In the intricate landscape of personal finance, particularly when navigating the waters of higher education funding, certain terms emerge as critical signposts. Among these, the “Master Promissory Note” (MPN) stands out as a foundational document for millions of borrowers. Far from being just another piece of paperwork, an MPN is a legally binding agreement that commits a borrower to repay a loan, often spanning multiple disbursements or even multiple academic years, under specific terms and conditions. Understanding its nature, implications, and proper management is paramount for anyone venturing into significant borrowing, especially within the realm of federal student aid.

At its core, the MPN serves as a borrower’s formal promise to repay money borrowed, along with any accrued interest and fees, to the lender. While promissory notes are common across various financial transactions, the “master” aspect signifies its ability to cover more than one loan. This streamlined approach, particularly prevalent in federal student loan programs, simplifies the borrowing process by allowing a single agreement to facilitate subsequent loan disbursements without the need for a new note each time. However, this convenience also places a greater onus on the borrower to fully comprehend the long-term commitment they are undertaking.

Understanding the Basics of a Master Promissory Note

To truly grasp the significance of an MPN, it’s essential to break down its fundamental components and recognize its primary applications. It’s more than just a signature; it’s an agreement that shapes a borrower’s financial future for years, if not decades.

Defining the MPN: A Legal Commitment

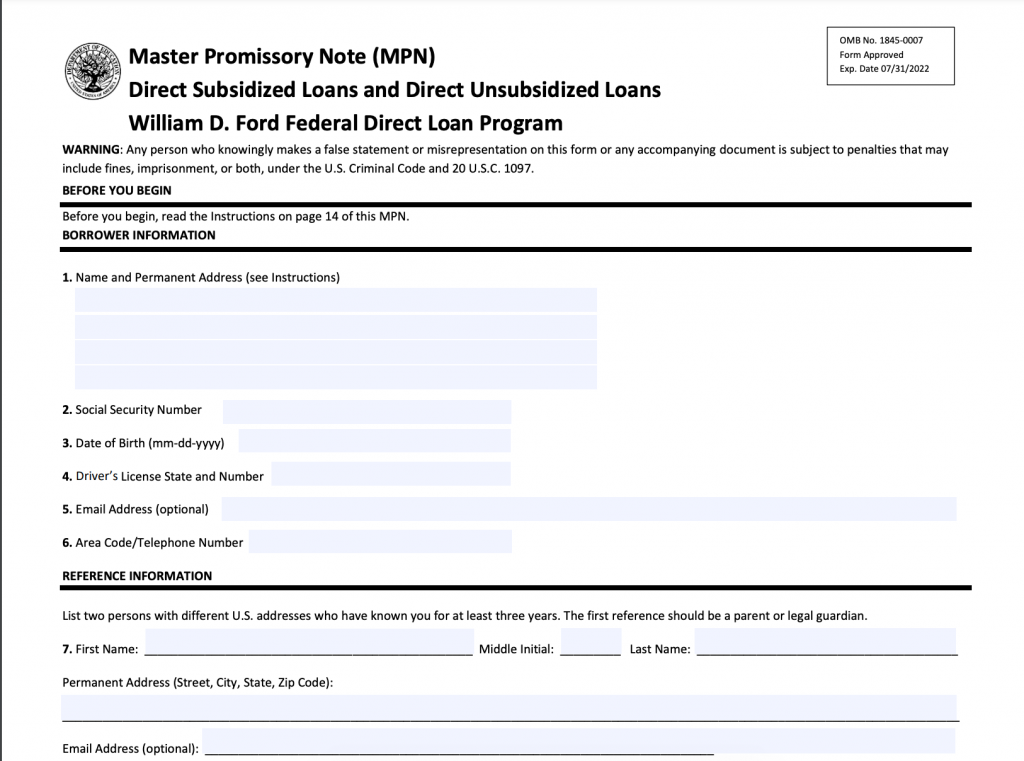

A Master Promissory Note is a written legal document wherein a borrower promises to repay a specific sum of money, borrowed for a specified purpose (like education), under clearly defined terms. Unlike a traditional promissory note that might be tied to a single, one-off loan, an MPN is designed for ongoing borrowing. This means that once signed, it can be used by your school to disburse multiple federal student loans over time—typically for up to 10 years for Direct Subsidized/Unsubsidized Loans, or for a single academic year for PLUS Loans (though a new MPN might be required annually for PLUS loans depending on the lender/servicer).

The legal weight of an MPN cannot be overstated. By signing, you are not merely acknowledging receipt of funds; you are entering into a contractual agreement. This contract outlines your responsibilities, such as making timely payments, and the lender’s rights, including the ability to pursue collection efforts if you default. It contains crucial details that dictate the terms of your repayment, making it a cornerstone of your financial obligation.

Who Uses an MPN? The Federal Student Loan Landscape

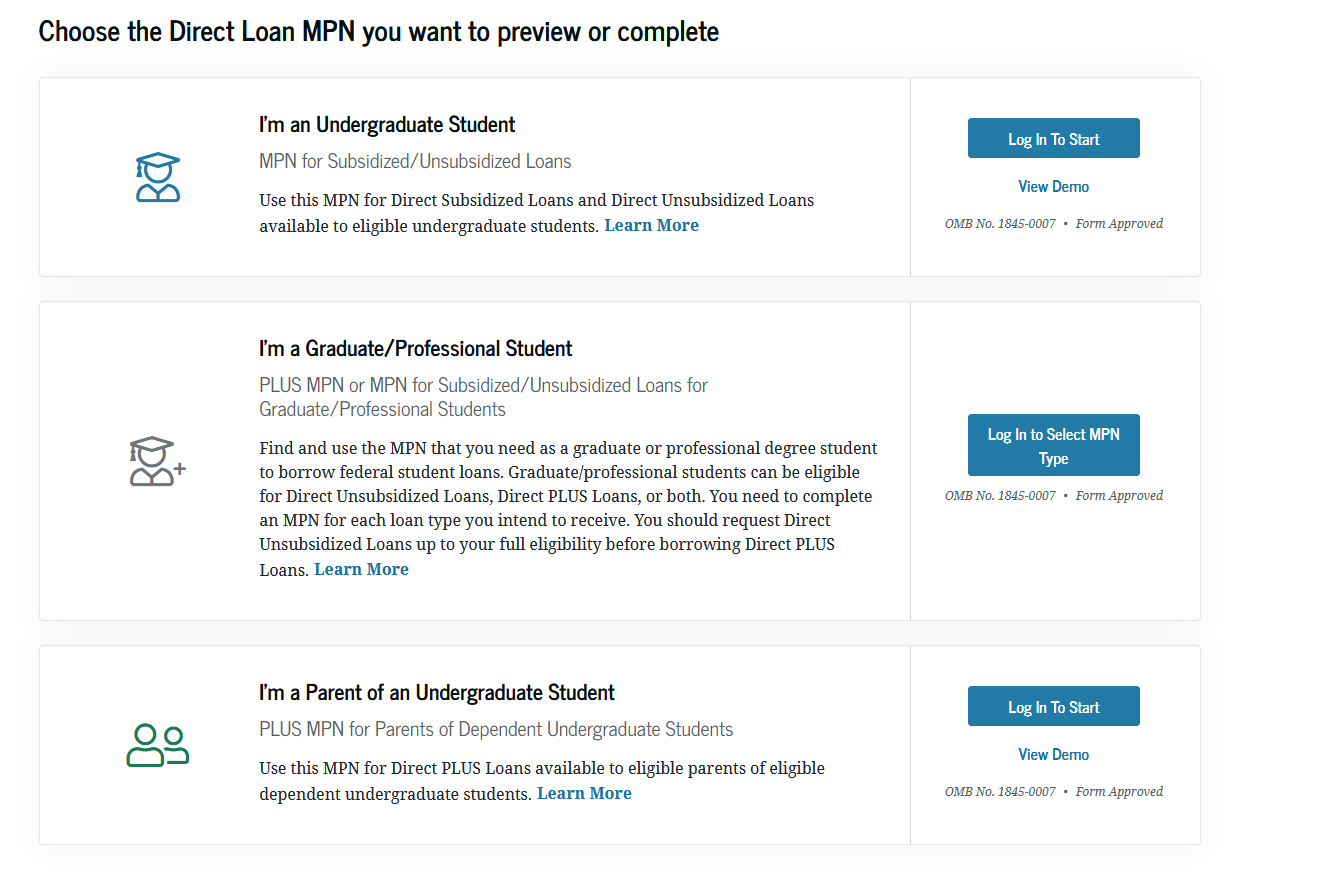

The most prominent users of the MPN are borrowers of federal student loans. If you’ve ever applied for financial aid through the Free Application for Federal Student Aid (FAFSA) and received federal student loans, chances are you’ve signed an MPN. Specifically, MPNs are required for:

- Direct Subsidized Loans: For undergraduate students with demonstrated financial need.

- Direct Unsubsidized Loans: For undergraduate and graduate students, regardless of financial need.

- Direct PLUS Loans: For graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS) to help pay for education expenses not covered by other financial aid.

While private student loans also utilize promissory notes, they typically do not employ the “master” format to the same extent as federal loans. This distinction highlights the unique, government-backed structure of federal student aid, which seeks to streamline the administrative burden for both students and institutions.

Key Components of an MPN: What You’re Agreeing To

Before signing any legal document, especially one with long-term financial implications, it’s imperative to understand its contents. An MPN typically includes several critical pieces of information:

- Borrower’s Information: Your full legal name, Social Security number, date of birth, and contact information.

- School Information: The institution you plan to attend and receive funds from.

- Lender/Servicer Information: Details about the Department of Education as the lender and the specific loan servicer assigned to manage your loan account.

- Maximum Loan Amount: For Direct Subsidized/Unsubsidized Loans, the MPN usually covers the aggregate maximum loan amount you can receive over your academic career, rather than a specific dollar figure for a single disbursement. For PLUS Loans, it often specifies a maximum annual amount.

- Interest Rates: While not always a fixed number on the MPN itself (as rates can change annually for federal loans), it will outline how interest is calculated and applied.

- Repayment Terms: This section details when repayment begins (e.g., after a grace period), the standard repayment period (typically 10 years for federal loans), and available repayment plans (standard, graduated, extended, income-driven).

- Borrower’s Rights and Responsibilities: This crucial section informs you about your right to cancel a loan disbursement, deferment and forbearance options, eligibility for loan forgiveness, and your responsibility to notify your servicer of changes (e.g., address, enrollment status).

- Consequences of Default: A clear explanation of what happens if you fail to repay your loan, including damage to credit, wage garnishment, and tax refund offsets.

- References: For federal student loans, you’ll typically need to provide two references who have known you for a specified period and have different U.S. addresses. These references are used to help locate you if you fail to respond to communications about your loan.

The Process of Signing a Master Promissory Note

The act of signing an MPN is more than a formality; it’s a critical step in securing financial aid. Understanding the process helps ensure that borrowers are fully prepared and informed.

When and Where to Sign: Navigating the Online Portal

The process of signing an MPN typically occurs after you have completed your FAFSA, received your financial aid offer from your chosen school, and decided to accept federal student loans. For federal loans, the MPN is usually signed electronically via the U.S. Department of Education’s website, StudentAid.gov.

Once you log in with your FSA ID (Federal Student Aid ID), you will navigate to the section for completing the MPN. The platform guides you through each section, prompting you to read and acknowledge the terms. It’s designed to be user-friendly, but the ease of the process should not overshadow the gravity of the commitment. You’ll typically complete the MPN only once for Direct Subsidized/Unsubsidized Loans, and it remains valid for up to 10 years, meaning your school can use it for future loan disbursements within that timeframe without requiring a new one. For Direct PLUS Loans, while an MPN can cover multiple years, some schools or lenders may require a new MPN annually, particularly if there are changes in your creditworthiness or if you’re a parent PLUS borrower.

What Information Do You Need? Preparing for the Commitment

To complete the MPN, you’ll need several pieces of information ready:

- Your FSA ID: This serves as your electronic signature for federal student aid documents.

- Personal Information: Your Social Security number, date of birth, current address, and phone number.

- School Information: The name of the school you plan to attend.

- Two References: As mentioned, these individuals should have different addresses and know you well. They are not co-signers and are not financially responsible for your loan. Their purpose is purely for contact in case the loan servicer cannot reach you.

It’s crucial to provide accurate and up-to-date information. Any discrepancies could delay the processing of your loans.

Understanding Your Rights and Responsibilities: Before You Sign

Before digitally signing the MPN, you are presented with extensive information regarding your rights and responsibilities. This is not boilerplate text to be skipped. It details crucial aspects such as:

- Right to Cancel: You have the right to cancel all or part of a loan disbursement within a specified timeframe (typically 30 days after disbursement) without incurring any interest or fees.

- Grace Period: The period after you leave school or drop below half-time enrollment before you must begin making payments.

- Deferment and Forbearance: Conditions under which you can temporarily postpone or reduce your loan payments due to specific circumstances like unemployment, economic hardship, or military service.

- Loan Forgiveness/Discharge: Situations where you might be eligible for your loans to be partially or entirely forgiven (e.g., Public Service Loan Forgiveness, Total and Permanent Disability Discharge).

- Responsibility to Repay: The fundamental commitment to repay the loan according to the terms, even if you don’t complete your education or are dissatisfied with your school.

- Notification Requirements: Your obligation to inform your loan servicer if you change your address, name, enrollment status, or transfer schools.

Failing to read and understand these terms can lead to significant financial distress down the line. It’s a critical step in financial literacy for any borrower.

Advantages and Disadvantages of an MPN

The design of the MPN offers both conveniences and potential pitfalls that borrowers should be acutely aware of.

Streamlined Borrowing Process: Reducing Red Tape

The primary advantage of the MPN, especially for federal student loans, is its ability to streamline the borrowing process. Instead of signing a new promissory note each time you receive a loan disbursement (e.g., each semester or academic year), one MPN can cover multiple loans over an extended period. This reduces administrative paperwork for both the borrower and the financial aid office, making the process of receiving funds smoother and more efficient. It allows students to focus more on their studies and less on repetitive bureaucratic tasks.

Long-Term Commitment: Stability vs. Oversight

Another benefit is the long-term validity of the MPN. For federal Direct Subsidized and Unsubsidized Loans, an MPN can be valid for up to 10 years. This means you may only need to sign it once throughout your undergraduate and even graduate studies, assuming you continue to meet eligibility requirements and attend a participating school. This provides a degree of stability and predictability in your loan acquisition process.

Potential Pitfalls: The Illusion of “Free Money” and Debt Accumulation

Despite its conveniences, the MPN structure presents potential drawbacks, primarily revolving around the ease with which multiple loans can be accumulated under a single agreement. Because you’re not signing a new document each year, the “out of sight, out of mind” phenomenon can set in. Borrowers might lose track of the total amount of debt they are accumulating, mistakenly viewing subsequent disbursements as less significant than the initial one. This can lead to a dangerous disconnect between the perceived cost of education and the actual loan burden.

Without the annual reminder of signing a new promissory note, some borrowers may become less diligent in reviewing their loan statements or understanding their aggregate debt. This lack of active engagement can result in shock upon entering repayment when the full scope of their financial obligation becomes apparent. It underscores the critical importance of actively tracking your loan balances and understanding that each disbursement, though covered by the same MPN, adds to your total principal and interest.

Beyond the Basics: Managing Your MPN and Loans

Signing an MPN is just the beginning of your financial journey. Effective management of your student loans requires ongoing vigilance and proactive engagement.

Tracking Your Loan Information: The National Student Loan Data System (NSLDS)

To avoid the pitfalls of overlooked debt, it’s crucial to regularly monitor your loan portfolio. The National Student Loan Data System (NSLDS) is the U.S. Department of Education’s central database for federal student aid. It provides a comprehensive view of all your federal student loans and grants, including:

- Lender and loan servicer contact information

- Loan types and amounts

- Disbursement dates

- Current status (e.g., in-school, grace, repayment)

- Interest rates

- Outstanding balances

Regularly checking your NSLDS record (accessible via StudentAid.gov) is the single most effective way to stay informed about your federal student loan obligations.

Repayment Options and Strategies: Tailoring Your Approach

The MPN outlines standard repayment terms, but federal student loans offer a variety of repayment plans designed to accommodate different financial situations. Understanding these options is key to successful repayment:

- Standard Repayment Plan: Fixed payments over 10 years (or 10 to 30 years for consolidated loans).

- Graduated Repayment Plan: Payments start low and increase every two years.

- Extended Repayment Plan: Lower payments over up to 25 years for borrowers with more than $30,000 in direct loans.

- Income-Driven Repayment (IDR) Plans: Payments are based on your income and family size, typically capping payments at 10-20% of your discretionary income. Any remaining balance after 20 or 25 years (depending on the plan) may be forgiven, though it might be taxable.

Choosing the right repayment plan can significantly impact your monthly budget and overall financial health.

Deferment, Forbearance, and Loan Forgiveness: Understanding Relief Options

Life is unpredictable, and federal student loans offer safety nets for borrowers facing financial hardship:

- Deferment: Allows you to temporarily postpone payments, and in some cases (like subsidized loans), interest does not accrue during this period. Common reasons include enrollment in school, unemployment, economic hardship, or military service.

- Forbearance: Also allows temporary postponement or reduction of payments, but interest typically accrues on all loan types during forbearance. It’s often granted when you don’t qualify for deferment but are experiencing temporary financial difficulty.

- Loan Forgiveness/Discharge: Certain programs, like Public Service Loan Forgiveness (PSLF) for those in qualifying public service jobs, or discharge options for total and permanent disability, can eliminate all or part of your loan balance. Eligibility criteria are strict, so understanding them upfront is important.

These options provide crucial flexibility, but they should be used strategically, as they often extend the loan term and can increase the total interest paid.

Importance of Financial Literacy: Beyond the Signature

Ultimately, the Master Promissory Note is a gateway to funding your education, but it also serves as an early lesson in financial responsibility. Developing strong financial literacy skills—understanding budgeting, managing debt, grasping the power of compound interest, and avoiding default—is vital. Engaging with your loan servicer, staying informed about your loan terms, and making proactive decisions about your repayment strategy will empower you to manage your student loan debt effectively and avoid potential pitfalls.

In conclusion, the Master Promissory Note is a deceptively simple document that holds significant long-term financial weight. While it streamlines the process of securing federal student aid, it places a substantial responsibility on the borrower to understand their commitment, track their accumulating debt, and plan for repayment. By treating the MPN with the seriousness it deserves and actively managing their loan portfolio, borrowers can leverage student loans to achieve their educational aspirations without succumbing to overwhelming debt.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.