In the landscape of American economics, the term “poverty wage” is often used interchangeably with “minimum wage” or “low income,” yet it represents a much more specific and harrowing financial reality. For millions of workers across the country, the income earned through full-time labor fails to cover the basic necessities of modern life: housing, food, healthcare, and transportation.

Understanding the poverty wage in the U.S. requires moving beyond simple federal statistics and looking at the intersection of purchasing power, regional inflation, and the “living wage” threshold. As the cost of living continues to outpace wage growth in many sectors, the distinction between earning a paycheck and achieving financial security has never been more pronounced.

Defining the Poverty Wage: Federal Benchmarks vs. Economic Reality

To understand what constitutes a poverty wage, one must first look at the official metrics provided by the U.S. government. However, there is a significant disconnect between these administrative numbers and the actual cost of staying afloat in a modern economy.

The Federal Poverty Guidelines

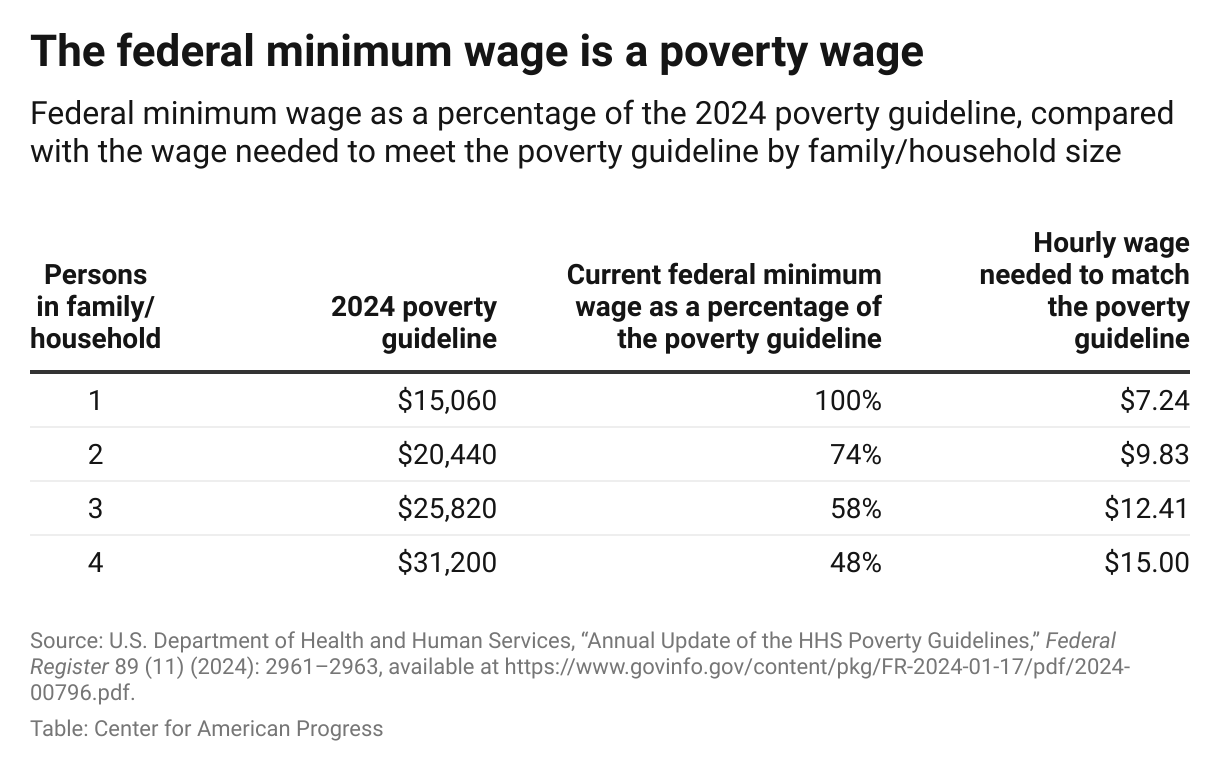

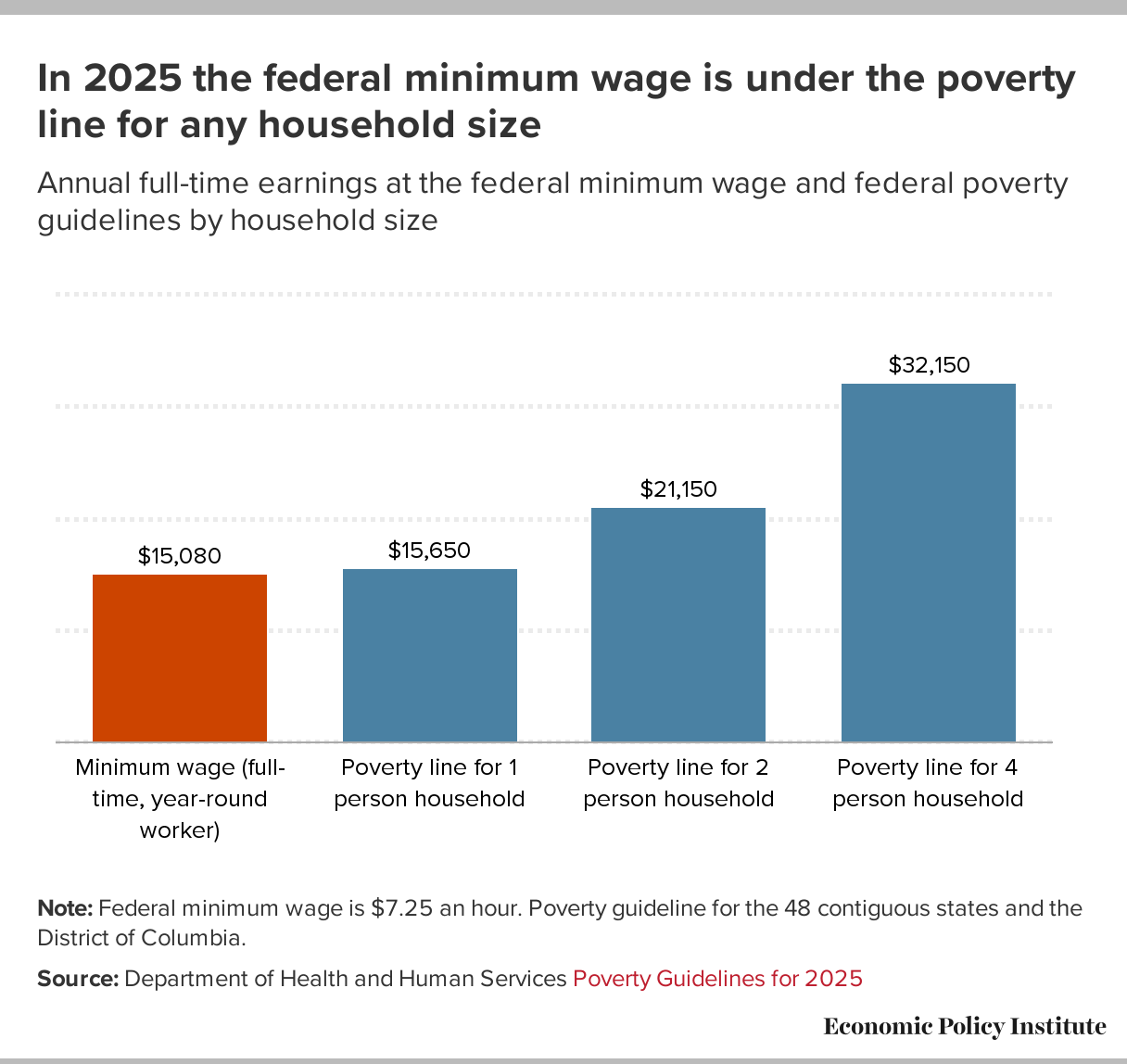

The U.S. Department of Health and Human Services (HHS) and the Census Bureau establish annual poverty guidelines. For 2024, the poverty guideline for a single individual is approximately $15,060 per year. For a family of four, it sits around $31,200. When calculated as an hourly rate for a full-time worker (2,080 hours per year), the “poverty wage” for an individual is roughly $7.24 per hour—almost exactly the current federal minimum wage of $7.25.

The issue with these guidelines is that they are based on a formula developed in the 1960s, which primarily calculated the cost of a minimum food diet and multiplied it by three. This formula fails to account for the meteoric rise in housing costs, childcare, and healthcare—expenses that now consume a much larger share of a household budget than food does.

The Minimum Wage Discrepancy

While the federal minimum wage has remained stagnant at $7.25 since 2009, many states have taken it upon themselves to raise the floor. However, even in states with a $15.00 minimum wage, many workers find themselves in “working poverty.” A poverty wage isn’t just a number below the federal line; it is any wage that keeps a worker in a cycle of debt and prevents the accumulation of any emergency savings. In many high-cost urban centers, a wage of $18 or $20 per hour can still function as a poverty wage if the local rent for a one-bedroom apartment exceeds 50% of the worker’s take-home pay.

The Cost of Living Crisis and the “Living Wage” Concept

Because federal poverty guidelines are often criticized for being outdated, economists and personal finance experts frequently point to the “Living Wage” as a more accurate counter-metric. A living wage is the minimum income necessary for a worker to meet their basic needs without resorting to public assistance or experiencing severe financial distress.

Regional Variances in Affordability

The primary reason a single “poverty wage” number is misleading is the vast geographic disparity in the U.S. economy. In rural Mississippi, a $15 hourly wage might provide a modest but stable life. In San Francisco, New York City, or Boston, that same $15 is effectively a poverty wage.

The “Self-Sufficiency Standard,” a measure used by many non-profits and economic researchers, suggests that in most U.S. counties, a single adult needs at least $35,000 to $45,000 annually just to cover the basics. When we look at families with children, that number often doubles due to the exorbitant cost of childcare, which in many states now exceeds the cost of a college tuition.

The MIT Living Wage Calculator as a Benchmark

The Massachusetts Institute of Technology (MIT) maintains one of the most respected tools for tracking these needs. Their data consistently shows that the “poverty wage”—if defined as the wage needed to avoid a deficit at the end of the month—is significantly higher than the federal minimum. According to their 2023–2024 data, the living wage for a family of four (two working adults, two children) in the United States is roughly $25.02 per hour, per person. This highlights a massive gap between what the government considers “poverty” and what the economy requires for “survival.”

Economic Factors Influencing the Poverty Threshold

Several macroeconomic factors contribute to the persistence of poverty wages and the erosion of the middle class. For the individual looking at their personal finances, these factors are the invisible “taxes” on their hourly earnings.

Inflation and Purchasing Power

Inflation is the most direct enemy of the low-wage worker. When the prices of essential goods—milk, eggs, gasoline, and utilities—rise, those earning a poverty wage feel the impact immediately. Unlike high-income earners who can absorb price increases by reducing their savings rate, low-wage workers have no buffer.

Over the last decade, while nominal wages have risen in some sectors, “real wages” (wages adjusted for inflation) have remained largely flat for the bottom 20% of earners. This means that while a worker might see a raise from $12 to $15 an hour, their ability to buy a gallon of gas or pay for a doctor’s visit has not actually improved.

The “Benefits Cliff” and Financial Traps

A unique and cruel aspect of the poverty wage in the U.S. is the “benefits cliff.” This occurs when a worker receives a small raise that pushes them just above the income threshold for public assistance programs like SNAP (food stamps) or Medicaid.

For example, a $1.00 per hour raise might result in an extra $160 of pre-tax income per month, but it could trigger the loss of $400 in childcare subsidies or food assistance. This creates a financial trap where earning a slightly higher “poverty wage” actually leaves the individual worse off, discouraging upward mobility and making it nearly impossible to bridge the gap toward a true living wage.

Strategies for Navigating Low-Income Challenges

For individuals currently earning at or near the poverty wage, personal finance takes on a different meaning. It is less about “investing in the stock market” and more about “mitigating disaster” and “strategic upskilling.”

Upskilling and Career Pivots

In the modern economy, the most effective way to escape a poverty wage is through targeted skill acquisition. This doesn’t necessarily mean a four-year degree, which often comes with debt that exacerbates financial instability. Instead, many are turning to:

- Trade Schools: Electrical, plumbing, and HVAC roles often start well above the living wage.

- Certifications: In the tech and administrative sectors, specific certifications (like CompTIA for IT or specialized medical billing) can provide an immediate $5–$10 per hour bump.

- Micro-credentials: Short-term programs designed to provide specific, high-demand skills in logistics, manufacturing, or digital services.

Financial Tools for Budgeting on a Tight Income

When every dollar is spoken for, financial management requires precision. Those stuck in the low-wage cycle can benefit from specific financial tools designed for volatility:

- Neobanks with Early Payday: Apps that allow workers to access their paychecks two days early can help avoid predatory payday loans.

- Microsavings Apps: Tools that round up transactions to the nearest dollar can help build a tiny “emergency buffer” that, while small, might prevent a missed utility payment.

- Zero-Based Budgeting: This method, where every single cent of income is assigned a “job” (rent, food, debt), is essential for those living on a poverty wage to ensure that essential costs are covered before any discretionary spending occurs.

The Corporate and Policy Outlook

The conversation around the poverty wage is not just an individual one; it is a corporate and systemic issue. As more businesses recognize that “financial wellness” contributes to employee retention and productivity, the landscape is slowly shifting.

The Shift Toward Fair Pay

A growing number of corporations are adopting “Socially Responsible” (ESG) frameworks that include commitments to paying a living wage rather than a poverty wage. These companies recognize that high turnover—often caused by workers being unable to afford transportation or stable housing—is more expensive in the long run than paying a higher hourly rate.

Legislative Efforts and Future Projections

On the policy front, there is continued pressure to index the federal minimum wage to inflation. If the minimum wage had kept pace with worker productivity since the 1960s, it would be over $20 per hour today. While a federal change remains politically contentious, the movement toward a “living wage” is gaining momentum at the municipal level.

In conclusion, the “poverty wage” in the U.S. is a moving target. While the government may define it as roughly $7.25 to $15.00 per hour depending on the context, the economic reality is that in most of the country, any wage under $20 per hour for a head of household is a struggle against the tide. Achieving true financial stability requires a combination of systemic policy reform, corporate responsibility, and individual financial strategy to bridge the gap between surviving and thriving.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.