In an era where global banking conglomerates often prioritize shareholder dividends over customer satisfaction, many consumers are turning toward a more community-focused alternative: the credit union. While traditional banks are owned by investors, credit unions are member-owned financial cooperatives. This fundamental difference in structure changes the entire dynamic of the banking relationship. However, because credit unions are not open to the general public in the same way a commercial bank is, many prospective members are unsure of how to gain entry.

Getting into a credit union is not as exclusive or difficult as it might have been decades ago, but it does require understanding the concept of “eligibility” and the “field of membership.” This guide provides a deep dive into the mechanics of credit union membership, the steps required to join, and why making the switch might be one of the most significant financial moves you make this year.

Understanding the Credit Union Difference

Before embarking on the journey of joining a credit union, it is essential to understand what these institutions are and why they have specific entry requirements. At their core, credit unions are built on the philosophy of “people helping people.”

Non-Profit Structure and Member Ownership

Unlike a commercial bank, a credit union is a 501(c)(14) non-profit organization. When you deposit money into a credit union, you aren’t just a customer; you are a “member-owner.” Your initial deposit—usually a small amount like $5 or $25—represents your “share” in the cooperative. Because there are no outside stockholders demanding a profit, any surplus earnings the credit union makes are returned to the members. These returns typically manifest as lower interest rates on loans, higher yields on savings accounts, and reduced fees.

Credit Unions vs. Traditional Banks

The primary distinction lies in the mission. While a traditional bank’s primary goal is to maximize profit for shareholders, a credit union’s primary goal is to provide affordable financial services to its members. This results in a more personalized approach to banking. Credit unions are often more willing to work with individuals who have less-than-perfect credit or who are looking for small-dollar loans that large banks might find unprofitable. Furthermore, because they are smaller and locally focused, the customer service experience is often rated significantly higher than that of national banking chains.

Navigating Eligibility: Finding Your Path to Membership

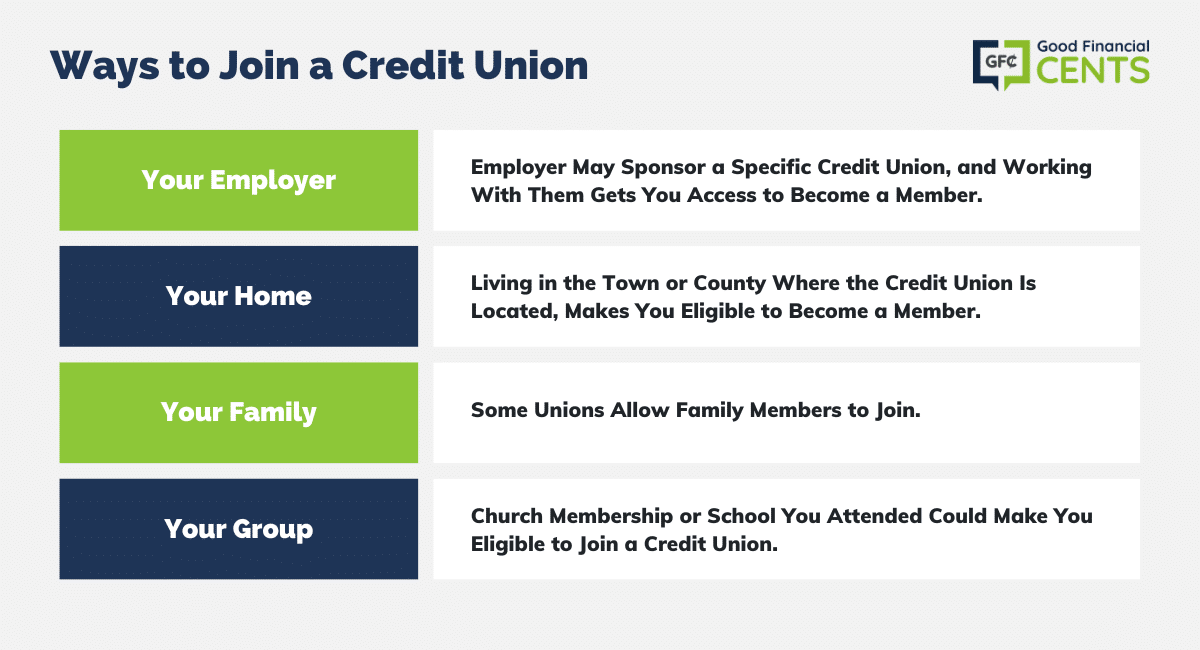

The most common hurdle to joining a credit union is the “Field of Membership” (FOM). By law, credit unions must define who they serve. This is what sets them apart from banks, which can theoretically serve anyone with a legal ID and cash. However, modern credit unions have expanded their FOMs to be incredibly inclusive.

Employment-Based Membership

Many of the largest credit unions in the country were founded to serve specific employer groups. For example, some were created for teachers, military personnel, or municipal employees. If your employer sponsors a credit union, you are automatically eligible to join. This often extends to retired employees of those organizations as well. Before looking elsewhere, check with your Human Resources department to see if your workplace is affiliated with a specific credit institution.

Geographic and Community Bonds

The most common way to join a credit union today is through a geographic bond. Many credit unions serve anyone who “lives, works, worships, or attends school” in a specific county, city, or metropolitan area. These community-chartered credit unions are designed to keep capital within the local economy. If you reside in a major city, there are likely several credit unions for which you are eligible based solely on your zip code.

Family and Household Connections

One of the most overlooked entry points is through family. Most credit unions allow immediate family members of existing members to join, regardless of where the relative lives or works. “Immediate family” usually includes spouses, children, siblings, parents, grandparents, and even household members who are not blood-related. If your spouse or parent belongs to a prestigious credit union, you likely have an “in” through their membership.

Professional Organizations and Associations

If you don’t meet the employment or geographic requirements, you can often join a credit union by becoming a member of an associated organization. Many credit unions partner with non-profits, labor unions, or advocacy groups. For instance, some credit unions allow you to join if you make a small, one-time donation (often as little as $10) to a specific environmental or educational charity. This effectively opens the credit union to anyone in the country who is willing to support that cause.

The Step-by-Step Process of Joining a Credit Union

Once you have identified a credit union for which you are eligible, the actual process of “getting in” is remarkably similar to opening a standard bank account, though it requires a few extra steps regarding your eligibility status.

Research and Selection

Not all credit unions are created equal. Before applying, compare the products they offer. Look at their mortgage rates, auto loan APRs, and the interest rates on their certificates of deposit (CDs). You should also check their digital infrastructure; if you rely heavily on mobile banking, ensure their app is modern and functional. Finally, verify that the institution is insured by the National Credit Union Administration (NCUA). The NCUA provides the same $250,000 protection for credit unions that the FDIC provides for banks.

Gathering Necessary Documentation

To streamline your application, have the following documents ready:

- Government-issued ID: A driver’s license, passport, or military ID.

- Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

- Proof of Eligibility: This might be a utility bill (for geographic membership), a pay stub (for employment membership), or proof of a donation to an affiliated non-profit.

- Initial Deposit: You will need a small amount of cash or a transfer from another bank to fund your “share account.”

The Application and Initial Deposit

Most credit unions allow you to apply online in about 10 to 15 minutes. During the process, you will be asked to choose which accounts you want to open. At a minimum, you must open a savings account (the share account) to establish your membership. Once your application is approved and your initial deposit is processed, you are officially a member-owner. You can then apply for credit cards, personal loans, or checking accounts with the institution.

Maximizing the Value of Your Membership

Joining is only the first step. To truly benefit from a credit union, you need to engage with its diverse financial ecosystem.

Lower Loan Rates and Higher Savings Yields

The most immediate benefit you will notice is the pricing. Because of their non-profit status, credit unions consistently offer lower interest rates on auto loans and mortgages. On the flip side, their “High-Yield” savings accounts often outperform those of “Big Four” banks. If you are planning a major purchase, such as a home or a car, being a credit union member can save you thousands of dollars in interest over the life of the loan.

Financial Literacy and Personalized Support

Credit unions are deeply invested in the financial health of their members. Many offer free financial counseling, credit-building workshops, and debt management tools. Because they are smaller, their loan officers often have more flexibility to look at the “whole person” rather than just a credit score. If you are trying to rebuild your credit, a credit union is often the best place to start, as they may offer credit-builder loans or secured credit cards designed for that purpose.

Shared Branching and ATM Networks

A common concern about credit unions is that they have fewer branches than national banks. However, many credit unions participate in the “CO-OP Shared Branching” network. This allows members of one credit union to walk into thousands of other credit union branches across the country and perform transactions as if they were at their home branch. Additionally, credit unions often belong to large, surcharge-free ATM networks (like Allpoint or MoneyPass), often giving members access to more ATMs than customers of even the largest national banks.

Common Obstacles and How to Overcome Them

While the process is generally straightforward, some applicants may encounter roadblocks. Understanding these can help you navigate the application more successfully.

Dealing with Credit History Issues

While credit unions are generally more lenient than banks, they still perform background checks. Most use a service called ChexSystems to see if you have a history of unpaid overdrafts or fraudulent activity at other financial institutions. If you have a “black mark” on your ChexSystems report, you might be denied a standard checking account. However, many credit unions offer “second-chance” accounts designed to help you rebuild your reputation in the banking system.

Finding “Open” Credit Unions

If you find that you truly do not meet any specific criteria for local or employer-based credit unions, look for “federally insured, low-income designated” credit unions or those with a “national” field of membership through association. Names like Navy Federal Credit Union (for military/veterans and their families) or PenFed (which used to be for military but is now open to almost anyone via simple requirements) are famous for their accessibility and high-quality service.

In conclusion, getting into a credit union is a strategic financial move that shifts the power back into your hands. By understanding the eligibility requirements and following the application steps, you can transition from being a mere customer of a bank to a member-owner of a community-focused financial cooperative. Whether you are looking for lower interest rates, better customer service, or a way to keep your money local, a credit union provides a robust and rewarding platform for your personal finance journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.