Car insurance is often viewed through the lens of legal compliance—a necessary hurdle to clear before driving a new vehicle off the lot. However, from a professional financial perspective, auto insurance is one of the most critical components of a robust risk management strategy. It serves as a financial hedge against catastrophic loss, protecting not just your vehicle, but your entire net worth and future earning potential.

Understanding how to get insurance for a car is less about finding the “cheapest” policy and more about optimizing your personal balance sheet. In this guide, we will explore the nuances of securing coverage through a financial lens, ensuring that your policy provides the maximum utility for every dollar spent.

Understanding the Financial Mechanics of Auto Insurance

Before venturing into the marketplace, it is essential to understand the underlying financial mechanics of an insurance policy. At its core, insurance is the transfer of risk from an individual to a larger pool in exchange for a premium. To make an informed decision, you must determine how much risk you are willing to retain and how much you need to outsource.

Assessing Liability, Collision, and Comprehensive Coverage

The “big three” components of car insurance represent different types of financial protection. Liability coverage is perhaps the most vital; it protects your assets from lawsuits if you are found at fault in an accident. In the context of personal finance, a “state minimum” policy is rarely sufficient for anyone with significant assets or savings.

Collision and comprehensive coverage, on the other hand, protect the asset itself—your car. Collision covers damage from accidents, while comprehensive covers non-collision events like theft or natural disasters. From a wealth-management perspective, if your vehicle’s market value is low enough that you could easily replace it out of pocket, you might consider “self-insuring” by dropping these coverages to save on premiums.

The Relationship Between Deductibles and Premiums

The deductible is the amount you pay out of pocket before insurance kicks in. In financial terms, this is your “risk retention” level. Choosing a higher deductible (e.g., $1,000 instead of $250) significantly lowers your monthly or annual premium. For individuals with a healthy emergency fund, opting for a higher deductible is often the more efficient financial move, as it reduces the “fixed cost” of the policy over the long term.

The Role of Uninsured and Underinsured Motorist Protection

While you may be financially responsible, others on the road may not be. Uninsured/Underinsured Motorist (UM/UIM) coverage is a defensive financial tool. It ensures that if you are hit by a driver who lacks adequate insurance, your own policy will cover your medical expenses and loss of income. This is essentially insurance for your own human capital, protecting your ability to earn a living if you are sidelined by an accident.

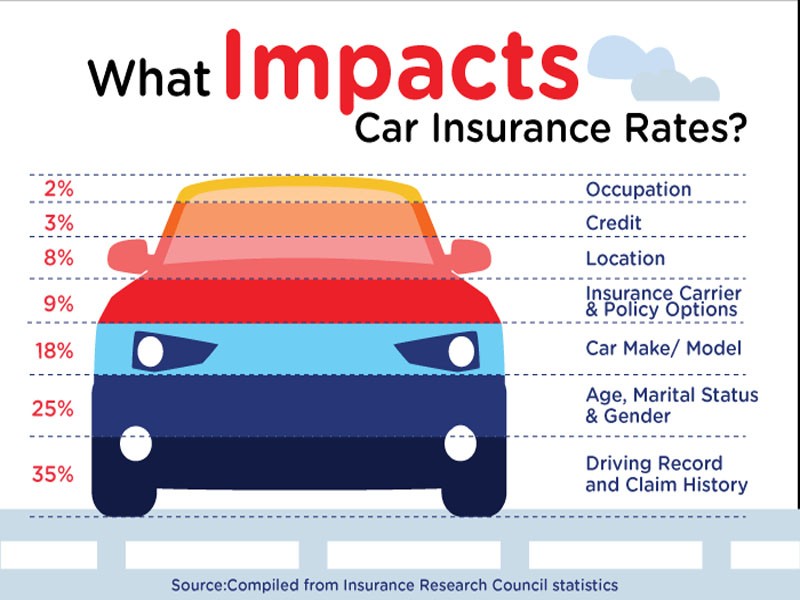

Factors Influencing Your Insurance Premiums and Financial Profile

In the eyes of an insurance provider, you are a data point. Actuaries use hundreds of variables to determine the likelihood that you will cost the company money. Understanding these factors allows you to position yourself as a “low-risk” asset, thereby securing better rates.

Credit Scores and Financial Reliability

In many jurisdictions, your credit-based insurance score is a major factor in determining your premium. Statistically, individuals who manage their finances responsibly tend to be more cautious drivers. Maintaining a high credit score is not just beneficial for mortgage rates; it is a direct lever for reducing insurance costs. If your credit has improved since you last shopped for insurance, re-evaluating your policy could lead to significant annual savings.

Asset Valuation and Depreciation

The type of car you drive dictates the “replacement cost” the insurance company faces. High-performance luxury vehicles are not only expensive to repair but are often associated with higher-risk driving behavior. When purchasing a car, it is wise to run a “Total Cost of Ownership” (TCO) analysis. A car that appears affordable at the dealership may become a financial burden once the insurance premiums—driven by the vehicle’s specific risk profile—are factored in.

Geographic and Demographic Risk Variables

Where you “park” your money—and your car—matters. Zip codes with high rates of theft or traffic congestion carry higher premiums. While you may not move just to save on car insurance, being aware of these variables helps in budgeting. Similarly, life stages (such as getting married or reaching age 25) often trigger a “de-risking” in the eyes of insurers, leading to lower rates.

Strategic Steps to Securing the Best Market Rate

Securing insurance is a procurement process. Like any business transaction, it requires diligence, comparison, and negotiation to ensure you are receiving the best value for your capital.

Comparison Shopping and Market Diligence

The insurance market is highly fragmented, and prices for the exact same coverage can vary by hundreds of dollars between carriers. To optimize your spend, you should obtain at least three to five quotes. Utilizing independent agents can be a strategic advantage; unlike captive agents who work for one company, independent agents can scan the entire market to find the best fit for your specific financial profile.

Leveraging Discounts and Policy Bundling

Most insurance companies offer “multi-line” discounts. By bundling your car insurance with homeowners or renters insurance, you create a “sticky” relationship with the provider, which they reward with lower rates. Additionally, look for “affinity discounts”—reductions based on your profession (e.g., educators, engineers, military), your alma mater, or memberships in professional organizations. These are essentially “loyalty points” for your financial reputation.

The Financial Impact of Usage-Based Insurance (UBI)

The rise of “Telematics” has introduced a new way to price risk. By allowing an insurer to track your driving habits via a mobile app or plug-in device, you can receive a premium based on actual performance rather than general statistics. For low-mileage drivers or exceptionally cautious ones, this “pay-how-you-drive” model can result in savings of 20% to 40%, directly increasing your monthly cash flow.

Integrating Insurance into Your Broader Financial Portfolio

Car insurance should not exist in a vacuum. It must be integrated into your overall financial plan, serving as a shield for your assets and a component of your long-term wealth-building strategy.

Protecting Your Net Worth from Liability Claims

As your net worth grows, your exposure to “litigation risk” increases. A standard auto policy might top out at $300,000 or $500,000 in liability coverage. For a high-net-worth individual, a single major accident could exceed these limits, putting personal investments and home equity at risk. In this scenario, the move is to secure an “Umbrella Policy.” This provides an extra layer of liability protection (often in $1 million increments) that kicks in after your auto policy is exhausted. It is one of the most cost-effective ways to protect a growing portfolio.

Reviewing Coverage as Life Milestones Occur

A financial plan is not static, and neither should be your insurance. Major life events—buying a home, having a child, or retiring—change your risk profile and your insurance needs. For instance, if you transition to remote work, your annual mileage will drop significantly. Failing to report this to your insurer is essentially leaving money on the table. A semi-annual “insurance audit” ensures that your coverage levels still align with your current financial reality.

The Opportunity Cost of Insurance Premiums

Finally, consider the opportunity cost. Every dollar spent on an inefficient insurance policy is a dollar that could have been invested in a brokerage account or a retirement fund. By aggressively shopping for the best rates and optimizing your deductibles, you free up capital for wealth-building activities. Over a 30-year driving career, the difference between an optimized insurance strategy and a “set-it-and-forget-it” approach can amount to tens of thousands of dollars in lost investment potential.

In conclusion, getting insurance for a car is a sophisticated financial exercise. It requires an understanding of risk, an eye for market opportunities, and a commitment to protecting one’s broader economic interests. By treating your auto policy as a strategic financial asset rather than a mere monthly bill, you ensure that you are protected on the road and on your path to financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.