For members of the Reserve and National Guard, the transition from active drilling status to civilian life—or even moving between periods of active duty and reserve status—is marked by a specific set of administrative hurdles. While many see military discharge papers as mere bureaucratic proof of service, in the world of personal finance and wealth management, these documents are essentially high-value keys. They are the primary instruments used to unlock a suite of financial products, tax advantages, and investment opportunities that are unavailable to the general public.

In the context of personal finance and business strategy, understanding exactly “what discharge papers reservists get” is the first step in maximizing one’s net worth after service. These documents serve as the ultimate “verification of eligibility” for multi-billion dollar federal and state programs. This guide explores the specific papers reservists receive and, more importantly, how to leverage them to build long-term financial security.

The Essential Documentation: DD-214 vs. NGB-22

The most common point of confusion for reservists is that, unlike their active-duty counterparts, they may receive several different types of discharge or separation papers depending on the nature of their service. From a financial planning perspective, knowing which document you hold determines which “financial buckets” you can tap into.

The DD Form 214: The Gold Standard for Federal Benefits

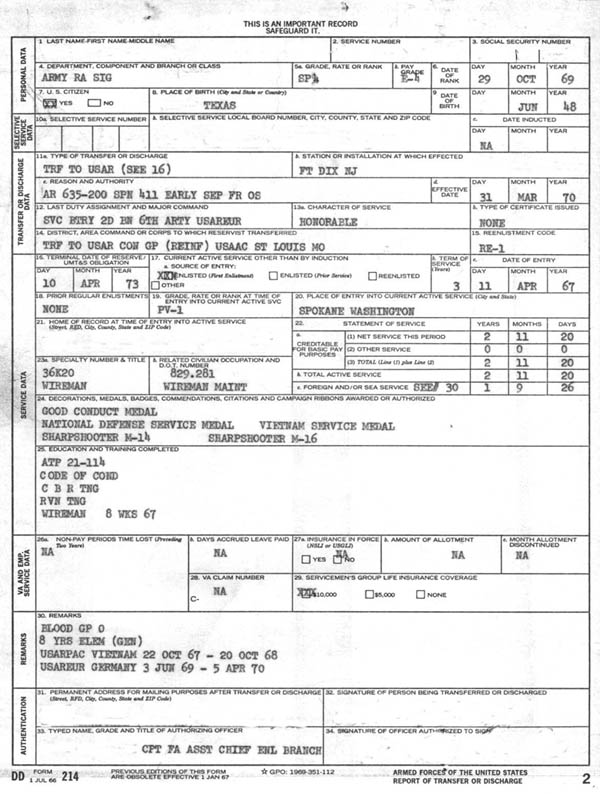

The Certificate of Release or Discharge from Active Duty, known as the DD-214, is the most recognizable document in the military. For a reservist, a DD-214 is generally only issued after a period of active duty service lasting 90 days or more (such as a deployment or specialized training).

Financially, the DD-214 is your passport to the Department of Veterans Affairs (VA) ecosystem. Whether you are applying for a mortgage with no down payment or seeking to lower your interest rates through a streamline refinance, the DD-214 is the primary proof of service required by lenders. It details your “Character of Service,” which must typically be “Honorable” or “Under Honorable Conditions” to qualify for the most lucrative financial incentives.

NGB Form 22 and Discharge Certificates

For members of the National Guard, the NGB Form 22 (Report of Separation and Record of Service) serves a similar purpose to the DD-214 but is issued by the specific state’s military department. For “pure” reservists who may not have been activated for a long enough duration to receive a DD-214, the DD Form 256 (Honorable Discharge Certificate) or the Reserve Component Points Statement becomes the foundational document for financial verification.

From an investment standpoint, these papers are used to prove “years of service” for retirement pay. Because reservists operate on a “points system,” these discharge papers are the only way to audit your retirement account with the Defense Finance and Accounting Service (DFAS) to ensure your future pension reflects your actual time served.

Leveraging Service Papers for Real Estate and Wealth Building

One of the most powerful wealth-building tools available to reservists is the VA Home Loan program. However, getting a Certificate of Eligibility (COE) for this program requires specific discharge documentation.

The VA Loan: A Zero-Down Investment Strategy

For many Americans, the biggest barrier to entry in the real estate market is the 20% down payment. For a $400,000 home, that is $80,000 in liquid capital. A reservist with the correct discharge papers (showing at least six years of service in the Selected Reserve or 90 days of active duty) can bypass this requirement entirely.

By using a VA loan, a reservist can keep that $80,000 invested in the stock market or a high-yield savings account, earning compound interest, while simultaneously building equity in a real estate asset. Furthermore, VA loans do not require Private Mortgage Insurance (PMI), which can save the borrower hundreds of dollars per month—capital that can be redirected into a Roth IRA or a brokerage account.

Real Estate Portfolio Expansion

Strategic reservists often use their discharge papers to engage in “house hacking.” This involves using a VA loan to purchase a multi-unit property (up to four units), living in one, and renting out the others. The discharge papers prove the eligibility for the low-interest, zero-down loan, while the rental income covers the mortgage and generates positive cash flow. This is one of the fastest ways for a veteran to transition from a service member to a real estate investor.

Educational Capital: Funding a Career Pivot and Skill Acquisition

Personal finance isn’t just about saving and investing; it’s about increasing your “human capital” or earning potential. The discharge papers a reservist receives are the gatekeepers to massive educational subsidies.

The Montgomery GI Bill – Selected Reserve (MGIB-SR)

Reservists who have a six-year obligation in the Selected Reserve and have completed initial active duty for training are eligible for the MGIB-SR (Chapter 1606). To access these funds, you typically need your Notice of Basic Eligibility (NOBE), which is often issued alongside or in place of standard discharge papers during a transition.

This benefit provides a monthly stipend for up to 36 months. For a reservist looking to transition into tech, finance, or high-level management, this tax-free money can pay for certifications, coding boot camps, or a master’s degree, significantly increasing their market value in the civilian sector.

Post-9/11 GI Bill and Residual Value

If a reservist was activated for at least 90 days, they likely qualify for a percentage of the Post-9/11 GI Bill. This is arguably the most valuable financial asset a reservist can possess. Beyond tuition and fees, it provides a Monthly Housing Allowance (BAH) based on the cost of living in the school’s zip code.

From a financial planning perspective, the Post-9/11 GI Bill allows a reservist to pursue a career change without dipping into their savings or taking on student debt. In the world of finance, avoiding a 7% interest rate on a $50,000 student loan is functionally the same as earning a 7% guaranteed return on investment.

Entrepreneurship and Business Financing for Reservists

For the reservist who wants to move away from the “W-2” lifestyle and into business ownership, discharge papers are essential for accessing specialized business capital and government contracts.

SBA Veteran Advantage Loans

The Small Business Administration (SBA) offers the “SBA Express” loan program, which features reduced fees for veterans and reservists. To qualify, you must present your DD-214 or other discharge papers to prove your status. These loans can be used for working capital, equipment purchases, or real estate acquisition for a business. Lowering the cost of capital is a critical factor in the success of a startup, and the “Veteran” status verified by discharge papers provides a distinct competitive advantage.

Veteran-Owned Small Business (VOSB) Certification

In the world of corporate and government contracting, being a Certified Veteran-Owned Small Business (VOSB) or a Service-Disabled Veteran-Owned Small Business (SDVOSB) opens doors to “set-aside” contracts. The federal government has a goal to award a certain percentage of all federal contracting dollars to veteran-owned businesses. Your discharge papers are the primary evidence required for this certification. This is a direct pipeline to revenue that non-veteran competitors cannot access, creating a protected niche for your business to grow.

Long-term Wealth Management and Retirement Planning

Finally, discharge papers play a crucial role in calculating and securing long-term retirement benefits, which are a cornerstone of any comprehensive financial plan.

Converting Service Time into Federal Retirement Credits

If a reservist moves into a federal civilian job (GS-level positions), they can “buy back” their military time to count toward their civilian FERS retirement. This is a powerful financial move that can allow a veteran to retire years earlier with a higher pension. However, this process is impossible without an accurate DD-214 or NGB-22 to verify the exact dates and nature of service.

The Reserve Retirement “Points” Audit

Unlike active duty members who retire after 20 years regardless of daily activity, reservists retire based on a points system. Your discharge papers, along with your final Points Statement, determine the size of your pension check starting at age 60 (or earlier if you had certain deployment periods).

In financial terms, this pension is an inflation-adjusted annuity. For a retired E-7 or O-4, the lifetime value of this pension, when adjusted for inflation and longevity, can easily exceed $1 million. Ensuring your discharge papers correctly reflect your service is the equivalent of auditing a million-dollar investment account. Missing points or unrecorded service periods can result in thousands of dollars of lost income every year during retirement.

Conclusion: The Paperwork of Prosperity

The discharge papers a reservist receives—whether it is the DD-214, the NGB-22, or the DD-256—are far more than a “thank you” for your service. They are financial instruments. From securing zero-down real estate to funding high-level education and launching a business, these documents are the foundation of a veteran’s personal wealth strategy.

By treating these papers with the same care one would treat a stock certificate or a deed to a property, reservists can ensure they are fully leveraging the economic advantages they earned through their service. In the modern economy, “thank you for your service” is a nice sentiment, but “here is your low-interest capital and tax-free education” is the reality that builds generational wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.