For many entrepreneurs, a small business loan is not just a financial instrument; it’s a launchpad for growth, a bridge over challenging times, or a catalyst for innovation. Access to capital is often the most significant hurdle for small businesses, making the ability to secure appropriate funding critical for survival and expansion in a competitive market. Understanding the intricacies of the application process, the various types of loans available, and the expectations of lenders can dramatically improve a business owner’s chances of success. This comprehensive guide will demystify the small business loan application process, providing a roadmap for securing the financial resources your enterprise needs to thrive.

Understanding Small Business Loan Options

Before embarking on the application journey, it’s crucial to understand the diverse landscape of small business loan products. Each option comes with its own set of requirements, advantages, and ideal use cases. Matching your business’s specific needs and financial profile with the right loan type is the first strategic step.

Traditional Bank Loans

Traditional banks, including national and regional institutions, have historically been a primary source of small business funding. They typically offer term loans, lines of credit, and commercial mortgages.

- Term Loans: These provide a lump sum of capital that is repaid over a fixed period with regular interest payments. They are often used for significant investments like equipment purchases or business expansion.

- Lines of Credit: Similar to a credit card, a line of credit offers a flexible pool of funds that can be drawn upon as needed, up to a certain limit. Interest is only paid on the amount borrowed, making it suitable for managing cash flow fluctuations or covering unexpected expenses.

- Commercial Mortgages: Specifically designed for purchasing or refinancing commercial real estate.

Pros: Often lower interest rates, longer repayment terms, and personalized service.

Cons: Stricter eligibility requirements, lengthy approval processes, and a preference for established businesses with strong credit histories and collateral.

SBA Loans (Small Business Administration Loans)

The U.S. Small Business Administration (SBA) doesn’t lend money directly but rather guarantees a portion of loans made by participating lenders (banks, credit unions, and online lenders). This government backing reduces the risk for lenders, making them more willing to lend to small businesses that might not qualify for traditional loans.

- SBA 7(a) Loans: The most common and flexible SBA loan program, offering up to $5 million for various business purposes, including working capital, equipment purchases, and real estate.

- SBA 504 Loans: Provides long-term, fixed-rate financing for major fixed assets like real estate or machinery, typically involving a partnership between a commercial lender, the SBA, and the borrower.

- SBA Microloans: Smaller loans, up to $50,000, for startup and expanding small businesses, often distributed through non-profit community-based organizations that also provide business assistance.

Pros: Lower down payments, longer repayment terms, and competitive interest rates compared to conventional loans. Easier to qualify for than direct bank loans, especially for startups or businesses with limited collateral.

Cons: Can still involve a lengthy application process due to both lender and SBA review, and significant paperwork.

Online Lenders

The rise of financial technology (fintech) has led to a proliferation of online lenders offering a diverse range of small business loan products. These lenders often leverage technology to streamline the application and approval process, providing faster access to funds.

- Term Loans: Similar to bank term loans but often with quicker approval and funding.

- Lines of Credit: Fast-access revolving credit for working capital.

- Short-Term Loans: Designed for immediate, smaller capital needs, with repayment periods ranging from a few months to a couple of years.

- Invoice Factoring/Financing: Selling your outstanding invoices to a third party at a discount to get immediate cash.

Pros: Faster application and approval times, more flexible eligibility criteria (some cater to businesses with less-than-perfect credit or shorter operating histories), and convenient online platforms.

Cons: Often higher interest rates and fees compared to traditional bank or SBA loans, potentially shorter repayment terms.

Alternative Financing Options

Beyond the mainstream, several alternative financing solutions exist for specific situations:

- Merchant Cash Advances (MCAs): A lump sum payment in exchange for a percentage of future credit card sales. Very fast, but extremely expensive.

- Crowdfunding: Raising small amounts of capital from a large number of individuals, often via online platforms. Can be equity-based, debt-based, or rewards-based.

- Grants: Non-repayable funds, typically offered by government agencies or foundations, for specific projects or industries. Highly competitive.

These options can be viable for businesses that cannot secure traditional loans but come with their own set of considerations regarding cost, equity dilution, or specific eligibility.

Preparing Your Business for a Loan Application

Regardless of the loan type you pursue, thorough preparation is paramount. Lenders are looking for signs of financial stability, responsible management, and a clear path to profitability. Presenting a well-organized and compelling case can significantly increase your chances of approval.

Develop a Robust Business Plan

Your business plan is the narrative of your company, outlining its vision, strategy, and financial projections. It demonstrates to lenders that you have a clear understanding of your market, operations, and how the loan will be used to achieve specific objectives.

- Executive Summary: A concise overview of your business and loan request.

- Company Description: What your business does, its mission, and legal structure.

- Market Analysis: Understanding your target market, competition, and industry trends.

- Organization and Management: Key personnel and organizational structure.

- Service or Product Line: Details of what you offer.

- Marketing and Sales Strategy: How you will reach and retain customers.

- Financial Projections: Crucial for lenders. This includes historical financial data (if applicable), realistic forecasts for revenue, expenses, and profitability, and how the loan will impact these figures.

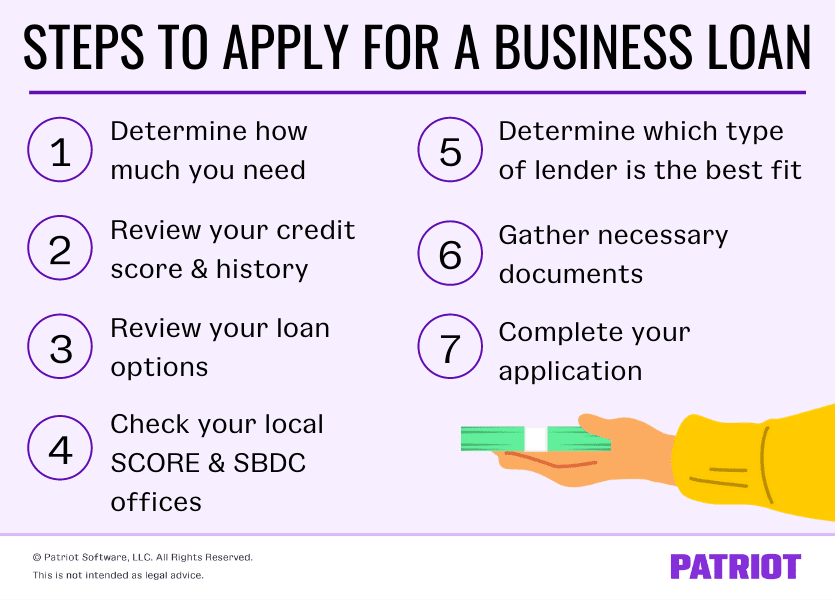

Organize Financial Documents

Lenders will scrutinize your financial health to assess your ability to repay the loan. Having all necessary documents prepared and organized beforehand will streamline the application process.

- Bank Statements: Business bank statements for the past 6-12 months.

- Tax Returns: Business tax returns for the past 2-3 years, and personal tax returns for business owners.

- Financial Statements:

- Profit & Loss (P&L) Statements: Also known as Income Statements, showing revenues, costs, and profits over a period.

- Balance Sheets: Snapshot of assets, liabilities, and owner’s equity at a specific point in time.

- Cash Flow Statements: Details how cash is generated and used, crucial for understanding liquidity.

- Accounts Receivable and Payable Aging Reports: Shows who owes you money and who you owe.

- Debt Schedule: A list of all existing business debts, including outstanding balances, interest rates, and payment schedules.

Understand Your Credit Score

Both your personal and business credit scores play a significant role in a lender’s decision.

- Personal Credit Score: Lenders often check the personal credit scores (FICO score) of business owners, especially for smaller loans or newer businesses, as it reflects past financial responsibility. Aim for a score of 680 or higher, with 720+ being ideal.

- Business Credit Score: Established businesses will have a business credit profile from agencies like Dun & Bradstreet, Experian Business, and Equifax Business. A strong business credit score indicates the company’s ability to handle financial obligations.

If your credit scores are low, take steps to improve them before applying. This might involve paying down debt, disputing errors on your credit report, or ensuring timely payments on all existing accounts.

Identify Collateral (if applicable)

For secured loans, lenders require collateral – assets that can be seized if you default on the loan. This reduces the lender’s risk. Common forms of collateral include:

- Real estate (commercial or sometimes personal, if cross-collateralized)

- Accounts receivable

- Inventory

- Equipment

- Vehicles

Having valuable, unencumbered collateral can significantly strengthen your loan application, particularly for traditional banks and SBA loans.

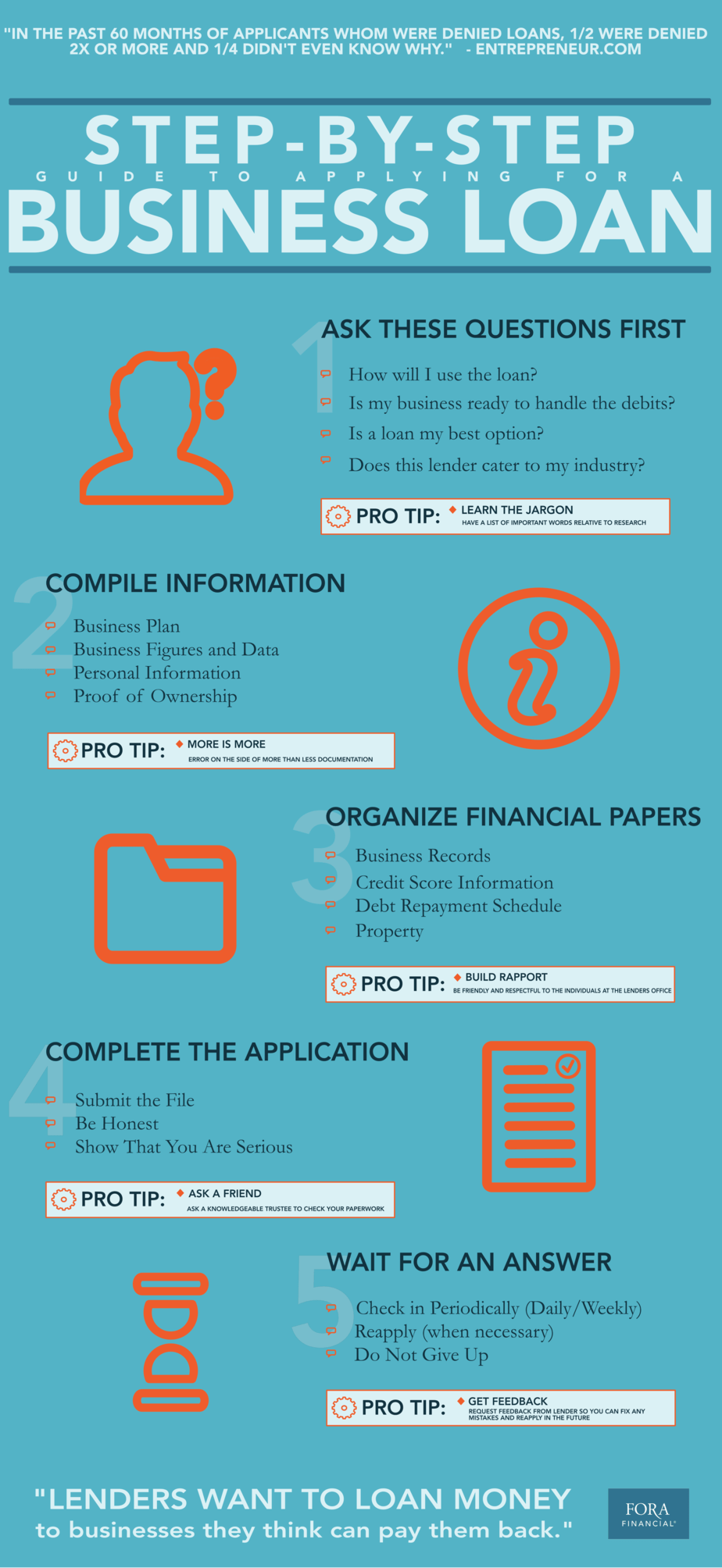

The Application Process: Step-by-Step

Once your business is prepared, the actual application process unfolds in several distinct stages. Navigating these steps effectively requires attention to detail and proactive engagement.

Research and Compare Lenders

Don’t settle for the first lender you find. Research multiple options, comparing their loan products, eligibility requirements, interest rates, fees, repayment terms, and customer service reviews. Consider your business’s specific needs (e.g., speed of funding, loan amount, type of collateral available) and match them with the lender’s offerings. Look for lenders who specialize in your industry or have a strong track record with businesses similar to yours.

Complete the Application Form Accurately

Carefully fill out the loan application form. Any inaccuracies or omissions can cause delays or even lead to rejection. Be honest about your financial situation. If you have questions, reach out to the lender for clarification. Double-check all figures and personal details.

Submit Required Documentation

Assemble all the financial and legal documents identified during your preparation phase. Create a clear, organized package for submission. If applying online, ensure all files are correctly formatted and uploaded. A comprehensive and well-presented document submission reflects professionalism and organization.

Be Prepared for Due Diligence

After submission, the lender will begin its due diligence process. This involves verifying the information you’ve provided, assessing your creditworthiness, and evaluating your business’s viability. You might be asked for additional documents, clarification on specific figures, or even an in-person interview. Be responsive, provide information promptly, and be ready to articulate your business plan and financial projections confidently.

Understand Loan Terms and Conditions

If your application is approved, the lender will provide a loan offer outlining the terms and conditions. This is a critical stage where you must meticulously review all aspects before signing.

- Interest Rate: Fixed or variable, and how it’s calculated.

- Repayment Schedule: Monthly, weekly, or other frequency; total number of payments.

- Fees: Origination fees, closing costs, prepayment penalties, late payment fees.

- Collateral Requirements: What assets are pledged.

- Covenants: Specific conditions you must adhere to during the loan term (e.g., maintaining certain financial ratios, not taking on additional debt without permission).

If anything is unclear, ask for explanations. Consider seeking advice from a financial advisor or legal counsel before finalizing the agreement.

Common Pitfalls and How to Avoid Them

Even with meticulous preparation, challenges can arise. Being aware of common pitfalls can help you navigate the process more smoothly.

Insufficient Preparation

The most frequent reason for loan rejection is inadequate preparation. Lenders are risk-averse and need to be confident in your ability to repay. A poorly organized application, incomplete documentation, or a vague business plan signals disorganization and higher risk. Spend ample time gathering documents, perfecting your business plan, and understanding your financial health.

Poor Credit History

A low personal or business credit score is a major red flag for lenders. If your credit is poor, applying immediately might be futile. Instead, focus on improving your scores by paying bills on time, reducing existing debt, and correcting any errors on your credit report. Consider alternative funding sources that are less credit-score dependent if immediate capital is needed, but always work towards better credit for future opportunities.

Unrealistic Financial Projections

While optimism is a valuable entrepreneurial trait, financial projections must be realistic and backed by market research and logical assumptions. Overly aggressive revenue forecasts or understated expense estimates will raise red flags. Lenders want to see conservative, achievable projections that demonstrate a clear understanding of your business’s financial reality and potential challenges.

Applying to the Wrong Lender

Not all lenders are created equal, and not all loan products suit every business. Applying to a traditional bank with a startup that has no collateral and poor credit is likely to result in rejection. Similarly, using a high-cost online short-term loan for a major equipment purchase isn’t financially sound. Researching and understanding which lenders and loan types align with your business’s stage, needs, and financial profile is crucial.

Beyond Approval: Managing Your Loan Effectively

Securing a loan is a significant achievement, but it’s only the beginning. Effective loan management is crucial for maintaining financial health and paving the way for future funding opportunities.

Adhere to Repayment Schedules

Timely loan repayments are non-negotiable. Missing payments or making late payments can severely damage your credit score, incur late fees, and strain your relationship with the lender. Set up automated payments or robust internal systems to ensure all installments are made on time. A strong repayment history builds trust and demonstrates financial responsibility, which is invaluable for future financing needs.

Monitor Business Performance

Continuously track your business’s financial performance against the projections you presented to the lender. This involves regularly reviewing your profit & loss statements, balance sheets, and cash flow. Ensure the funds are being used as intended and are contributing to the business’s growth as planned. If performance deviates significantly from projections, it’s an early warning sign that adjustments might be needed in your operations or financial strategy.

Maintain Communication with Your Lender

Building a good relationship with your lender is beneficial. If you anticipate any difficulties in making a payment or foresee a change in your business operations that might impact your ability to meet loan covenants, communicate proactively with your lender. They may be willing to work with you to find a solution, such as adjusting payment terms, rather than facing a default. Transparency and open communication foster trust and can lead to more favorable outcomes in challenging situations.

In conclusion, applying for a small business loan is a strategic endeavor that requires thorough preparation, careful decision-making, and diligent post-approval management. By understanding the available options, meticulously organizing your business’s financials, and approaching the process with a professional and insightful mindset, you can significantly enhance your chances of securing the capital needed to fuel your business’s success and sustainable growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.