In the realm of personal finance and wealth management, data is the compass that guides every strategic move. Whether you are evaluating the annual yield of a high-interest savings account, calculating the impact of inflation on your purchasing power, or determining the precise allocation of assets within a diversified portfolio, one mathematical concept reigns supreme: the percentage. While modern financial software and AI-driven apps handle much of the heavy lifting, the ability to manually calculate percentages on a standard or financial calculator remains a fundamental skill for any savvy investor or budget-conscious professional.

Understanding how to calculate percentages is not merely about arithmetic; it is about interpreting the velocity of your money. A 5% return on a $10,000 investment represents a different strategic milestone than a 5% interest rate on a $10,000 credit card debt. To navigate these waters effectively, one must master the tool at hand—the calculator—to transform raw figures into actionable financial intelligence.

The Role of Percentages in Personal Finance and Investment

Percentages are the universal language of finance. They allow investors to compare apples to oranges, such as comparing the performance of a volatile tech stock against a stable government bond. Without the context of percentages, nominal figures can be misleading.

Understanding the Time Value of Money

The concept of the Time Value of Money (TVM) is rooted in percentage-based growth. When you look at a calculator to determine your future wealth, you are essentially calculating the compounding effect of a percentage over time. A small difference in percentage—say, between a 7% and an 8% annual return—can result in a difference of hundreds of thousands of dollars over a thirty-year career. By mastering percentage calculations, you can visualize how small adjustments in your savings rate or interest yields can exponentially alter your financial trajectory.

Evaluating Investment Performance

Investors use percentages to calculate Return on Investment (ROI). This is the most critical metric for determining whether a capital allocation was successful. If you buy a property for $200,000 and sell it for $250,000, the $50,000 profit is a nominal win. However, by using your calculator to find that this represents a 25% gain, you can then compare that performance against the S&P 500 or other benchmarks. This comparison is the hallmark of professional-grade financial management.

Essential Techniques: Using Your Calculator for Standard Financial Computations

While every calculator varies slightly—from the basic four-function device to the sophisticated scientific or financial models—the logic of percentage remains constant. Understanding the underlying formulas ensures that you aren’t just pushing buttons, but rather directing a financial outcome.

The Direct Percentage Key Method

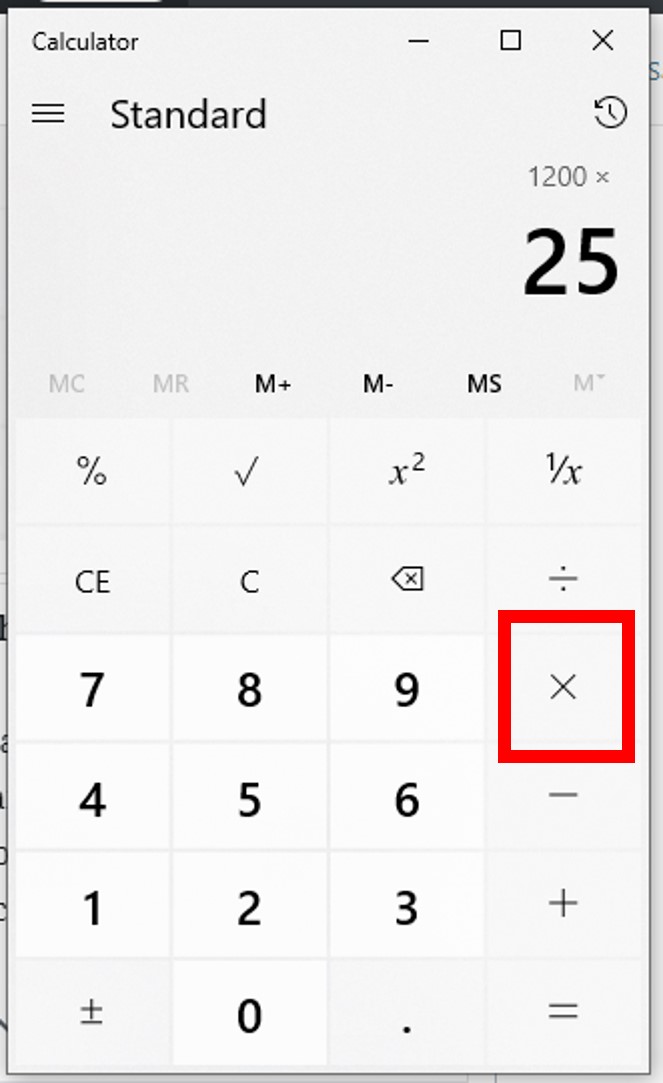

Most standard and smartphone calculators include a dedicated percentage (%) key. To find a specific percentage of a total (for example, finding 15% of a $1,200 monthly dividend), the process is straightforward:

- Enter the total amount ($1,200).

- Press the multiplication (×) key.

- Enter the percentage rate (15).

- Press the percentage (%) key.

- Press equals (=).

The calculator automatically converts the “15” into “0.15” and performs the multiplication. This is the quickest way to calculate sales tax, tips, or immediate interest accrual.

Calculating Discounts and Markups Manually

In business finance, you often need to calculate the “net” after a discount or the “gross” after a markup. If a side hustle generates a product that costs $50 to make and you want a 40% profit margin, you must calculate the markup.

To do this without a dedicated profit margin button:

- For a Discount: Multiply the original price by (1 – decimal percentage). For a 20% discount on a $100 item: $100 × 0.80 = $80.

- For a Markup: Multiply the cost by (1 + decimal percentage). For a 40% markup on a $50 item: $50 × 1.40 = $70.

Finding the Percentage Change (Profit and Loss)

To calculate the percentage increase or decrease in an asset’s value—such as a stock price moving from $150 to $185—you use the “New minus Old divided by Old” formula.

- Enter the new value (185).

- Subtract the original value (150) to get the nominal gain (35).

- Divide that result by the original value (150).

- Multiply by 100.

In this case, $(35 / 150) times 100 = 23.33%$. This tells the investor that their capital has grown by over 23%, a vital metric for portfolio rebalancing.

Advanced Financial Tools: Beyond the Basic Calculator

As your financial journey matures, a simple handheld calculator may give way to more robust tools. However, the logic remains the same; the tools simply allow for more variables like time, frequency of compounding, and inflation adjustments.

Utilizing Financial Calculators for Compound Interest

For serious debt repayment or retirement planning, a dedicated financial calculator (like the TI-BAII Plus) is invaluable. These devices have specific buttons for N (number of periods), I/Y (interest rate per year), and PV/FV (present and future value). When calculating percentages here, you are often looking for the “effective” interest rate. For example, if a loan has a 12% nominal annual rate but compounds monthly, the calculator helps you find that the “Effective Annual Rate” (EAR) is actually 12.68%. Understanding this percentage gap can save an individual thousands in interest payments.

Digital Spreadsheets and Automated Calculations

In the modern office, Microsoft Excel or Google Sheets are the ultimate financial calculators. Using the formula = (B2-A2)/A2 and formatting the cell as a “Percentage” allows for the mass processing of financial data. This is particularly useful for “Side Hustle” entrepreneurs who need to track monthly revenue growth percentages across multiple product lines simultaneously. It moves the user from “calculating a number” to “analyzing a trend.”

Common Pitfalls and How to Avoid Calculation Errors

Financial ruin is often found in the decimal points. A simple error in how a percentage is entered can lead to a misunderstanding of one’s net worth or tax liability.

Distinguishing Between Gross and Net Percentages

A common mistake in business finance is confusing “markup” with “margin.” If you buy an item for $70 and sell it for $100, that is a $30 profit. On a calculator, many people see that $30 is 42.8% of $70 (the cost) and call it a 42% margin. However, profit margin is calculated based on the selling price. In reality, $30 is 30% of $100. Miscalculating this percentage can lead a business owner to believe their profit margins are healthier than they actually are, leading to overspending and eventual cash flow crises.

The Danger of Compounding Errors in Long-term Planning

When using a calculator to project 20 or 30 years into the future, even a 0.5% error in your assumed inflation rate or expense ratio can result in a massive discrepancy in your final numbers. This is why financial professionals often perform “sensitivity analysis”—calculating the same scenario at 4%, 5%, and 6%—to understand the range of possible outcomes. Always double-check your inputs; ensure you are dividing by the “original” value, not the “new” value, when seeking a percentage of growth.

Strategic Application: Turning Calculations into Financial Growth

Once you are comfortable with the “how” of percentage calculation, you can move toward the “why.” Using these figures strategically is what separates those who simply “save money” from those who “build wealth.”

Budgeting with the 50/30/20 Rule

One of the most effective personal finance frameworks is the 50/30/20 rule. Using your calculator, you take your net take-home pay and apply these percentages:

- 50% to Needs: Housing, utilities, groceries.

- 30% to Wants: Dining out, hobbies, entertainment.

- 20% to Savings and Debt Repayment: Building the future.

If your calculator shows that your “Needs” are consuming 65% of your income, you have a mathematical mandate to either reduce costs or increase your income. The percentage provides the clarity needed for discipline.

Debt Management and Interest Rate Optimization

For those carrying multiple debts, the calculator is a weapon for liberation. By calculating the percentage of interest paid on each debt (the APR), you can prioritize payments using the “Avalanche Method.” By focusing all extra capital on the debt with the highest interest percentage—rather than the highest balance—you minimize the total amount of money “lost” to the bank.

In conclusion, knowing how to calculate a percentage on a calculator is more than a basic math skill; it is a foundational pillar of financial literacy. By mastering these calculations, you empower yourself to see past the marketing jargon of financial institutions, evaluate your investment opportunities with clinical precision, and steer your personal economy toward long-term prosperity. Whether it is a 1% fee on a mutual fund or a 20% growth in a side business, every percentage point matters in the pursuit of financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.