First, change your Venmo password and disconnect any suspicious linked devices. Then, contact Venmo Support directly through the app or their official website to report the issue. Provide them with all relevant details, including transaction IDs and timestamps. If the fraudulent activity involves your linked bank account or debit card, also notify your financial institution. While Venmo has certain protections, particularly for “eligible purchases” with authorized merchants, P2P payments to individuals you “trust” typically lack the same level of fraud protection as credit card transactions, underscoring the importance of vigilance and prompt action.

In conclusion, Venmo serves as an incredibly useful tool for modern financial interactions, simplifying peer-to-peer payments and making group expenses effortless. However, sound personal finance dictates that money should be managed actively and efficiently. By understanding the distinction between a Venmo balance and a traditional bank account, choosing the appropriate transfer method (standard or instant) based on your needs, and adhering to robust security practices, you can effectively integrate Venmo into your broader financial strategy. Regularly transferring your Venmo balance to an interest-earning account, budgeting for these funds, and recognizing Venmo’s specific role in your financial ecosystem are key steps towards maximizing convenience while safeguarding your financial health. Ultimately, “getting money off Venmo” isn’t just about the transfer; it’s about making your money work harder for you within a secure and well-planned financial framework.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.