In the world of personal finance, few numbers carry as much weight as the average mortgage rate. For the aspiring homeowner, a fluctuation of even half a percentage point can mean the difference between an affordable monthly payment and a financial burden that limits long-term wealth accumulation. For the seasoned investor, mortgage rates are the pulse of the real estate market, dictating the feasibility of new acquisitions and the liquidity of existing portfolios.

Understanding what constitutes an “average” mortgage rate requires more than just looking at a daily ticker. It involves a deep dive into macroeconomic forces, personal financial health, and the structural mechanics of the banking industry. This article explores the intricate world of mortgage rates, providing the insights necessary to navigate one of the most significant financial decisions of your life.

The Mechanics of Mortgage Rates: What Drives the Numbers?

When people ask “what is the average mortgage rate,” they are usually referring to the 30-year fixed-rate mortgage, the gold standard of American home lending. However, this rate is not a static figure plucked from thin air; it is the result of a complex interplay of global and domestic economic factors.

The Role of the Federal Reserve

While the Federal Reserve does not directly set mortgage rates, its influence is paramount. The Fed sets the federal funds rate—the interest rate at which commercial banks borrow from each other overnight. When the Fed raises this rate to combat inflation, the cost of borrowing increases across the economy. Banks, in turn, pass these costs on to consumers in the form of higher interest rates for credit cards, auto loans, and mortgages. Conversely, when the Fed lowers rates to stimulate economic growth, mortgage rates typically follow suit, though not always in a perfect one-to-one ratio.

The 10-Year Treasury Yield and Mortgage-Backed Securities

A more direct correlation exists between mortgage rates and the 10-year Treasury yield. Most 30-year mortgages are paid off or refinanced within ten years. Therefore, investors view 10-year Treasury bonds and Mortgage-Backed Securities (MBS) as similar investment vehicles. When investors demand higher yields on Treasury bonds due to economic uncertainty or inflation fears, the yields on MBS must also rise to remain competitive. This “spread” between the 10-year yield and the 30-year mortgage rate is a critical metric for financial analysts.

Inflation and Purchasing Power

Inflation is perhaps the greatest enemy of a fixed-income investor. Because mortgage lenders are essentially lending a lump sum today to be paid back over 30 years, they must ensure the interest they charge accounts for the declining purchasing power of the dollar. High inflation expectations lead to higher mortgage rates as lenders seek to protect their future returns. When inflation is low and stable, lenders can afford to offer more competitive, lower rates.

Key Factors Influencing Your Personal Mortgage Rate

While the national “average” provides a baseline, the rate you are actually quoted by a lender will vary based on your specific financial profile. Lenders use a risk-based pricing model, meaning the more risk you represent, the higher the interest rate you will pay.

Credit Scores and Financial Health

Your FICO score is the single most influential factor in determining your mortgage rate. A borrower with a score above 760 is viewed as low-risk and will likely receive the lowest available rates. Conversely, a borrower with a score below 620 may face rates that are several percentage points higher—or may be denied a conventional loan altogether. Maintaining a clean credit history, low credit card utilization, and a history of on-time payments is the most effective way to secure a rate below the national average.

Loan-to-Value (LTV) Ratio and Down Payments

The amount of equity you have in the home significantly impacts the lender’s risk. A higher down payment—typically 20% or more—results in a lower Loan-to-Value (LTV) ratio. Lenders are more comfortable offering lower rates to borrowers who have more “skin in the game,” as these borrowers are statistically less likely to default on their obligations. Furthermore, an LTV above 80% usually requires Private Mortgage Insurance (PMI), which adds to the overall monthly cost even if the interest rate itself remains stable.

Choosing the Right Loan Product

The “average” rate differs significantly across various loan types.

- Fixed-Rate Mortgages: These offer stability, with the interest rate remaining constant over the life of the loan (usually 15 or 30 years).

- Adjustable-Rate Mortgages (ARMs): These often start with a lower “teaser” rate for a set period (e.g., 5 or 7 years) before adjusting annually based on market indices. ARMs can be beneficial in a falling-rate environment but carry significant risk if rates rise.

- Government-Backed Loans: FHA, VA, and USDA loans often have different rate structures and may offer lower rates for those who qualify, particularly for first-time buyers or veterans.

Historical Context: Average Rates Through the Decades

To understand today’s mortgage landscape, one must look backward. The “average” rate is only meaningful when compared to historical norms.

The High-Interest Era of the 1980s

For younger homebuyers, today’s rates may seem high, but a look at the early 1980s provides a sobering perspective. In October 1981, the average 30-year fixed mortgage rate peaked at an astounding 18.63%. This was a result of the Federal Reserve’s aggressive campaign to break the back of “Great Inflation.” During this era, “creative financing” and seller-financed deals were the only ways many Americans could afford to move.

The Post-2008 Low-Interest Decade

Following the 2008 financial crisis, the Federal Reserve entered a period of unprecedented monetary easing. This led to a decade of historically low mortgage rates, often hovering between 3% and 4.5%. This era culminated during the 2020-2021 pandemic period, where rates dropped to all-time lows below 3%. This created a “gold rush” in the housing market but also set the stage for the inventory shortages and price appreciation seen today.

The Current Economic Transition

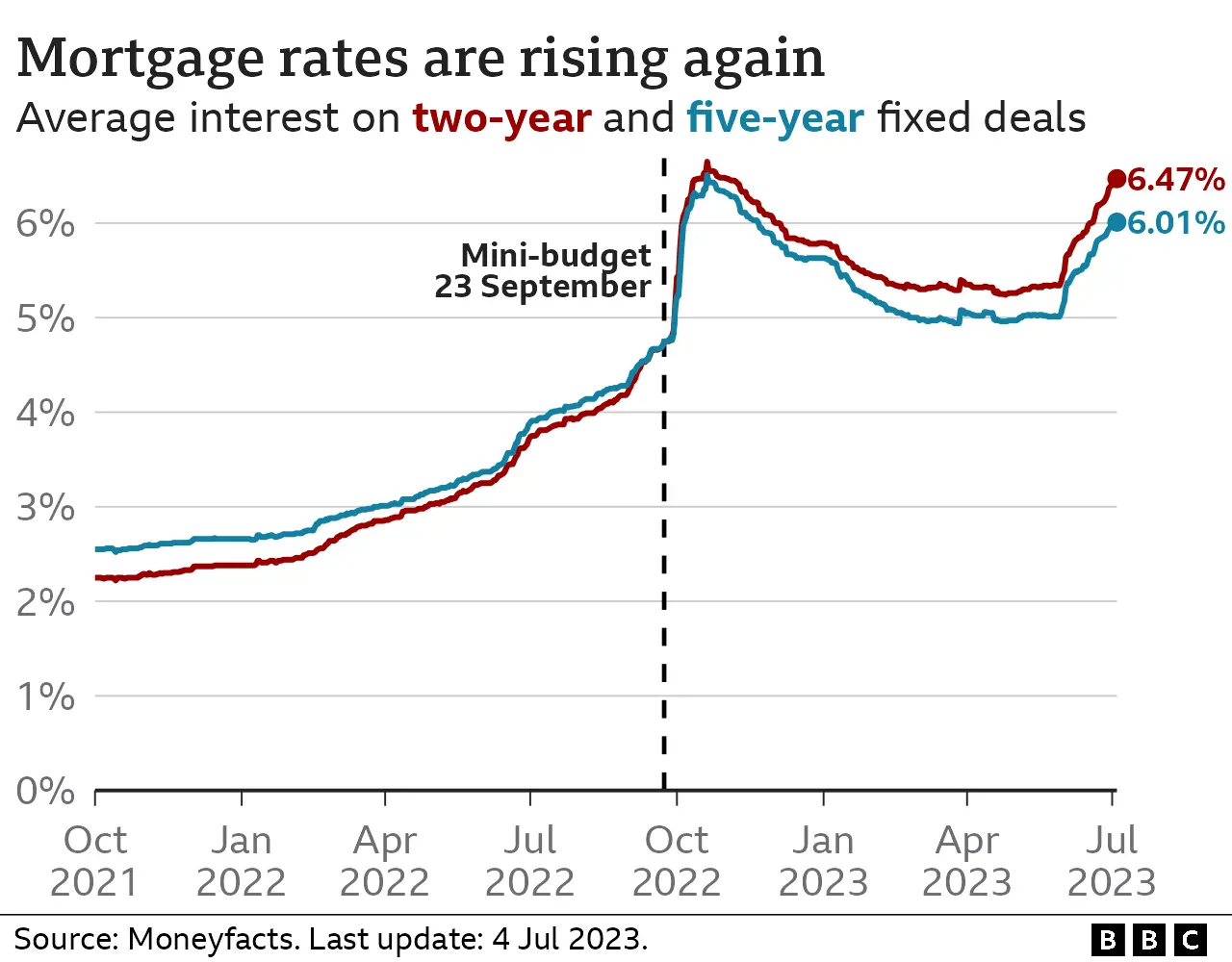

As the global economy adjusted to post-pandemic realities and supply chain disruptions, inflation surged, forcing central banks to hike rates rapidly. This shift brought mortgage rates from their historic lows back toward their long-term historical average (which is closer to 6-7%). Understanding that current rates are actually quite “normal” by historical standards can help buyers make more rational, less emotional decisions.

Strategies for Securing the Best Possible Rate

In a fluctuating market, savvy borrowers don’t just accept the first rate they are quoted. There are several strategic moves you can make to lower your long-term interest costs.

Comparison Shopping and the Power of Choice

One of the biggest mistakes borrowers make is only getting a quote from their primary bank. Studies have shown that getting at least three to five quotes from different lenders—including credit unions, online lenders, and traditional banks—can save a borrower thousands of dollars over the life of the loan. Each lender has different overhead costs and “appetite” for risk, which translates into varied pricing.

Buying Down the Rate with Discount Points

If you plan on staying in your home for a long time, “buying points” may be a wise financial move. One point typically costs 1% of the loan amount and reduces your interest rate by about 0.25%. This represents a trade-off: you pay more upfront at closing to secure a lower monthly payment for the next 30 years. Calculating the “break-even point”—the moment where the monthly savings exceed the initial cost of the points—is essential.

Timing the Market and Rate Locks

Mortgage rates can change multiple times in a single day based on economic news. Once you find a rate that fits your budget, utilizing a “rate lock” is crucial. A rate lock guarantees that your quoted interest rate won’t change between the time of your application and your closing, provided the loan closes within a specific window (usually 30 to 60 days). Some lenders also offer a “float-down” option, which allows you to snag a lower rate if market conditions improve before you close.

The Long-Term Financial Impact of Interest Rates

The difference between a 6% and a 7% interest rate may seem nominal, but when projected over 30 years, the financial implications are staggering.

Amortization and Total Interest Paid

On a $400,000 loan, the difference between a 6% and 7% rate is roughly $260 per month. Over the 30-year life of the loan, that 1% difference results in over $93,000 in additional interest payments. This is capital that could otherwise be directed toward retirement accounts, education funds, or other investment vehicles. Understanding this math reinforces why searching for the best rate is perhaps the highest-earning “side hustle” a person can undertake.

![]()

Refinancing: The Strategy of “Date the Rate, Marry the House”

A common mantra in high-rate environments is “Date the Rate, Marry the House.” This philosophy suggests that if you find a home you love, you should buy it despite current rates, with the intention of refinancing when rates eventually drop. While this is a viable strategy, it requires careful financial planning. Refinancing involves closing costs, and there is no guarantee that rates will drop significantly in the near future. A sound financial plan should always account for the possibility that the current rate may be the rate you keep for the long haul.

In conclusion, the average mortgage rate is a dynamic figure influenced by a tapestry of global economic trends and individual financial choices. By understanding the underlying drivers of these rates and taking proactive steps to optimize your financial profile, you can navigate the complexities of the housing market with confidence, ensuring that your home remains a pillar of your long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.