Budgeting is often perceived as a restrictive practice—a financial straightjacket that prevents you from enjoying the fruits of your labor. However, in the realm of personal finance, a budget is actually a tool of liberation. It is a strategic roadmap that empowers you to take control of your capital, ensuring that your money is working for you rather than simply slipping through your fingers. To answer the question “how can I make a budget,” one must look beyond simple math and delve into a structured system of financial management.

Developing a budget is an essential skill for anyone looking to achieve financial independence, clear debt, or build wealth. By establishing a clear understanding of your cash flow, you can align your spending with your long-term goals. This guide provides a deep dive into the mechanics of budgeting, from initial assessment to the implementation of sophisticated financial frameworks.

Foundations of Budgeting: Assessing Your Financial Landscape

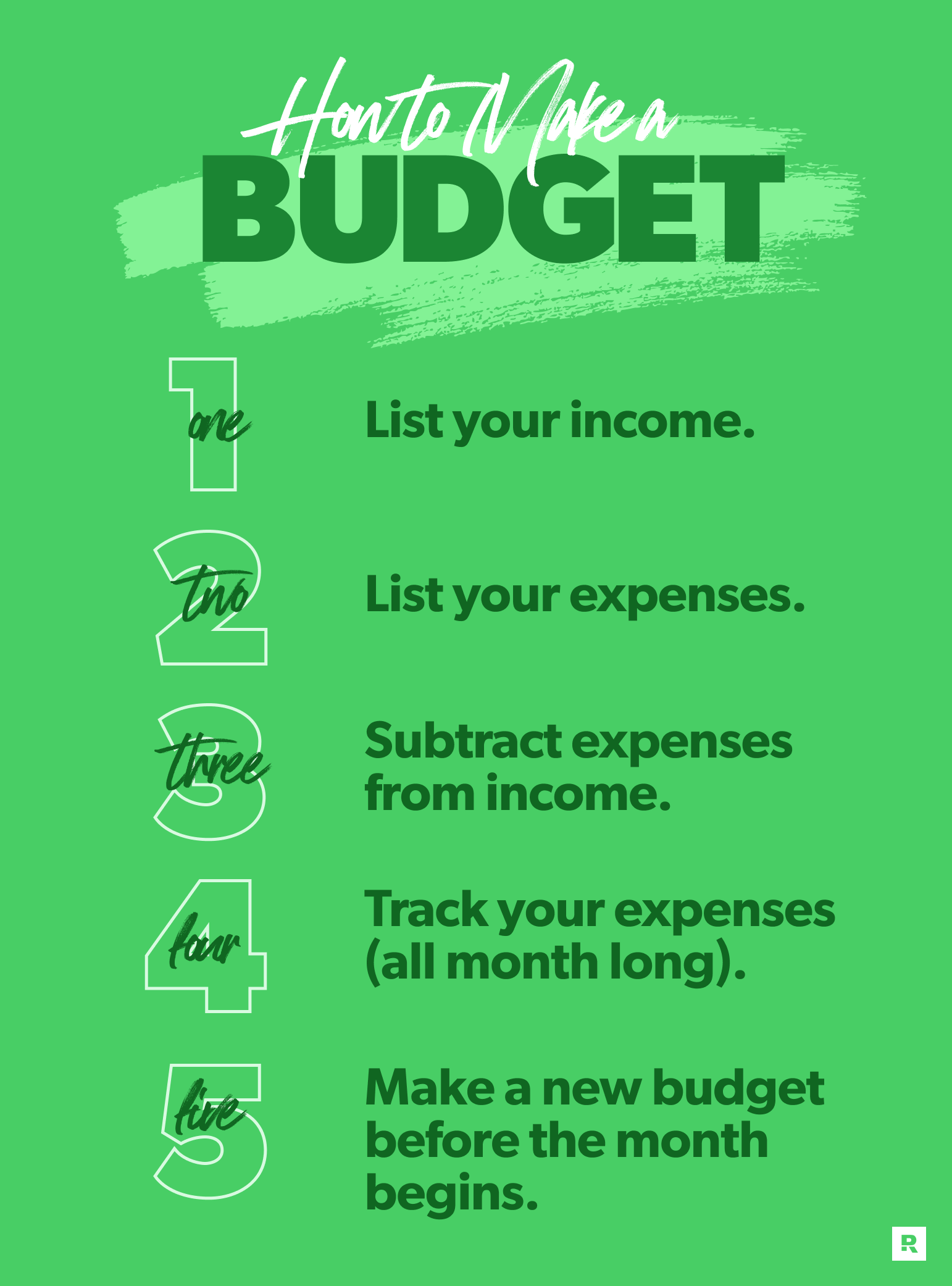

Before you can determine where your money should go, you must have an unflinching understanding of where it currently is. The foundational phase of budgeting involves a comprehensive audit of your financial reality.

Calculating Your True Net Income

The most common mistake in budgeting is basing a plan on a gross salary. To build a functional budget, you must calculate your net income—the amount that actually hits your bank account after taxes, health insurance premiums, and retirement contributions. If you are a freelancer or a gig economy worker, this requires a more nuanced approach, involving an average of your past six to twelve months of earnings and setting aside a percentage for self-employment taxes.

Identifying Fixed vs. Variable Expenses

Once your income is established, you must categorize your outflows. Fixed expenses are the non-negotiable costs that remain relatively constant each month, such as rent or mortgage payments, car insurance, and subscription services. Variable expenses, on the other hand, fluctuate based on behavior. These include groceries, utility bills, dining out, and entertainment. Distinguishing between these two is critical because variable expenses are the primary “levers” you can pull to find extra savings.

The Power of Tracking Spending Habits

A theoretical budget rarely survives contact with reality without a tracking period. Before finalizing your budget, spend 30 days recording every single transaction. This practice reveals “leaking” capital—small, recurring purchases that do not seem significant in isolation but accumulate into substantial monthly outflows. Whether you use a dedicated ledger or a digital tracking tool, this data is the raw material from which a successful budget is built.

Choosing the Right Budgeting Framework

There is no one-size-fits-all approach to financial planning. The effectiveness of a budget depends heavily on your personality, your financial goals, and your level of discipline. Here are three of the most effective frameworks used by financial professionals.

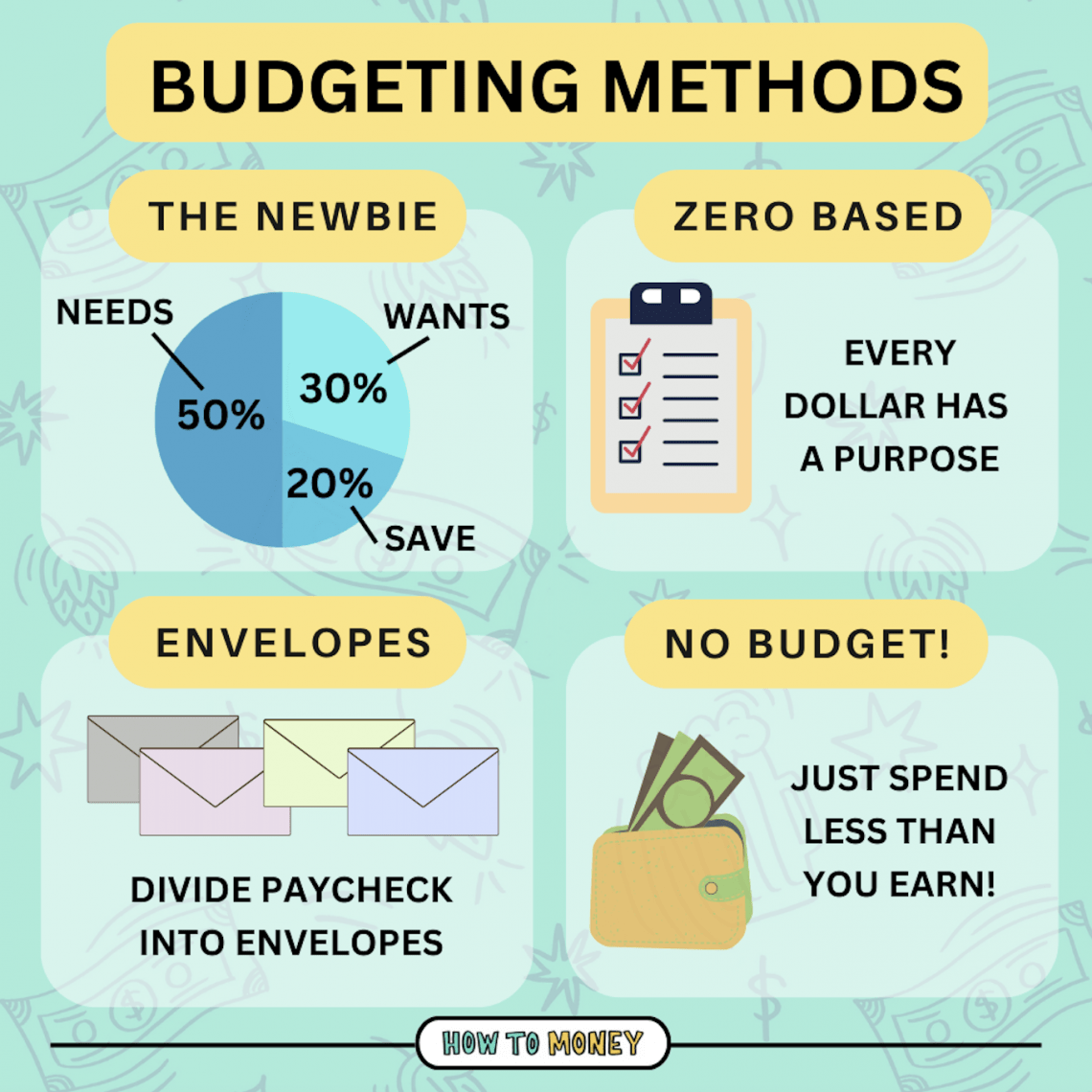

The 50/30/20 Rule

Popularized by Senator Elizabeth Warren, this is perhaps the most intuitive framework for beginners. It suggests allocating 50% of your net income to “Needs” (housing, utilities, basic groceries), 30% to “Wants” (hobbies, vacations, dining out), and 20% to “Financial Goals” (debt repayment, savings, and investments). This system provides a high-level overview of your priorities and ensures that you are living within your means while still building a future.

Zero-Based Budgeting

Zero-based budgeting is a more rigorous method where every dollar you earn is assigned a specific job. If you earn $5,000 a month, your expenses, savings, and debt payments must equal exactly $5,000 by the end of the month. This does not mean you have zero dollars in your bank account; rather, it means you have proactively decided where every cent goes. This method is highly effective for those who find themselves wondering where their money went at the end of the month.

The Envelope System and Digital Equivalents

For those who struggle with overspending in specific categories, the envelope system is a classic solution. You allocate a set amount of cash for categories like “Dining” or “Clothing” into physical envelopes. Once the money is gone, you cannot spend more in that category until the next month. In our increasingly cashless society, many “digital envelope” tools now allow users to create virtual buckets within their accounts, providing the same psychological barriers against overspending without the need for physical currency.

Strategic Debt Management and Savings Integration

A budget is not just about covering expenses; it is about growth. To move from financial stability to financial freedom, your budget must prioritize the elimination of liabilities and the accumulation of assets.

Building and Protecting Your Emergency Fund

The first financial goal integrated into any budget should be an emergency fund. Financial experts generally recommend saving three to six months of essential living expenses. This fund acts as a buffer against life’s unpredictability—medical emergencies, sudden job loss, or urgent home repairs. By budgeting for this fund as a “fixed expense,” you ensure that a temporary setback does not derail your long-term financial health.

Prioritizing High-Interest Debt

Debt is a significant drag on wealth creation. When building your budget, you must decide on a debt-repayment strategy. The “Debt Avalanche” method focuses on paying off debts with the highest interest rates first, which mathematically saves the most money over time. Alternatively, the “Debt Snowball” method focuses on paying off the smallest balances first to create psychological momentum. Whichever method you choose, the payment must be a non-negotiable line item in your monthly budget.

Automating Long-Term Investing

The ultimate goal of budgeting is to create a surplus that can be invested. Whether it is a 401(k), an IRA, or a brokerage account, the most effective way to ensure consistent investing is automation. By treating your investment contributions as a monthly “bill” that must be paid to your future self, you remove the temptation to spend that surplus on lifestyle inflation. Over time, the compound interest generated from these budgeted contributions becomes a powerful engine for wealth.

Leveraging Modern Financial Tools and Professional Strategies

In the modern era, you do not have to rely on a pencil and paper to manage your finances. A variety of tools can help streamline the process and provide deeper insights into your financial health.

The Role of Automated Budgeting Applications

Many people fail at budgeting because the manual entry of data becomes tedious. Automated apps sync directly with your bank accounts and credit cards, categorizing your transactions in real-time. These tools provide visual representations of your spending trends, helping you identify areas where you are exceeding your limits. However, the key to success with these tools is active engagement; an app can track your money, but it cannot make the decision to stop spending for you.

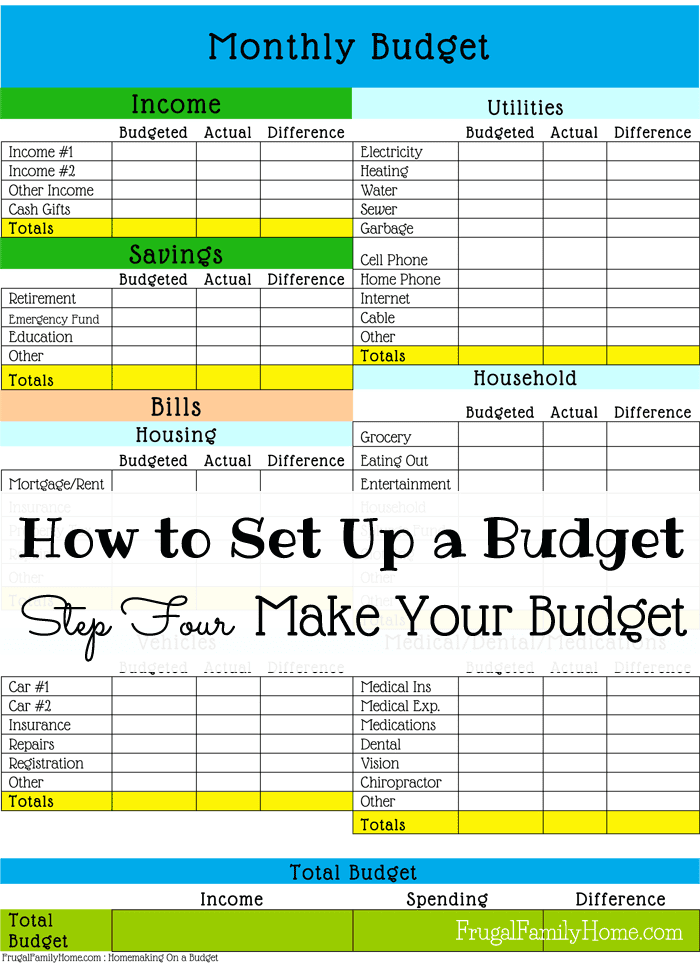

Utilizing Spreadsheets for Customization

For those who want absolute control, spreadsheets (such as Excel or Google Sheets) remain the gold standard. A spreadsheet allows you to build a custom dashboard that reflects your unique financial situation. You can create complex formulas to project future wealth, track your net worth over time, and simulate different financial scenarios (e.g., “What happens to my retirement date if I increase my savings by 5%?”).

Conducting Monthly Financial Audits

Budgeting is not a “set it and forget it” activity. It is a living document. At the end of each month, you should conduct a “financial audit.” Compare your actual spending against your budgeted amounts. If you consistently overspend in one category, you may need to adjust your expectations or your behavior. Likewise, if you have a surplus, you can strategically reallocate it toward your highest-priority financial goal.

Maintaining Consistency and Overcoming Common Pitfalls

The hardest part of budgeting is not the math—it is the discipline. To stay on track, you must anticipate the psychological and practical challenges that often lead to “budget burnout.”

Planning for “Sinking Funds”

One of the most common reasons budgets fail is the “unexpected” expense that was actually predictable. Annual car registrations, holiday gifts, and quarterly insurance premiums often catch people off guard. To solve this, use “sinking funds.” Calculate the total annual cost of these items, divide by 12, and include that amount in your monthly budget. By the time the bill arrives, the money is already sitting in your account.

Managing Lifestyle Creep

As your income increases through raises or side hustles, it is tempting to increase your standard of living proportionally. This is known as “lifestyle creep.” A professional approach to budgeting suggests that a significant portion of any income increase should be directed toward savings and investments rather than new expenses. This ensures that your wealth grows faster than your consumption.

Developing a Financial Growth Mindset

Ultimately, the most successful budgeters are those who view their budget as a tool for growth rather than a punishment. Instead of thinking “I can’t spend money on that,” think “I am choosing to spend my money on my freedom and my future.” This shift in perspective transforms the budget from a chore into a powerful instrument of personal agency. By consistently applying these principles, you will not only answer the question of how to make a budget, but you will also master the art of building a secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.