In the world of personal finance and wealth building, real estate remains one of the most reliable pillars for long-term growth. However, the efficiency of the real estate market doesn’t happen by accident. Behind every “For Sale” sign and every digital listing lies a complex, high-stakes infrastructure known as the Multiple Listing Service, or MLS. For the average investor, homeowner, or financial enthusiast, understanding the MLS is not just about knowing where houses are listed; it is about understanding the primary data source that dictates market value, liquidity, and investment potential.

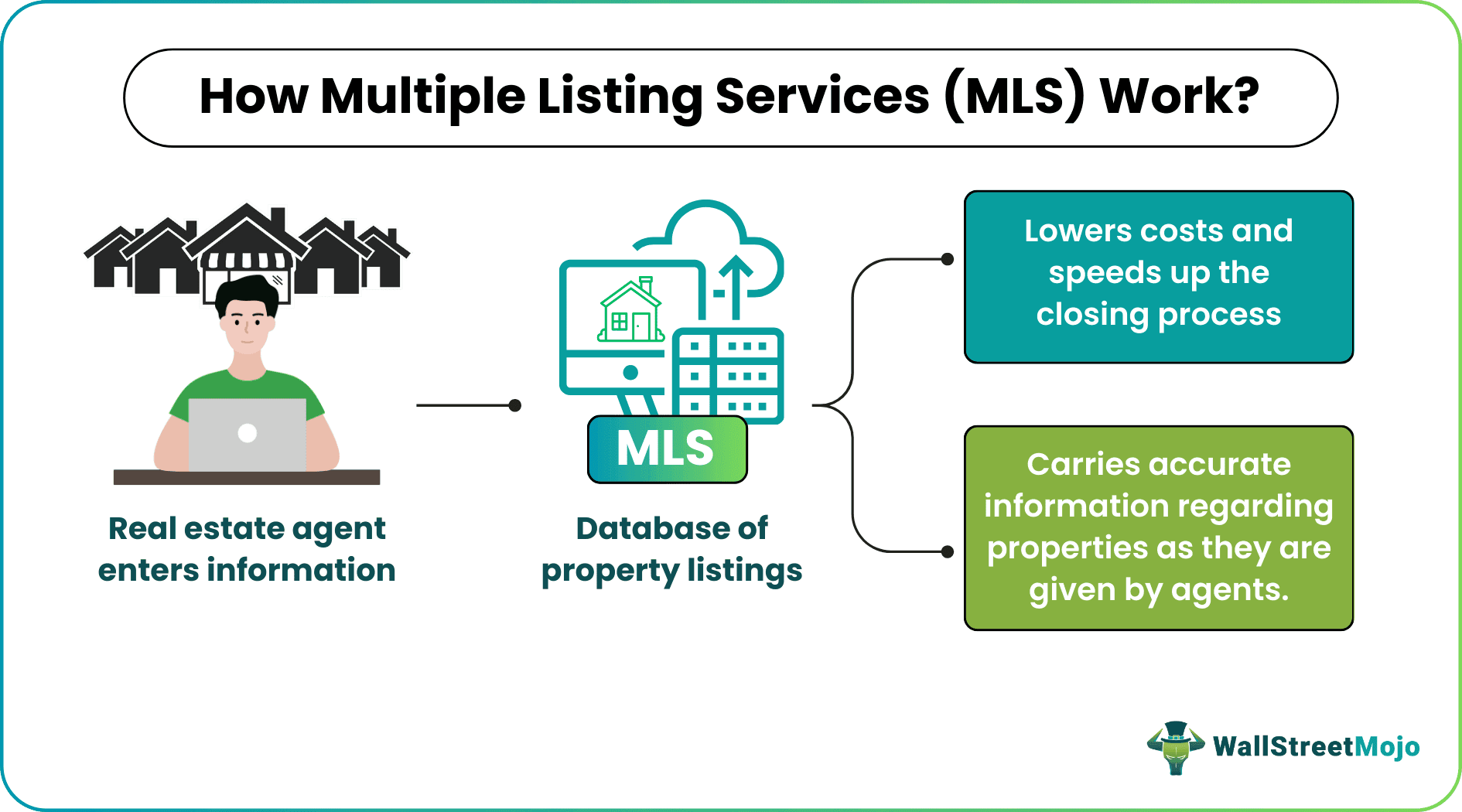

The MLS is far more than a simple website. It is a suite of private databases used by real estate professionals to share information about properties for sale. By centralizing data, the MLS creates an efficient marketplace that benefits both buyers and sellers, ensuring that financial transactions are based on accurate, real-time information rather than guesswork.

Understanding the Multiple Listing Service (MLS) as a Financial Ecosystem

To understand what the MLS is from a financial perspective, one must look at it as a mechanism for market liquidity. In any financial market—whether it is the New York Stock Exchange or a local real estate pocket—liquidity refers to the ease with which an asset can be turned into cash without a significant loss in value. The MLS is the tool that provides this liquidity to the housing market.

The Definition and Origin of the MLS

The concept of the MLS dates back to the late 19th century. Real estate brokers would gather at the offices of their local associations to share information about the properties they were trying to sell. They agreed to compensate other brokers who helped find a buyer. This “broker cooperation” model was revolutionary because it shifted the industry from a fragmented collection of individual salespeople into a cohesive, synchronized network.

Today, the MLS is a digital powerhouse. It is not a single national database, but rather a collection of approximately 600 regional databases across the United States. Each regional MLS is governed by local boards of Realtors and is designed to ensure that every participant has access to the same high-quality data.

How the MLS Facilitates Market Liquidity

In a market without an MLS, a seller would have to rely solely on their individual broker’s network. If that broker didn’t know the right buyer, the house could sit on the market for years, or the seller might be forced to accept a much lower price.

By using the MLS, a listing is instantly broadcast to thousands of other professionals who represent active buyers. This massive exposure creates a competitive environment. From a “Money” perspective, competition is the driver of fair market value. When more eyes are on a property, the price discovered through the bidding process is much more likely to represent the true financial value of the asset.

The Role of MLS in Real Estate Investing and Personal Finance

For anyone focused on personal finance or professional investing, the MLS is the “Golden Record” of data. While consumer-facing apps have made browsing for homes a hobby, the professional MLS remains the source of truth that informs serious financial decisions.

Accessing Accurate Data for Valuation

One of the most critical steps in any financial investment is valuation—determining exactly what an asset is worth. In real estate, this is done through “Comparables” or “Comps.”

The MLS provides detailed information that public sites often lack or delay, such as:

- Original Listing Price vs. Final Sale Price: This tells an investor how much “wiggle room” there is in a specific neighborhood.

- Days on Market (DOM): A crucial metric for identifying distressed assets or cooling markets.

- Property History: Knowing how many times a property has been sold or refinanced provides insight into its long-term financial health.

- Specific Disclosures: Information regarding taxes, HOA fees, and internal upgrades that directly affect the net present value of the investment.

Without this granular data, an investor is essentially flying blind. Using inaccurate data from third-party aggregators can lead to overpaying for an asset, which is a cardinal sin in personal finance.

The Impact of MLS on Property Appreciation and ROI

The MLS plays a direct role in a homeowner’s Return on Investment (ROI). Because the MLS requires standardized data entry, it allows for better “indexing” of neighborhoods. When a house down the street sells for a record high on the MLS, that data point is immediately used by appraisers to value neighboring homes.

This creates a transparent trail of appreciation. For someone looking to use their home as a financial tool—perhaps through a Home Equity Line of Credit (HELOC) or a cash-out refinance—the MLS data provides the evidence needed by banks to approve those financial products. In essence, the MLS helps “prove” your wealth to the rest of the financial world.

The Financial Evolution: Modern Trends and the MLS Model

As with all things in the “Money” niche, the MLS is currently undergoing a period of significant evolution. Changes in technology and legal precedents are reshaping how this data is accessed and how much it costs to participate in this ecosystem.

From Private Databases to Open Market Transparency

For decades, the MLS was a “walled garden,” accessible only to licensed professionals. However, the rise of “Brokerage Feed” technology (IDX) has allowed portions of MLS data to flow into the public domain via sites like Zillow, Redfin, and Realtor.com.

While this has democratized access to information, it has also changed the financial strategy for buyers. Today’s savvy financial consumer uses public data to do preliminary research but relies on the “full” MLS data via a broker to make the final transaction. This two-tiered system of information ensures that those who are serious about their capital still seek out the most accurate, unfiltered data source available.

The Impact of Commission Structure Changes

A major topic in business finance recently has been the legal challenges regarding how real estate commissions are handled within the MLS. Historically, a seller would offer a set commission to a buyer’s agent within the MLS listing.

Recent legal settlements in the United States are decoupling these payments. From a personal finance standpoint, this is a monumental shift. It means buyers may now have to budget for their own representation out-of-pocket, or negotiate it differently. This change is forcing a new level of financial literacy among consumers, as they must now calculate the “all-in” cost of a real estate transaction with more precision than ever before.

Navigating the MLS Ecosystem for Financial Success

Whether you are a first-time homebuyer or a seasoned landlord, your financial success depends on how you interact with the information derived from the MLS.

Working with Brokers to Leverage MLS Insights

In the world of investing, information is the ultimate currency. While you can find a house on a public app, a professional with MLS access can provide you with “hot sheets” and “under-contract” data that hasn’t hit the public sphere yet.

For a buyer looking for a deal, getting access to a property 24 to 48 hours before it appears on a major app can be the difference between a successful purchase and being outbid. In a competitive market, time is literally money. A broker acting as your “data gatekeeper” can filter the MLS for specific financial criteria—such as price-per-square-foot ratios or specific zoning codes—that allow for high-yield investment strategies like “house hacking” or short-term rentals.

Common Myths That Could Cost You Money

There are several misconceptions about the MLS that can lead to poor financial decisions:

- “Zestimates are as good as MLS data”: Public algorithms are often off by 5-10% because they lack the “sold” data and specific interior condition notes found only in the MLS. Relying on an algorithm for a $500,000 purchase is a major financial risk.

- “Everything is on the MLS”: While the vast majority of homes are there, “Pocket Listings” or “Off-Market” deals exist. However, for a seller, staying off the MLS usually means less exposure and a lower final sale price—a net negative for their personal balance sheet.

- “The MLS is a government entity”: It is not. It is a private business network. This means it is governed by market incentives. Understanding that the MLS is a business tool for brokers helps investors understand why the data is kept so strictly updated—because the brokers’ own commissions and reputations depend on it.

Conclusion: The Bottom Line on MLS and Your Money

In conclusion, the Multiple Listing Service is the invisible hand that guides the residential and commercial real estate markets. For anyone interested in the “Money” niche—be it through personal finance, wealth management, or active investing—the MLS represents the pinnacle of market efficiency.

It provides the transparency needed to value assets, the exposure needed to sell them at peak prices, and the historical data needed to project future growth. While the tools we use to access this data are changing, the fundamental value of a centralized, verified, and professional real estate database remains unchanged. By understanding the power and the mechanics of the MLS, you position yourself to make smarter, data-driven decisions that will protect and grow your net worth for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.